Defying Dire Predictions, China Is the Bubble That Never Pops

Don’t tell President Trump, but China is winning.

(Bloomberg Businessweek) -- Don’t tell President Trump, but China is winning.

The U.S. has thousands of new Covid-19 cases a day. China’s reported daily case count is down to double digits. The U.S. is braced for an historic 6% contraction in gross domestic product. China’s rapid rebound means it’s poised for another year of growth—and a speedier catch-up in the race to overtake the U.S. as the world’s biggest economy. America’s international standing has seldom been lower. From the corridors of the World Health Organization to the protest-ridden streets of Hong Kong, China’s global clout increases.

For many, China’s world-beating rebound must come as a surprise. To read the history of China analysis in the last 30 years is to be bombarded with predictions of imminent demise. Sure, the skeptics conceded, double-digit growth looked impressive. But, they said, just poke beneath the surface, and the reality was an unsustainable bubble. The authoritarian political system was too constricting for the economy to truly thrive. Banks were stuffed with bad loans. The industrial landscape was littered with zombie companies, the urban landscape with ghost towns.

At first, it appeared Covid-19 would confirm that narrative. Reports about a virus contracted from bats and spread in a crowded wet market confirmed prejudices about a primitive and backward people. The story of Dr. Li Wenliang—the whistleblower who tried to alert China’s authorities but had been silenced—affirmed the superiority of the open U.S. system. Footage of mechanical drones barking “go home” at lockdown dodgers added fears about the rise of a surveillance superstate.

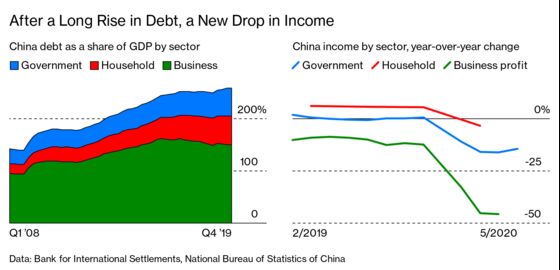

The lockdown hammered China’s economy. With factories closed, profits for state-owned enterprises slumped, falling close to 50% in the first months of the year. Home sales—a critical driver of China’s construction boom—plummeted. Tax revenue and land sales, which are the main source of revenue for local governments, followed them down. Workers faced rising unemployment and shrinking incomes. The official data showed the jobless rate rising above 6%. Cynics assumed the reality was worse.

In the grizzly bear narrative, the arch villain in China’s economy is debt. A four-trillion-yuan ($565 billion) stimulus that started as a powerful response to the 2008 great financial crisis ran too strong for too long. Debt for the economy as a whole rose precipitately—climbing from 140% of GDP in 2008 all the way to 260% in 2019. Everyone from International Monetary Fund policy wonks to Wall Street money managers to China’s own communist cadres were warning of a dangerous bubble.

The biggest borrowers—state-owned enterprises, real estate developers, local governments—were the very same groups that were now facing plunging incomes as Covid-19 swept through the economy. Surely the day of reckoning was nigh.

For some in the Trump administration, it seemed like a good moment for a victory lap. China’s outbreak would “accelerate the return of jobs to North America” said Wilbur Ross, the commerce secretary. Back at the end of January, when China had the virus and the U.S. did not, that seemed tone-deaf to human suffering. A few months later, with China in recovery mode and the U.S. reporting 2.2 million cases, it’s clear that it was also off-base on where the economic costs would fall.

Beijing took action on Feb. 1, a Saturday. For more than a week, China’s financial markets had been closed, an extended break as policymakers kept the 1.4 billion population on lockdown for the Lunar New Year holiday. On Monday, they opened again. With traders scrambling to price in a plethora of bad news—from a rising case count to falling markets in the U.S. and Europe—there was only one way the markets could go: down.

In a show of strength, the People’s Bank of China, the China Banking and Insurance Regulatory Commission, and the State Administration of Foreign Exchange issued a joint statement, committing to stabilize the market and extend more credit to small businesses stretched to the breaking point by the lockdown. More action followed. The People’s Bank of China injected 1.7 trillion yuan into the economy—a record slug of cash aimed at calming nervous markets. Interest rates were cut. Bearish short sellers faced new regulatory constraints. And cash-rich insurance funds were given a clear signal: Buy stocks now.

It worked. A drop in stocks was inevitable, but with the assurance of strong support from Beijing the market quickly regained lost ground. The yuan, a crucial gauge of investor confidence, moved back to the strong side of 7 to the dollar. China’s seven-day repo rate, the beating heart of the financial system, stayed low and stable, showing banks had no shortage of funds.

With the financial system steady, policy focused on plugging the gaps for businesses and households—preventing the lockdowns necessary to control the pandemic from triggering a downward spiral of bankruptcies and unemployment. Banks were told to go easy on borrowers. Nationwide, small enterprises and companies got a holiday on loan repayments. In Hubei, the epicenter of the outbreak, big ones were off the hook too. Fiscal policy shifted to reduce the burden on business, freeing up cash flow. An accountant at a cinema in the northern metropolis of Tianjin says breaks on taxes and social security contributions helped keep the lights on through the lockdown.

Major corporations, from state-owned dinosaurs to gleaming new tech titans, swung into action. From long experience, state-owned companies know the crisis drill—no letting workers go, no turning off the investment taps, keep money flowing through the system. Tencent Holdings Ltd. and Alibaba Group Holding Ltd., tech giants whose payment and messaging apps are the digital arteries of China’s economy, created add-ons that enabled the government to judge who could leave the house safely. Leveraging its payments network, Alibaba provided cut-price loans to small businesses and street vendors, helping keep them afloat through the lockdown.

The outcome will be far from perfect. China is poised for the lowest growth of the reform era. Bloomberg Economics’ forecast is for GDP to expand 2.1% in 2020, down from 6.1% in 2019 and the lowest since the start of Deng Xiaoping’s reform and opening in 1978. But a system-shaking crisis has been avoided. Markets are stable. Banks are still standing.

How did China manage once again to defy the doubters? The answer—as I argue in my new book, China: The Bubble That Never Pops—lies in the strengths of a system that are hiding in plain sight: rock-solid funding for the banks, state intervention that can be more strength than weakness, and the competitive edge that comes from enormous size.

Let’s start with the banks. Much ink has been spilled on the risks in China’s financial sector. Since November 2008, when then-Premier Wen Jiabao pressed the “go” button on the four-trillion-yuan stimulus, bank assets have more than quadrupled in size. Reviewing the history of credit bubbles, the IMF found none that had expanded so quickly, but plenty of more modest size that still imploded into crisis.

Worse, the problem of moral hazard—the assumption that a deep-pocketed government would backstop bad loans—was endemic. In 2019, cracks started to appear. Baoshang Bank Co., a city lender in Inner Mongolia, became the first Chinese bank in 20 years to fail. Defaults, including by state-owned companies and local governments, rose. Even ahead of the Covid-19 crisis, it seemed like sky-high debt, recklessly allocated, might result in a day of reckoning.

Maybe tomorrow, but not today. Missing from the crisis thesis was a crucial point: Financial meltdowns don’t start because bad loans are too high; they happen because banks run out of funding. In the Asian Financial Crisis in 1997, Korea’s banks didn’t melt down because they had made too many loans to crony-capitalist chaebol. They melted down because the foreign funds they relied on to finance their operations dried up. In 2008, Lehman Brothers didn’t collapse because it had too many investments in dodgy mortgage- backed securities. It collapsed because the money markets that financed its activity decided to cut it off.

In China, the combination of a high savings rate and tight controls on moving capital out of the country means that a lack of funding is unlikely to be a problem. Its banks can count on a steady inflow of domestic savings to provide a stable, long-term basis to fund operations. While helter-skelter expansion in lending is a problem—as are a state-dominated banking system and zombie borrowers—as long as bank funding remains adequate, there’s no trigger for crisis.

Then there is the nature of business. Nowhere is the contrast between the U.S. free-market system and China’s state-centric approach as sharply drawn as in the relationship between government and corporations. In the U.S., a hands-off approach is a critical driver of economic dynamism. In China, the biggest banks, telecoms, airlines, and industrial companies are owned by the state. Even in private companies, the Communist Party exercises an influence that would be unthinkable in the U.S.

There are major costs to this approach. “We’re state-owned, so we don’t have to worry about profits,” says the manager of one massive power project on the outskirts of Beijing. Writ large, that cavalier attitude to the niceties of actually making money means a big chunk of the corporate sector is mired in low productivity. Return on assets for state companies is a fraction of the level in the private sector.

But there are also benefits. China’s direct control of state companies—and sway with the private sector—gives policymakers a powerful instrument to manage the ups and downs of the economic cycle. Rarely has that been more evident than in the response to the Covid-19 shock. State companies holding on to their employees prevented spiraling unemployment. Tech giants supported the public health response and the credit stimulus. In a crisis, government and business moving together can be a powerful force for resolution.

Behind it all are the benefits of China’s enormous size. As far back as 1776, Adam Smith—the grandfather of modern economics—recognized that the “vast multitude” of China’s population gave it a built-in advantage in the global economic race. If, Smith wrote, China could “learn for themselves the art of constructing all the different machines made use of in other countries,” they would be able to leapfrog ahead of smaller rivals. After Deng kicked open the door to the world in 1978, and even more after entry to the World Trade Organization in 2001, China had ample opportunity to “learn for themselves.” By directing the resources of the state to acquire new technologies, and then scaling them to China’s massive domestic market, industrial planners were able to give Chinese companies a competitive edge first in textiles, then metals, and now high-speed trains, solar panels, and nuclear power.

That story isn’t over. China’s GDP per capita is just a third of the level in the U.S. That means ample room for continued catch-up growth. As China focuses its attention on the technologies of the future—from electric vehicles to industrial robots and artificial intelligence—the annual pace of growth could stay close to 5% through 2025 and end the decade not much lower. With global businesses deeply invested in their China relationship, Trump’s trade war is unlikely to change the trajectory.

“There are lots of Baoshangs,” says one senior banker in Henan province, hinting that other banks could go the same way as the failed lender. Maybe. But as long as the market believes the government will underwrite their operations, they will stay in business. And as long as China continues to grow, the government’s ability to provide that backstop won’t come into question.

One day, a crisis will come along that’s too big even for Beijing to handle. When that happens, the price of allowing problems to fester in the dark will be a meltdown of monumental proportions. One day. But if a once-in-a-hundred-year pandemic doesn’t pop the bubble, the question is: What will? —With David Qu and Yinan Zhao

Adapted from China: The Bubble That Never Pops by Bloomberg chief economist Tom Orlik. Published by Oxford University Press.

©2020 Bloomberg L.P.