A $1 Trillion Fed-Fueled Borrowing Bonanza for the Creditworthy

A $1 Trillion Fed-Fueled Borrowing Bonanza for the Creditworthy

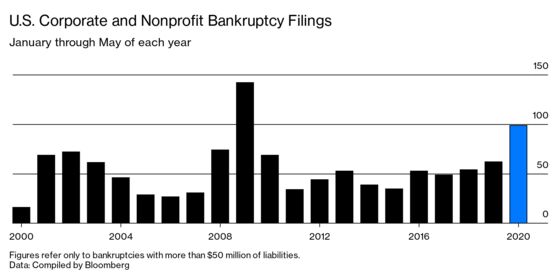

(Bloomberg Businessweek) -- With the pandemic lockdowns starving many businesses of revenue, debt is becoming either the key to survival or a ticket to bankruptcy in corporate America. Companies strong enough to gain access to the bond markets have borrowed $1 trillion this year at the fastest pace on record. Then there are those that can’t afford to carry the debt they have, leading to the most large bankruptcy filings in the first five months of the year since 2009, during the Great Recession.

One of the first things the Federal Reserve did in response to the pandemic was pledge to buy investment-grade corporate bonds. Later it even said it would buy some of the highest-rated junk bonds. The effect was dramatic, reassuring bond investors and driving down interest rates even before purchases began. Funds that invest in U.S. investment-grade bonds, junk bonds, and leveraged loans saw a combined inflow of $13.8 billion in the week ended May 27, the largest on record, according to data from Refinitiv Lipper. That abundance of buyers has helped issuers such as Boeing Co. and Marriott International Inc. raise money to ride out the crisis.

“The Fed took a market that had no certainty and put as much certainty into it as they could,” says Elaine Stokes, a portfolio manager at Loomis Sayles & Co. “It almost becomes inevitable that there’s this crazy amount of demand.”

Fed Chair Jerome Powell has said the borrowing spree is a “really good thing,” and the bond sales help avoid turning “liquidity problems into solvency problems.” But the Fed’s support is only temporary, and there’s concern that more borrowers may find themselves in distress when that support inevitably stops. “The Fed is providing liquidity to the higher parts of the credit market, which has kept investors in buying mode,” says Winifred Cisar, head of credit strategy at Wells Fargo & Co. “But on the other side, if you have a larger credit universe, your number of defaults will be higher. That’s just the math.”

The debt binge started out with some of the highest-quality borrowers, such as Exxon Mobil Corp. and Verizon Communications Inc. Some top-notch borrowers have simply taken advantage of cheap funding costs. Amazon.com Inc., for example, set a new low for corporate interest rates on bonds it sold on June 1. For debt due in three years, investors agreed to receive a coupon of just 0.4%. It’s also paying record-low rates on bonds due in 7, 10, and 40 years, according to data compiled by Bloomberg. Apple Inc. borrowed earlier in May to help buy back stock, while asset management giant BlackRock Inc. and drugmaker Pfizer Inc. may use recent bond proceeds to refinance debt.

But the borrowing has since expanded to riskier investment-grade companies such as the cruise line Carnival Corp. and into the depths of junk, including AMC Entertainment Holdings Inc., which runs movie theaters. Some of this could arguably be labeled rescue financing—without new borrowing, many companies could be in serious trouble.

Companies in sectors hit hardest by the virus may be paying stiff prices for their borrowing. Many, including rental car company Avis Budget Group Inc. and Norwegian Cruise Line Holdings Ltd., are paying interest rates well above 10%. “We issued bonds to get through the tough times and we feel comfortable with the position we’re in,” says David Calabria, senior vice president of corporate finance at Avis Budget. Carnival, Norwegian, and AMC didn’t respond to requests for comment.

At the same time, a buoyant bond market hasn’t been enough to help all companies. In May alone, 28 companies with liabilities greater than $50 million filed for bankruptcy, compared with 29 in May 2009. For the year through May, the tally stands at 99 companies seeking court protection. In bankruptcy, companies are able to negotiate with their existing creditors to find a way forward.

Many of these businesses were already in crisis. Retailers J.C. Penney Co. and J. Crew Group Inc., which both sought Chapter 11 protection from creditors in May, were debt-choked and squeezed by online-only rivals. In the energy sector, Hornbeck Offshore Services Inc. and Ultra Petroleum Corp. had both noted the risk of bankruptcy even before energy prices went into a historic crash that briefly took crude prices into negative territory.

Now the wave is sweeping up companies that were in decent shape before Covid-19, only for the pandemic to swiftly upend their businesses. Car rental giant Hertz Global Holdings Inc. had access to the capital markets in November, and its bonds due in 2028 traded above par as recently as late February, though it didn’t take long for travel shutdowns to zap demand for rental cars and ultimately force it into bankruptcy. The pain extends beyond U.S.-based businesses. Latam Airlines Group SA, Latin America’s largest air carrier, filed for Chapter 11 protection in New York on May 26 despite posting four consecutive years of profits before the crisis.

Neither company was perfect—each had junk-grade ratings—though they were hardly distressed. But experts say more bankruptcies are to come from ailing retailers that can only skip rent payments for so long—and airlines that aren’t expected to see a substantial recovery in passenger demand until 2023, according to S&P Global Ratings.

The next concern on the horizon is that the borrowing of 2020 is creating a group of so-called zombie companies. These are businesses that can borrow their way through the next few months but may not be able to earn enough to cover interest payments. Although they may have been investment-grade before the pandemic, they might also be in businesses such as travel that will suffer its effects long after people are able to do basic things like get haircuts again. “If revenues don’t turn around quickly for many companies, the lifeline created by accessing the credit markets may not be enough,” Patrick Leary, chief market strategist at Incapital, wrote in a May 28 report. In that case, “the issue of insolvency just got a whole lot larger.” —With Sally Bakewell

Read next: How Larry Fink’s BlackRock Is Helping the Fed With Bond-Buying

©2020 Bloomberg L.P.