In Fink We Trust: BlackRock Is Now ‘Fourth Branch of Government’

In Fink We Trust: BlackRock Is Now ‘Fourth Branch of Government’

(Bloomberg Businessweek) -- When the Federal Reserve needed Wall Street’s help with its pandemic rescue mission, it went straight to Larry Fink. The BlackRock Inc. co-founder, chairman, and chief executive officer has become one of the industry’s most important government whisperers. In contrast to other influential financiers who’ve built on ties to President Trump, Fink possesses a power that’s more technocratic. BlackRock, the world’s largest money manager, can do the things governments need right now.

The company’s new assignment is a much bigger version of one it took on after the 2008 financial crisis, when the Federal Reserve enlisted it to dispose of toxic mortgage securities from Bear Stearns & Co. and American International Group Inc. This time it will help the Fed prop up the entire corporate bond market by purchasing, on the central bank’s behalf, what could become a $750 billion portfolio of debt.

One part of the Fed’s plan is to buy bond exchange-traded funds. BlackRock itself runs ETFs under the iShares brand, and could end up buying funds it manages. There are rules in place to avoid conflicts of interest—for example, it won’t charge the Fed management fees on ETF shares. “BlackRock is acting as a fiduciary to the Federal Reserve Bank of New York,” says a spokesman for the company. “As such, BlackRock will execute this mandate at the sole discretion of the bank, and in accordance with their detailed investment guidelines.”

Still the arrangement is bringing new attention to the company’s scale and ubiquity. “It’s impossible to think of BlackRock without thinking of them as a fourth branch of government,” says William Birdthistle, a professor at the Chicago-Kent College of Law who studies the fund industry.

Fink was on the shortlist in 2012 to replace outgoing Treasury Secretary Tim Geithner. Now he’s widely viewed as a contender for that post in a possible Joe Biden administration. It isn’t clear how that would be received by the Democratic Party’s left flank. But Fink stands out for Wall Street-friendly members of the party who see value in the expertise of financiers.

The company’s primary business, index fund management, has been hailed for making investing easier and cheaper. And while some of his funds hold shares of fossil fuel companies, making Fink the bête noire of some environmentalists, he urges companies to better prepare for the realities of climate change and pursue a purpose beyond simply profit.

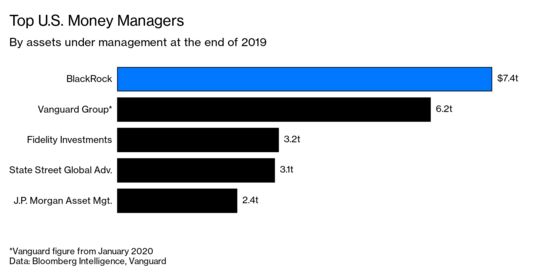

There’s probably no other financial institution that brings to the table what BlackRock does. It’s experienced in running large portfolios on behalf of others. It’s ubiquitous in markets for everything from passive, index-linked products to hands-on mutual funds, with $6.5 trillion in assets under management as of March 31. It’s the largest issuer of ETFs, which act like mutual funds but trade on an exchange. It actively manages more than $625 billion in bond funds for pension plans and other institutional clients. Almost anyone looking to buy a diverse portfolio quickly would consider BlackRock—and the Fed did the same. In a virtual hearing of the Senate Banking Committee on May 19, Fed Chairman Jerome Powell said BlackRock was hired for its expertise and “it was done very quickly due to the urgency” of the matter.

Beyond money management, BlackRock’s software platform, Aladdin, appealed to the Fed. The program evaluates risk for clients that include governments, insurers, and rival wealth managers, monitoring more than $20 trillion in assets. (Bloomberg LP, the parent company of Bloomberg News, sells financial software that competes with Aladdin.)

BlackRock has ascended to speed-dial status among Washington officialdom in part through shrewd business maneuvering. It scooped up Barclays Global Investors, including its iShares ETF division, in the fallout from the 2008 crisis. That gave BlackRock a stronghold in low-cost index funds, transforming it into the world’s largest asset manager almost overnight—and supercharging more than a decade of growth.

At the same time, the money manager built a powerful advocacy arm. Its sphere of influence reaches beyond the central bank to lawmakers, presidents, and government agency heads from both political parties, though its hiring leans Democratic. Bloomberg found only a handful of current BlackRock executives who came out of the George W. Bush administration, but more than a dozen Barack Obama alumni. These include Obama’s national security adviser, senior adviser for climate policy, the former Federal Reserve vice chairman he appointed, and numerous White House, Treasury, and Fed economists.

Its influence is also global: The Bank of Canada tapped BlackRock in March as an adviser for its purchases of commercial paper, the short-term debt that companies use to fund day-to-day expenses such as payroll. Last month the European Union hired the money manager to advise it on how to incorporate environmental, social, and governance practices into the way EU banks manage risk.

The Fed has also tapped Pacific Investment Management Co. to revive its 2008 role buying commercial paper. And after evaluating responses to a request for proposals, the Fed chose State Street Corp. to act as the administrator and keeper of securities for some of its emergency programs.

BlackRock, however, was handed three Fed assignments without any competitive process—though the Fed plans to rebid the contracts once the programs are in full swing. BlackRock will manage portfolios of corporate bonds and debt ETFs. It will do the same for newly issued bonds—sometimes acting as the sole buyer—and for up to 25% of bank-syndicated loans. And it will purchase commercial mortgage-backed securities from quasi-government agencies such as Fannie Mae and Freddie Mac.

BlackRock could reap as much as $48 million a year in fees for its Fed work, according to a Bloomberg analysis. That’s no windfall, especially in relation to its $4.5 billion in earnings last year. But it may further cement the money manager’s ties with policymakers. On May 12, BlackRock began the first stage of these programs when it began buying ETFs.

As with technology companies Facebook Inc. and Alphabet Inc., BlackRock’s growth raises questions over how big and useful a company can become before its size poses a risk. The firm has long argued that, unlike banks, it’s not making investments for itself with tons of borrowed money. Watching over large sums of money for clients doesn’t make its business a threat to the broader financial system.

With its latest assignment, that argument could be harder to make, says Graham Steele, director of the Corporations and Society Initiative at the Stanford Graduate School of Business. “They are so intertwined in the market and government that it’s a really interesting tangle of conflicts,” says Steele, who formerly worked at the Federal Reserve Bank of San Francisco. “In the advocacy community there’s an opinion that asset managers, and this one in particular, need greater oversight.”

Already there are growing worries about the power of BlackRock, Vanguard Group Inc., and State Street, often called the Big Three because they hold about 80% of all indexed money. That raises concerns about how they wield their voting power as shareholders and has even drawn attention from antitrust officials.

BlackRock avoided being branded too big to fail after the 2008 meltdown, when regulators weighed whether big asset managers should be regarded as systemically important. The concern then was that funds could amplify market stress by rushing to sell assets to meet client redemption demands.

The current crisis, and BlackRock’s role in the cleanup, comes with different risks. The company could become a focus of public antagonism if things don’t go well. It’s a massive corporation aiding the central bank in a bailout that’s already been criticized for favoring massive corporations.

And then there are the potential conflicts. One arm of BlackRock knows what the Fed is buying, while other parts of the business participating in credit markets could benefit from that knowledge. To avoid conflicts, “there are stringent information barriers in place,” says the BlackRock spokesman. BlackRock employees working on the Fed programs must segregate their operations from all other units, including trading, brokerage, and sales. The fee waiver on ETFs helps avoid the appearance of self-dealing.

But BlackRock’s contract with the Fed also acknowledges that senior executives “may sit atop of the information barrier” and “have access to confidential information on one side of a wall while carrying out duties on the other side.” Staff working on the Fed programs must go through a cooling-off period before moving to jobs on the corporate side, but it would last only two weeks.

Birdthistle, the Chicago-Kent law professor, suggests the Fed could have made its process more competitive by allocating some of its funds for buying corporate credit to a group of asset managers from the outset, instead of just one. “It raises the question: Why did all the money have to go to one company?” he asks. “I get why BlackRock would be on the list, but I don’t understand why it would be the only one on the list.”

©2020 Bloomberg L.P.