It’s Always Sunny at the Davos of the Private Equity Industry

It’s Always Sunny at the Davos of the Private Equity Industry

(Bloomberg Businessweek) -- Berlin’s Tegel Airport is a Cold War throwback, hailing from the time before travelers had to go through perfume shops, luxury stores, and immense food courts to board a flight. It’s too small to comfortably serve the now hip and hopping capital of Germany—there aren’t that many direct flights from the U.S.—but that doesn’t stop the crowds from coming.

And each year in late February, Tegel welcomes a particularly exclusive set of visitors: Some fly in on private jets; others straggle in through connections, feeling ragged though still dressed in expensive jeans and Allbirds. They’ve booked as many as 20 back-to-back 30-minute meetings for each of the next four days, encounters that have been described as Wall Street speed dating.

They’ve come to court the people controlling trillions of dollars in assets, who have also arrived in Berlin for a convention at the InterContinental Hotel. It’s called SuperReturn International, a party of 2,500 attendees celebrating the private equity industry—the firms that invest in almost every big company you’ve ever heard of and are looking to own even more.

Collectively, private equity firms manage upwards of $3 trillion. Outback Steakhouse, the Weather Channel, and Neiman Marcus have all passed through their hands, entwining the industry in our everyday lives. Just one firm, Washington-based Carlyle Group LP, which has controlled everything from Hertz to AMC movie theaters, has a total of about 900,000 employees in all the companies it currently owns.

Other major players include Leon Black’s Apollo Global Management LLC—which in 2017 raised a record-setting $24.7 billion for its ninth fund—KKR & Co., TPG Capital, and the biggest of them all, Blackstone Group. Blackstone expects to reach about $20 billion when it completes the first phase of capital-raising for its flagship fund in coming weeks. These firms raise money from insurance companies, pension funds, endowments, and other big investors. They amplify their buying power with borrowed money in the form of leveraged loans and high-yield bonds. They’re well-paid for their work: typically “2 and 20”—a 2 percent annual management fee and 20 percent of any profits. They remake the purchased companies, sell them off to private buyers or take them public, and reap the rewards.

The firms’ billionaire co-founders—Carlyle’s David Rubenstein, KKR’s Henry Kravis, Blackstone’s Stephen Schwarzman, and others—have emerged as statesmen-philanthropists, counseling presidents, making huge contributions to universities (Kravis at Columbia Business School), setting up Rhodes scholarship-like programs in China (Schwarzman), and even renovating the Washington Monument (Rubenstein, who’s also the host of The David Rubenstein Show on Bloomberg TV). They also invest in the sports world. In the NBA alone, the Philadelphia 76ers, Atlanta Hawks, Boston Celtics, Detroit Pistons, and Milwaukee Bucks are all owned by one or more private equity billionaires.

In Berlin, which was unseasonably sunny and warm for winter, the mood reflected all that success and influence. The main convention hall buzzed with interviews, as journalists sniffed out the deals being negotiated behind closed doors, in smaller sessions, at private dinners, and in the German capital’s bars and nightclubs. The private equity firms were looking for new places to invest, but they were also wooing the endowments and institutional investors whose enormous pools of cash have made the industry one of the most important—if opaque—engines of the global economy.

What can possibly go wrong?

Pessimists point out that at the previous peak of the private equity industry, in 2007, buyouts regularly passed the $20 billion mark. The two biggest deals ever—Blackstone’s buyout of Equity Office Properties Trust (an unmitigated success) and KKR and TPG’s purchase of power company TXU (an abject failure)—were signed that year. And then the Great Recession set in. A few companies bought by private equity firms, such as Toys “R” Us and Claire’s, collapsed from a combination of too much debt and the weak economy. But some buyouts survived the financial meltdown. In July 2007, as the crisis was beginning, Blackstone bought Hilton Hotels Corp. Today it stands as the most profitable buyout of all time, and Hilton is publicly traded.

Successes like that ensured that private equity wouldn’t fade away, and as the world economy recovered, the industry faced none of the wrath and regulation directed at others on Wall Street. Investment banks such as Goldman Sachs Group Inc. and JPMorgan Chase & Co., which help finance private equity deals, found themselves answering to lawmakers and subject to a host of new regulations; they were essentially barred from activities that put them in competition with their private equity clients (a fund run by Goldman had been one of the owners of TXU). Private equity firms stepped in to take up some of the work deemed too risky for banks in their newly scrutinized state, especially making sometimes risky loans to small and midsize companies. Blackstone, KKR, Carlyle, Apollo, and Ares Management all became publicly traded companies, accelerating expansions into businesses far beyond leveraged buyouts. More important, they continued to amass massive war chests from investors desperate for returns better than they were getting in public markets.

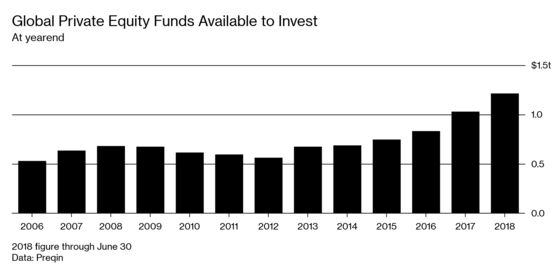

So what might cloud the sunny private equity environment? Brexit? The left wing of the Democratic Party? The Federal Reserve? At SuperReturn, one of the concerns was dry powder—that is, money investors had committed to private equity companies that they haven’t used yet. As that amount moves toward $1.5 trillion, many worry that there aren’t enough good deals to absorb it. A company that starts as a bargain could quickly become overpriced if managers eager to deploy their cash start bidding against one another.

Volatility can be a good thing—that touch of uncertainty disrupts equations and brings prices down. Ares Chief Executive Officer Michael Arougheti says his team was salivating in the wake of last year’s Christmas Eve sell-off and wild market swings. “It was a little bit of an appetizer,” he says. “Those are the types of markets where we do the best.” But with stocks climbing steadily, opportunities can be scarce.

Confident dealmakers such as Joseph Baratta, global head of private equity at Blackstone, say they’re willing to wait. “Certain sellers are going to have to realize that prices have come down,” he says, adding that the industry has years to put its money to work—even if it can’t right away, there’s no real penalty for not investing.

But the private equity companies also have to sell, ideally after just a few years. Their profit model is built on unloading assets at the right time. One of the biggest recent mistakes among managers has been calling the top too soon. During an onstage conversation between Black and Rubenstein in Berlin, Apollo’s founder conceded that his warning six years ago to sell “everything that’s not nailed down” was a bit premature.

Interest rates are a critical factor, so the firms watch the Fed and other central banks carefully. When rates go up quickly the cost of borrowing soars, making deals more expensive. Coupled with higher purchase prices, that heightens the possibility of lower returns when the time comes to sell. Higher interest rates are “the one thing in the world that could upset what’s going on today,” says Brookfield Asset Management Inc. CEO Bruce Flatt, adding that he doesn’t expect rates to rise much in the near term.

Then there’s politics. Flatt oversees about $350 billion, much of it in real estate. The company controls swaths of Lower Manhattan and the Canary Wharf district in London. The latter has given him a front seat to Brexit. Flatt and his private equity brethren insist that Prime Minister Theresa May’s drama will be only a speed bump. It hasn’t yet dented their business in London.

Perhaps the most unpredictable political risk is the populist bent of the Democratic Party in Washington. That might bring private equity under political and regulatory scrutiny as never before. In 2007 lawmakers were riled, basically, at how much money the private equity tycoons made and how they benefited from the “carried interest” loophole, which allowed the bulk of their personal earnings to be taxed as capital gains, not ordinary income, resulting in huge savings. That flurry of unwanted attention led the industry to launch its first real lobbying effort, an all-out campaign that successfully beat back legislation to change the tax treatment.

When Mitt Romney, co-founder of private equity firm Bain Capital LP, ran for president in 2012, both his Republican primary rivals and ultimately his opponent for the Oval Office, President Barack Obama, pilloried him for his private equity past, casting him as a heartless, job-cutting fat cat.

Alarmed at being portrayed as vulture capitalists, the industry sought to soften its image during the long bull market. Its lobbying group changed its name from the Private Equity Growth Capital Council to the American Investment Council. The AIC goes from lawmaker to lawmaker in the halls of Congress to emphasize the number of employees at private-equity-backed companies. Private equity chiefs have also begun talking about their various “stakeholders,” building teams to ensure they’re working not just with investors, but also with communities, regulators, and lawmakers. The companies’ leaders have historically avoided being summoned to testify on Capitol Hill. But the time may be coming for a public inquisition. Democratic presidential candidate and Massachusetts Senator Elizabeth Warren was among those who publicly, and successfully, pressed KKR and Bain to front $20 million for severance to former employees of Toys “R” Us, which had gone bankrupt, in part, because of debt incurred in the 2005 leveraged buyout. Many in the industry fear the concession could create a precedent, forcing them to set aside money in future deals for such contingencies, crimping profits.

Can private equity avoid the pitchforks? It is, to say the least, not a popular time to be a Wall Street billionaire. The amount of money they’re pulling in remains astounding. Schwarzman took home $567.8 million in dividends and compensation in 2018. And that was a bit of a comedown. In 2017 he earned $786.5 million.

Still, firms believe they can see enough of the political horizon to prepare for and ride out turbulence. The industry seems to be ready for everything—everything that can be expected, that is. A black cloud can appear, or a black swan. It’s always sunny weather—until it’s not.

To contact the editor responsible for this story: Howard Chua-Eoan at hchuaeoan@bloomberg.net

©2019 Bloomberg L.P.