‘Inflation Guy’ Has Been Waiting Years to Tell You About the I-Word

‘Inflation Guy’ Has Been Waiting Years to Tell You About the I-Word

(Bloomberg Businessweek) -- Michael Ashton, who styles himself “Inflation Guy” on Twitter, has been preparing for this moment for almost 20 years. In the early 2000s, he was a derivatives trader at Barclays Capital in New York when he was tapped to build a business around inflation swaps, contracts that let traders bet on a rise in consumer prices. Ashton says he was a “good enough” trader—the real job was to build a new market by being “an evangelist for the product.”

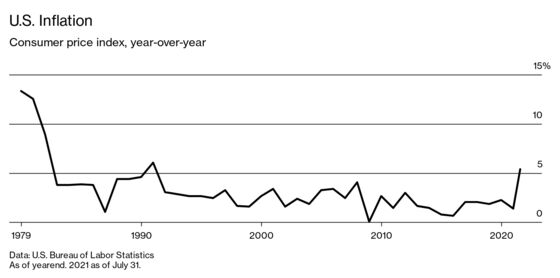

He became one even though, until recently, he expected inflation to be low and stable. Correctly so: In recent years, the U.S. consumer price index has often grown below 2% annually. Ashton says his measured outlook irritated his bosses at Barclays, who viewed it as an impediment to drumming up business. He thought it didn’t matter: Inflation was an ever-present risk, he was inventing ways to insure against it, and low inflation made it cheap to do so. But while the market grew, and Ashton in 2009 founded an advisory business for hedging large or unusual inflation risks, he remained a voice in the desert crying out that he had rain boots for sale. “The lack of interest was amazing,” he says. “It’s incredible how little people thought about it—what that risk was.”

Suddenly, that’s no longer true. Inflation has spiked this year, and while Federal Reserve Chair Jerome Powell says it’s probably a temporary supply shock as the economy emerges from lockdown, Ashton sees more on the way. And he says business is booming. New customers include two private equity firms that he says are “very concerned about the effect inflation has on portfolio companies.” He’s launching a fund for wealthy and institutional investors to track the monthly change in the U.S. consumer price index via a combination of inflation-protected bonds, whose principal value is adjusted to changes in the CPI, and futures linked to energy, Japanese yen, and an index of home prices.

At the same time, Ashton is having to defend his turf. “All of a sudden there’s all these inflation experts around,” he says. “I put in 10,000 hours waiting for this to happen. Now that it’s happened, I’m positioned to save the day, as it were.” And so Inflation Guy, who until recently limited his public-facing activity to a Twitter feed that mainly dissected the monthly CPI reports, launched a podcast. Its logo shows him wearing a superhero cape emblazoned with the letter “i.”

Its objective is inflation education for an investing population that has had the luxury of ignoring it for a long time. While people under 40 have barely experienced it, inflation, he says, “is the risk that every investor is born with, and if you do nothing to address that inflation risk, you have it until the day you die.” The difficulty in making that argument is that some people banging the same drum are conspiracy theorists, Ashton says. It doesn’t take long to find the corners of the internet dedicated to the proposition that the government has been intentionally understating inflation by a wide margin for half a century. “The crazy train,” he calls it.

But even outside those fevered quarters, there’s plenty of debate about what causes inflation. Ashton says his views “are distinctly non-mainstream”—meaning he’s a monetarist, or someone who believes that inflation is mainly a consequence of too much money in the system, rather than overheated economic growth or other factors. The idea once held tremendous sway, but in recent years it has fallen out of favor with economists and central bankers. The Fed under Alan Greenspan finally stopped targeting money supply growth in 2000 because, he’d said, it was no longer “a reliable indicator of financial conditions in the economy.”

With the Fed’s M2 money supply index having increased about 33% since February 2020, roughly five times faster than the economy, we may be about to find out if monetarism can make a comeback. A counterpoint is that even though the Fed’s pandemic recovery efforts have created more money by some measures, the velocity of those dollars—how often they change hands in a given period of time—is still low. If people and businesses are hanging on to their money, there’s less pressure on prices. For the past 18 months, “we haven’t seen any of the pass-through from increased money supply to increased lending and spending,” says Omair Sharif, president of the research company Inflation Insights. Inflation skeptic Lacy Hunt, chief economist at Hoisington Investment Management Co., predicts velocity will keep falling because of rising debt levels dampening growth.

Ashton says the appeal of monetarism is that it keeps things relatively simple. He became a convert after couple of years of constant tinkering with inflation models that used economic growth inputs. “I stepped back and said, if you have to keep re-parameterizing the model, it probably means there’s something wrong with the fundamental theory,” he says. A monetarist view of the past several decades is that there’s been a virtuous cycle in which lower inflation led to lower interest rates, which in turn is what actually caused the lower velocity. (People were in less of a hurry to invest their cash since low interest rates also mean lower returns.) Ashton says the Fed’s recent stimulus efforts risk reversing that cycle. While the Fed assumes it can eventually bring inflation under control by raising rates, he says this may instead goose velocity by making people less willing to hold cash.

Ashton thinks it’s possible sustained higher inflation won’t come to pass, but he says he has about 70% confidence in his forecast. His broader point is that people should be mindful of inflation risk even when they think it’s low. After all, with 10-year Treasury notes, a benchmark for safe long-term investments, yielding just 1.3%, even a fairly modest amount of inflation can erode the value of savings over time. For retail investors looking for a simple hedge, Ashton points to Series I savings bonds from the U.S. Treasury, which pay a rate linked to inflation. “A rare good deal from the government,” he says.

Read next: Soaring Cost of Food Is Forcing Families to Scrimp at the Dinner Table

©2021 Bloomberg L.P.