Cheap ETFs Are Hot, But BlackRock’s Premium Funds Pay the Bills

Cheap ETFs Are Hot, But BlackRock’s Premium Funds Pay the Bills

(Bloomberg Businessweek) -- It’s no secret low-cost ETFs are big business for BlackRock Inc.

Over the past decade, the money manager’s suite of iShares exchange-traded funds has become the most popular on the planet, amassing almost $2 trillion of client assets along the way.

Its behemoth iShares Core S&P 500 ETF charges a management fee of just 0.04 percent of assets per year, or a scant 40 cents per $1,000. You might wonder how BlackRock makes money charging so little. What’s rarely publicized is just how much of ETF profits—the single biggest source of BlackRock’s revenue—comes from its smaller, high-priced offerings.

BlackRock doesn’t disclose how much it earns from individual ETFs, but calculations by Bloomberg show that almost half the company’s ETF revenue comes from its premium-priced products, which are popular with hedge funds and other professional investors. It’s a stark contrast to its biggest rivals, such as Vanguard Group and State Street Corp., which depend primarily on attracting individuals to its low-fee ETFs.

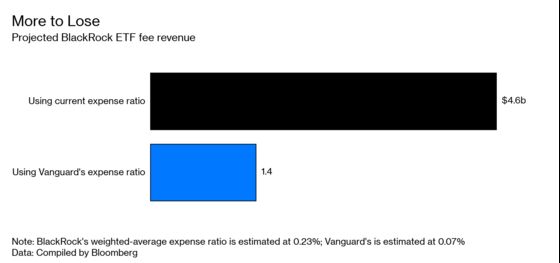

At a time when the fund industry’s seemingly never-ending price war pushes ETF fees closer and closer to zero, relying on high-cost ETFs could be risky. For now, those high-margin ETFs provide a crucial buffer for BlackRock as the industry cannibalizes itself. But BlackRock has that much more to lose if investors abandon them for lower-cost alternatives. If it were to cut ETF fees to match Vanguard across the board, a back-of-the-envelope estimate suggests it could cost the firm upwards of $3 billion in annual revenue.

Melissa Garville, a spokeswoman for BlackRock, said in an emailed statement that “iShares is positioned to serve different client types who value different components of the ETF value proposition.”

While BlackRock has introduced a “core” lineup of low-cost funds in recent years for the buy-and-hold set, Ben Johnson, who heads passive-strategy research at Morningstar Inc., says that institutional investors have long preferred its more established and costlier ETFs because they’re easy to trade. “From BlackRock’s point of view, why kill your golden geese?” he says. “A huge chunk of their fee revenue comes from a small portion of their funds. Rather than strip themselves of millions of dollars in revenue” by cutting prices, the firm can keep profiting by maintaining the status quo.

In recent months, a slew of fund providers, including Vanguard and BlackRock itself, have slashed fees in one of the industry’s most aggressive rounds of price cuts to date. One upstart even went as far as to pay investors to buy into its ETF. And Fidelity Investments already offers some traditional index mutual funds with zero fees. While the low-fee push has fueled the passive-investing boom and made it cheaper than ever to own ETFs, providers are paying the price. Fee revenue has declined and profit margins are down, and some companies have eliminated jobs. Shares of the biggest publicly traded asset managers, which were surging toward records in early 2018, are down nearly 30 percent from those highs.

Consider the difference between the firm’s iShares MSCI Emerging Markets ETF, which goes by the ticker EEM, and its iShares Core S&P 500, ticker IVV. With $35 billion in assets, EEM is just one-fifth the size of IVV. Yet the emerging-markets ETF throws off 3.5 times more in fees. That’s because EEM charges 0.69 percent, or $6.90 per $1,000 invested, 17 times what IVV costs.

For the $178 billion S&P 500 ETF to generate as much in fees as its smaller counterpart, it would need to accumulate more than half a trillion dollars. Put another way, for every nickel that EEM takes in, IVV needs a dollar to produce the same amount of revenue.

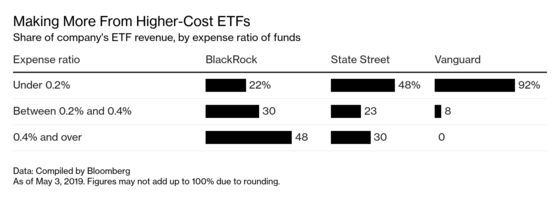

Cash cows such as these make BlackRock stand out. Of the 879 iShares ETFs tracked by Bloomberg, 393 have expense ratios of 0.4 percent or more. While they account for just one-fifth of iShares assets, the funds are responsible for roughly 48 percent of BlackRock’s total ETF revenue.

State Street and Vanguard are skewed in the opposite direction. State Street gets 48 percent of its ETF revenue from its SPDR funds that have expense ratios of less than 0.2 percent. For Vanguard, it’s more than 90 percent.

So how, exactly, has BlackRock been able to maintain these higher-than-average fees? Part of the answer lies in the sheer scope of its offerings. Want to invest in Russian stocks? State Street and Vanguard have nothing to offer you. But iShares has two Russia-focused ETFs, both of which charge more than 0.6 percent. A large number of BlackRock’s premium-priced ETFs focus on a single country or a specific industry.

And even when the competition has a lower-cost product, iShares ETFs are often still preferred by institutions that buy and sell large amounts of shares. They’re more widely traded, making it easier for hedge funds that want to bet against certain sectors to do so. For example, daily volume for BlackRock’s EEM has averaged more than 60 million shares in the past five years. That’s quadruple the amount of its low-cost competitor, the Vanguard FTSE Emerging Markets ETF. An array of derivatives contracts has also developed around some iShares ETFs, catering to professional traders.

“For the trading crowd, expense ratio is almost meaningless,” says Eric Balchunas, an ETF analyst at Bloomberg Intelligence. “If you have one of these super-liquid ETFs, it’s like a diamond, it’s like having beachfront property. Liquidity is the one thing that makes you immune to the fee war.”

Fund providers don’t exactly make it easy to figure out where their ETF profits come from. Take, for example, BlackRock’s regulatory filings. You can find how much money has flowed into its funds, but it’s up to the reader to calculate how much each dollar throws off in fees. (BlackRock discloses expense ratios in the fact sheets for its ETFs—but you’d still have to do the math yourself to determine which ones generate the most revenue.)

In the first quarter, BlackRock rebounded from a rocky end of 2018, and reported assets under management rose to $6.5 trillion. Revenue from base fees, however, declined by the most in seven years, regulatory filings show. BlackRock said in its release that the decrease was due primarily to the market swoon in the fourth quarter and the continued appreciation of the dollar.

The risk is that BlackRock could be exposed to bigger revenue declines if investors, both large and small, begin to shift out of its premium-priced ETFs in earnest.

There are signs that’s starting to happen. Total assets of its iShares MSCI Emerging Markets ETF have declined by roughly 12 percent in the past year. (For context, its share price fell a bit more than 4 percent, meaning a significant chunk of the decrease was because of client withdrawals.) Over that same span, assets in the iShares Core MSCI Emerging Markets ETF, ticker IEMG, surged by roughly $10 billion, lifting its assets under management past $60 billion. At 0.14 percent, its expense ratio is just one-fifth the amount for EEM.

“BlackRock is smart to squeeze out the revenue of keeping the bigger, more liquid funds higher-cost for now,” Balchunas says. “But eventually, the cheaper funds will take over.”

To contact the editor responsible for this story: Michael Tsang at mtsang1@bloomberg.net, Pat Regnier

©2019 Bloomberg L.P.