What Financial Advisers Are Telling Rich Clients About Biden’s Tax Hike

What Financial Advisers Are Telling Rich Clients About Biden’s Tax Hike

(Bloomberg Businessweek) -- President Joe Biden’s proposal to roughly double the capital-gains tax for the rich has put financial advisers in the unusual position of acting as part therapist and part fortune teller. Frantic calls are coming in from clients surprised to see that what they’d dismissed as rhetoric from the 2020 election campaign has come out this week as concrete White House proposals.

Advisers are telling them to keep calm, but they’re also counseling to prepare for action—bringing forward planned asset sales, shedding stock, reallocating investments, and even restructuring income. “Don’t do anything drastic just yet,” Ed Reitmeyer, a partner at accounting company Marcum LLP, is telling his clients. “The world isn’t over because of a higher capital-gains tax rate.”

It may not be over, but it would be changed. For individuals and couples earning more than $1 million, Biden is proposing to increase the tax rate on profits realized when an asset is sold to 39.6%. He also wants to end a tax break that wipes away taxable capital gains at death, allowing families to escape taxes on appreciated assets when they’re inherited.

The current capital-gains tax rate is 20%, one of the lowest levels in the 100-year history of special tax rates for investments. Depending on how the legislation shapes up in the coming months in Congress, the richest Americans can expect larger tax bills in the future. The White House says the new top capital-gains rate—43.4% when including a surtax to help pay for the Affordable Care Act, or Obamacare—applies to 0.3% of taxpayers, or about 500,000 households.

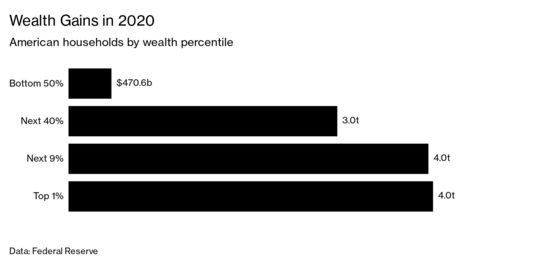

Although relatively small in number, those taxpayers loom large in their share of wealth. Looking at only a slightly larger slice, the richest 1% of households are sitting on as much as $1.5 trillion of unrealized capital gains on equities, according to calculations by Goldman Sachs Group Inc.

“Of course clients are worried,” says Chris Pegg, senior director of wealth planning for Wells Fargo Wealth & Investment Management. Especially concerned: those planning big taxable transactions such as sales of businesses, he says. The uncertain path for the legislation doesn’t dispel the angst, either. “You really can’t tell what’s coming, and yet you have to plan anyway.”

Capital-gains taxes are paid only when an asset is sold, so some investors could plan to hold on indefinitely and perhaps bypass any higher rates under Biden if Republicans win back power in Congress and reduce them in the future. Advisers are counseling those needing to move sooner, or who are less optimistic about future tax cuts, to think about speeding up transactions or to look at ways to minimize the bite.

“We may be in a position to convince our clients to sell down some of those holdings and pay capital gains at a lower rate before those tax rates double,” says Tony Roth, chief investment officer of Wilmington Trust Investment Advisors Inc. Speaking on Bloomberg TV last week, he flagged unrealized gains on tech shares in particular as an asset ripe to consider locking in gains.

But some advisers are finding clients hesitant to sell, after years of being told to do anything to avoid triggering a taxable event. “We have one of the lowest capital-gains rates in history right now, but my clients still don’t pay capital gains. They still don’t sell stock. They don’t like taking any gains,” says Austin Frye, a wealth adviser in Miami.

There is some risk in acting too soon. Biden’s proposal is an opening bid. Democrats in Congress are already reshaping the plan, and any proposal has to clear razor-thin margins in both the House and Senate. In all likelihood, any final legislation will be more moderate and include some combination of lower rates or more carve-outs than what’s detailed in the Biden plan.

More alarmingly for the wealthy, Congress also has the power to make the changes retroactive, to the start of 2021 or even earlier. But signs are that’s not the White House’s preference. “Retroactively is generally not favored,” says Todd Simmens, a former legislative counsel to the Joint Committee on Taxation, who now works for accounting firm BDO. “If folks are planning for some changes, it would be safe and prudent to assume that the changes are effective in January 2022.”

One strategy for investors who are convinced their current holdings will keep growing in value: selling, paying the tax at today’s rate, then buying the asset back. This course of action sets a new, higher purchase price that minimizes any future levy, says Todd Morgan, chairman at Bel Air Investment Advisors in Los Angeles. That approach could work well for an asset such as Tesla Inc., whose stock has increased almost 700% since the start of 2020, or Bitcoin, which was just about worthless a decade ago but now tops $50,000.

“Wealthy individuals and investors generally have the ability to hold for as long as they want” and usually borrow against their portfolios if they need money for current use, says Alison Hutchinson, managing director at Brown Brothers Harriman & Co. If the rules change, however, investors may decide to sell before the changes go into effect.

One other new problem the wealthy could face is increased IRS scrutiny, something that has support from both Democrats and Republicans. Biden wants $80 billion for the IRS to strengthen enforcement in the coming decade.

The most obvious way to avoid higher capital-gains rates is to keep income less than $1 million in any given year. Marya Robben, an estate-planning attorney at Lathrop GPM in Minneapolis, says her executive clients may want to shift more income into deferred compensation plans. Pegg at Wells Fargo notes that sales of property or private businesses could be structured in ways that buyers pay sellers over a period of several years, spreading out that income.

As always with complicated regulations, it pays to pore over the fine print. Changes “will be designed with protections” for family-owned businesses and farms, allowing “heirs who continue to run the business” to avoid paying taxes, a White House fact sheet says. “It will be interesting to see how you define these things,” Hutchinson says.

If the tax-hike legislation does pass this year, wealthy investors could have only a couple of months—or even a few weeks if the negotiations drag on long enough—to react before the changes take effect. “You might want to accelerate income. You might want to defer deductions to a time when they would be more valuable,” Pegg says. “If you think you can get the deal done, get the deal done.” —With Tom Keene

Read next: How Bill Hwang of Archegos Capital Lost $20 Billion in Two Days

©2021 Bloomberg L.P.