A Proposed Megadeal Exposes the Grim Outlook for Europe’s Banks

A Proposed Megadeal Exposes the Grim Outlook for Europe’s Banks

(Bloomberg Businessweek) -- The world’s largest money manager has a stark warning: More than a decade after the global financial crisis, European banks still face a long and tortuous path to recovery. “Europe is in the midst of a painful, painful transition,” Philipp Hildebrand, vice chairman of BlackRock Inc., said on Bloomberg TV. “I would expect it to entail significant changes in the way banks operate, in their business models, and it will take time.” Until then, he said, investors will probably steer clear.

That the region’s financial institutions, including some of the biggest, are in a state of grinding decline is a grave cause for concern—and not just for their stockholders and bondholders. Europe relies heavily on its lenders to fuel growth. Banks provide about three-quarters of financing to companies and nine-tenths of credit to households. In the U.S., corporations rely on capital markets—selling bonds and shares—for the bulk of their financing.

Indeed, part of the pressure on Deutsche Bank AG and Commerzbank AG to consider a merger came from parts of the German government that very much want a healthy national financial champion to help accelerate the country’s flagging growth. But there’s no easy fix. Both banks are struggling with their own overhauls, and even if they can manage the tens of thousands of job cuts that would likely come with a marriage, it’s not clear that a bigger entity would be significantly stronger.

With economic expansion sputtering not only in Germany but also across the European continent, time may be running out for banks to heal themselves. Another recession would complicate their turnarounds. At the heart of the difficulties are weak balance sheets and modest profitability. Many banks are still just barely able to cover their cost of equity—that is, what investors seek as compensation for companies’ perceived risk.

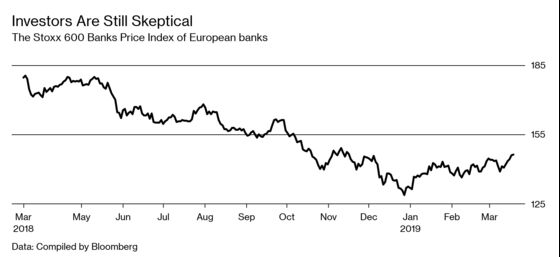

Nowhere is this lack of confidence more visible than in stock valuations. Since January 2018, when shares touched a two-year high, the benchmark Stoxx 600 Banks Price Index has dropped about 26 percent. European banks are worth just a quarter of their peak value, reached in 2007.

By comparison, U.S. banks have rebounded from the abyss and by early 2018 had recovered almost all of their post-crisis losses, with profits reaching a record last year. As measured by return on equity, profitability stands at about 9.5 percent in Europe. In the U.S. it’s closer to 12 percent.

European banks have bolstered their balance sheets, offloaded toxic assets, and retreated to core activities and geographies after the threats to their survival unleashed by the financial and subsequent sovereign debt crises. Nudged by more stringent regulation, they’ve also adopted more prudent lending and trading practices. But investors are hardly pricing that in. Banks on average trade at 20 percent below their book value, with a huge divergence that sees some of the biggest companies—that’s you, Deutsche Bank—trade at discounts of as much as 75 percent. By contrast, U.S. banks are valued significantly more highly by investors, at a 40 percent premium to book value, according to Bloomberg Intelligence.

While leaders of European banks can do more to address their institutions’ weaknesses to revive profitability, they’re stuck in a quicksand of low interest rates and rising costs. Regulation is forcing banks to hold more funds to help cushion potential losses in the event of crises, and investment needed to tighten controls and upgrade antiquated technology is pushing expenses higher. Meantime, competition from financial-technology upstarts is forcing banks to spend more on innovation and chipping away at fees they can charge on payments such as international cash transfers, all of which is eroding margins.

What’s more, the region’s failure to complete its vision for a single, Europe-wide financial-services market—the so-called banking union—has left in place obstacles that make it almost impossible for banks to grow outside their home markets. Instead, rising national interests have led to a splintering of Europe. Britain’s decision to leave the European Union will add further barriers and exacerbate the fragmentation of capital markets. The future looks bleak.

After the financial crisis, Europe and the U.S. set off on divergent courses. While the federal government swept in to recapitalize America’s biggest banks in 2008, getting them to write off their toxic assets sooner, Europe stopped short of forcing the broader industry to reboot, instead salvaging individual lenders that were on the verge of collapse. Seeking state backing carried a stigma of desperation that European lenders sought to avoid. They resorted to raising capital piecemeal and to modest reorganization.

Armed with stronger balance sheets, U.S. banks quickly recovered, while in 2011, when Europe was hit by another crisis, it became apparent that its lenders still needed fixing. As Cyprus, Greece, Ireland, Portugal, and Spain requested international aid—in part to prop up their financial industries—calls for capital injections to mimic what the U.S. had done weren’t heeded. Lenders in some of the bigger economies, such as Italy and Germany, were left largely to muddle through. “Europe’s big problem was that it reacted very slowly to the crises, taking small steps ex post each time and never taking ex ante resolute action,” says Dante Roscini, a Harvard Business School professor.

In the end, banks across the euro zone did get some help, but it was in the form of cheap loans from the European Central Bank—€700 billion ($795 billion)—and quantitative easing through the ECB’s purchase of €2.6 trillion in corporate and sovereign bonds. While that helped push up asset prices, improving bank balance sheets and bolstering confidence, it also encouraged banks to buy more of their own nations’ sovereign debt. That fueled a so-called doom loop that potentially reduces lending, undermining the economy, and adds to both bank and government weakness.

Since 2014 the ECB has also maintained negative interest rates, which have turned the bread and butter of the euro zone’s banks rancid. Among the bigger European lenders, the average net interest margin—the difference between the interest they receive on loans and what they pay out on deposits, adjusted for assets—is about 1.6 percent, less than half of the 3.3 percent enjoyed by the top U.S. banks, Bloomberg Intelligence data show. Banks in the 19 countries that use the euro have to pay 0.4 percent interest on the €2 trillion they park with the ECB, costing them about €8 billion every year, according to a recent research paper by Deutsche Bank.

ECB President Mario Draghi has signaled that low interest rates are here to stay. As he cut the growth forecast for the euro zone from 1.7 percent to 1.1 percent for 2019, Draghi pledged that rates will stay at the current record-low levels at least through the end of the year, pushing back the outlook for faster economic growth. “There is no end in sight to banks’ profit squeeze,” says Peter Hahn, a dean at the London Institute of Banking & Finance.

Just four months ago, the expectation that interest rates would rise helped lure Doug Braunstein, a former chief financial officer at JPMorgan Chase & Co., to Deutsche Bank stock. In announcing he’d bought a 3 percent stake in the bank in November, he pointed to the “significant upside” to earnings for the private and commercial bank from rising interest rates.

Deutsche and Commerzbank are holding exploratory talks to create Europe’s fourth-largest financial institution, with a €1.8 trillion balance sheet. The thinking is that by removing overlaps at home through job reductions, the deal will also lower the banks’ overall funding expenses. The combined businesses will see profitability rise, and the bigger company could also compete more effectively with other global banks in securities trading.

A combined bank would still have to cope with Europe’s structural inefficiencies. More than 6,200 banks operate across the EU. While that’s down from 8,500 in 2008, the market remains deeply fragmented. In Germany, the top five institutions hold about 30 percent of the banking assets; in the U.S., the figure is more than 65 percent.

A merger would leave Deutsche Bank and Commerzbank with just a 10 percent to 15 percent market share, giving them little pricing power in a cutthroat sector. Hundreds of Germany’s public-sector savings banks and cooperative lenders compete with commercial lenders on unequal terms, because they’re not as driven by profitability. While a single supervisor, the ECB, oversees the biggest lenders, smaller ones are regulated by national agencies, adding to inconsistencies. The absence of a truly single European market will continue to hinder cross-border combinations, too. Lenders can’t make the most of expanding outside their home markets, because they can’t move funds around freely. Even across the euro zone, countries still run individual deposit insurance programs.

National interests hinder progress. Some government officials are resisting efforts to create a Europe-wide agency to help detect and prevent dirty money flows, despite the obvious need. In September, Denmark’s Danske Bank AS reported it had moved about $230 billion, much of it suspicious, through its Estonia unit. Since then more than half a dozen European lenders have faced allegations of money laundering either as the prime lender or as correspondent banks.

The European Commission, the executive branch of the EU, has proposed giving more power to the European Banking Authority, but national judiciaries would probably still need to be the enforcers. Other structural weaknesses abound. The average European bank has sovereign debt exposure equal to 170 percent of its core Tier 1 capital, more than triple the exposure of U.S. banks, according to Deutsche Bank analysts. What’s more, about 60 percent of an average European bank’s sovereign holdings are of their home government’s debt, the research shows. That’s because, for now, sovereign debt on banks’ books still carries a zero risk weighting, meaning it doesn’t count in calculations of how much capital they must hold.

While choking under the weight of bad loans, Italian banks used much of the stimulus funding from the ECB to buy sovereign debt rather than boost lending in the recession-hit economy. As things stand, bad loans still make up more than 10 percent of total loans, and Italy slipped back into recession last year.

The ECB’s efforts to revive the euro zone’s economies by keeping rates low isn’t working, says Harvard Business School’s Roscini. “Instead of prompting businesses and households to borrow, negative interest rates over a long period create a sense of anxiety,” he says. “Banks need more profitability to take on more credit risk. Europe is beginning to look ever more like Japan.” That’s a grim description: Declining margins have left many of Japan’s lenders limping for two decades now.

—Martinuzzi is a finance columnist for Bloomberg Opinion.

To contact the editor responsible for this story: Howard Chua-Eoan at hchuaeoan@bloomberg.net

©2019 Bloomberg L.P.