Don’t Feel Too Relieved by the Bounce Back in Stocks

Don’t Feel Too Relieved by the Bounce Back in Stocks

(Bloomberg Businessweek) -- Is this a bear market or a bull market? It’s a strange question to ask just weeks after a 34% decline in the S&P 500, but here we are. The surge in the index from its low on March 23 exceeded the 20% threshold many consider to define the start of a new bull market, even if the record high on Feb. 19 remains a distant memory. Like anyone stuck in their home for the last few weeks lamenting that they aren’t sure exactly what day it is, the Covid-19 virus is causing a disorienting effect on investors. No one seems 100% sure what type of market environment this is.

Bear markets are famous for including stunning rallies that turn out to be short-lived. The financial crisis had a few such upswings, including a 24% surge from late November 2008 into early January 2009, before the final low was finally set in March. Underpinning the current confusion is an unprecedented series of interventions by the Federal Reserve, combined with a still-fuzzy picture of just how long the virus will wreak havoc on the economy and corporate profits. The picture may begin to clear as companies begin to report their results for the first quarter and offer guidance about what to expect for the rest of the year.

That can’t come soon enough, considering how starved of forward-looking data Wall Street is after so many companies have withdrawn their forecasts. A buzz saw is headed for corporate profits this year, but the extent of the damage is still a bit of a guess. Imagine you owned a representative slice of the S&P 500, worth $2,762 based on the index’s level of about 2,762 on April 13. The high estimate among Wall Street strategists tracked by Bloomberg for your full-year 2020 earnings per share is $178, while the low is $110. That’s a spread of $68 a share. In early December, the difference between the high and low forecasts was $16.

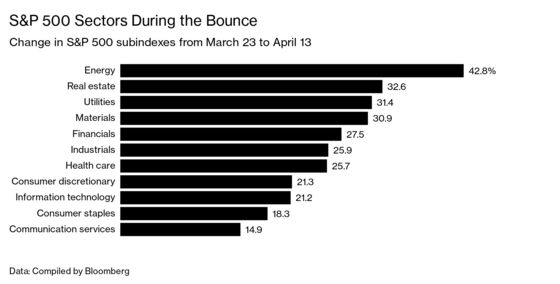

Those strategists are focused on overall S&P profits. Looking at estimates based instead on analysts’ forecasts for individual companies, it’s hard to argue that a sustained rally is under way. Profits at S&P 500 companies are estimated to have shrunk 11% in the first quarter, led by a 51% plunge in energy company earnings and 31% drops for the consumer discretionary and industrial sectors. The second quarter is expected to be even worse, with an estimated 22% decline in S&P 500 earnings, followed by decreases of almost 10% in the third quarter and 1.2% in the fourth.

So what explains the recent buying? The bulls’ case boils down to that simple, time-tested Wall Street rule: Don’t fight the Fed. And this time, don’t fight Congress, either. The Federal Reserve is basically writing blank checks to shore up the fixed-income markets that otherwise could drag the stock market into the dirt with them, and lawmakers are spending trillions of dollars to mitigate the damage caused by shutting down vast swaths of the economy to slow the spread of the virus. Whether those trillions will be enough is a further debate, but investors think Congress is at least moving in the right direction.

“The combination of unprecedented policy support and a flattening viral curve have dramatically reduced downside risk for the U.S. economy and financial markets and lifted the S&P 500 out of bear market territory,” Goldman Sachs strategists led by David Kostin wrote to clients on April 13. “If the U.S. does not experience a second surge in infections after the economy reopens, the ‘do whatever it takes’ stance of policymakers means the equity market is unlikely to make new lows.”

That “if” about infections is a big one, of course. And there are a lot of questions about just how many cylinders the economy will be firing on when it does reopen. How long will it take for consumers to feel comfortable crowding into restaurants, movie theaters, airplanes, amusement parks, and other tourist spots? How long until they are comfortable enough about their own economic prospects to pull the trigger on big purchases?

But forget all that for a minute, and just consider what the Goldman strategists and others are predicting may happen: The S&P 500 may have set its low for this episode on March 23, barely a month after its last record high on Feb. 19. That is unheard of in the history of bear markets since 1929. It took an average of 373 trading days from record high to bottom during those 10 declines, according to numbers crunched by Bloomberg macro strategist Cameron Crise. The shortest time from peak to bottom was 74 days in 1987, and that bear market wasn’t accompanied by the type of major economic downturn that is in the cards today.

This argues that investors shouldn’t assume that the bear market is anywhere near over. At the same time, 2020 is the type of year in which historical precedents may not count for much. The speed at which the market entered bear territory is also unprecedented, as is the world’s response to this virus. Even OPEC and other oil-producing nations are getting into the precedent-breaking game, with historic cuts to production in an effort to shore up prices and the energy sector of the economy. Perhaps the lesson of 2020 is this: Just because something never happened before, that doesn’t mean it should be surprising.

©2020 Bloomberg L.P.