Biden Is Coming for the Tax Loopholes That the Rich Cherish

Biden Is Coming for the Tax Loopholes That the Rich Cherish

(Bloomberg Businessweek) -- You’d expect taking money from the 1 Percent to be child’s play in a democracy. The 99 Percent have less money than the rich, but they have way more votes. In practice, Robin Hoodism isn’t so simple. Rich people can rightly make the case that they’re already picking up a big share of the nation’s tab for defense, social spending, and everything else. They can argue, more controversially, that raising their taxes will discourage them from working, inventing, and investing, to everyone’s detriment. And if all else fails, they can hire lawyers and accountants to minimize what they owe the Internal Revenue Service.

President Joe Biden is determined nonetheless to raise taxes on the rich, whose share of the national wealth has soared since the 1970s, and he has a strategy to overcome the inevitable resistance. His aim in the American Families Plan is to combine provisions in such a way that the various parts work together to make higher taxes politically defensible and their collection feasible. If he manages to get his package passed more or less intact, many of the most widely used tax minimization strategies will be foiled. The White House promises the plan “will not only reverse the biggest 2017 tax law giveaways, but reform the tax code so that the wealthy have to play by the same rules as everyone else.”

Biden’s loophole-plugging playbook is evident in his proposed changes in how rich people’s capital gains on assets are taxed. The administration wants to raise the tax on capital gains to 39.6% after the first $1 million, making it the same as the rate on ordinary income. When combined with the existing 3.8% Medicare surtax on investment income, the total levy would rise to 43.4%, the highest since the 1920s outside of a blip in 1978. The problem he faces is that capital gains are notoriously hard to tax. They aren’t taxed until the asset is sold, unlike wages, which are taxed when earned. If you don’t sell before you die, you don’t owe any capital-gains taxes, and your heirs will be taxed only on gains that occur from the time they inherit.

Goldman Sachs Group Inc. estimates the wealthiest 1% of U.S. households have as much as $1.5 trillion of unrealized capital gains on stocks alone. If Congress were to raise the tax rate on capital gains but do nothing else, the government’s revenue would fall by $33 billion over a decade, because the rich would hang on to more assets until death, according to an analysis by the nonpartisan Penn Wharton Budget Model at the University of Pennsylvania.

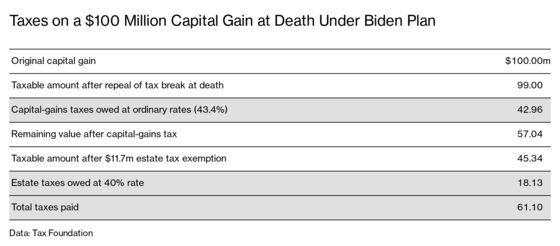

So Biden wants to blow apart that time-honored asset-protection strategy by declaring that from now on, wealthy people won’t be able to erase capital gains by dying—what’s sometimes called the Angel of Death loophole. Under his plan, their heirs would owe tax on an asset’s gains from original acquisition to time of sale. Knowing that a tax is inescapable would cause people to stop postponing realization of capital gains, says John Ricco, associate director of policy analysis at the Penn Wharton Budget Model. That one change would turn Biden’s proposed capital-gains tax increase from a $33 billion revenue loser into a $113 billion revenue gainer, according to Ricco’s calculations. Including the estate tax, the Tax Foundation calculates, the federal government could eventually capture 61% of a $100 million capital gain.

Biden is also trying to block the exits for companies with his previously announced American Jobs Plan. Ordinarily, raising the rate that U.S. corporations pay on their profits to 28% from 21%, as he proposes, would cause companies to shift profits to countries with lower tax rates, depriving the U.S. Treasury of revenue. So the White House proposes coupling the higher tax with an all-out effort to get other countries to sign onto a global minimum tax rate. Under a plan in the works with European nations, if a tax haven country like the Cayman Islands chose not to tax a company’s local profits, the nation where the company was headquartered could collect tax on the profits attributed to the haven, which in theory at least would eliminate the incentive for companies to use tax havens.

President Donald Trump won passage of his Tax Cuts and Jobs Act of 2017, which reduced taxes mainly on the rich, by including reductions in rates for other Americans as well. Biden is limiting his hikes to those earning more than $400,000 a year, with the bulk affecting those making $1 million a year or more. The spending side of his American Families Plan is aimed at the poor and middle class: two years of free preschool and two years of free community college; paid family and medical leave; automatic extension of unemployment insurance in recessions; and making permanent the refundable tax credits for child care and health insurance in the American Rescue Plan, among other things. Those provisions could secure the votes of Democrats who might otherwise oppose tax hikes—and just maybe win over a Republican or two.

To see how ambitious Biden’s tax agenda is, consider how hard it’s been for Democratic presidents to close what’s known as the carried interest loophole—the provision that allows partners at hedge funds and private equity firms to save on taxes by classifying their income as capital gains rather than ordinary income. Raising the tax on capital gains would automatically plug that loophole, but, for good measure, Biden is asking Congress to do away with the concept of carried interest. He also aims to cap a tax break known as the 1031(b) exchange that lets real estate investors defer taxes when they exchange one property for another. And he wants Congress to make permanent Trump’s limit on the size of losses that certain businesses can claim as an offset to their taxable income.

The biggest revenue raiser in the American Families Plan—$700 billion over 10 years—is also the easiest to sell politically: stronger enforcement of tax laws. Because of budget cuts, the share of returns with adjusted gross income of $10 million or more that were examined by IRS auditors fell from 30% in fiscal year 2011 to 7% in fiscal year 2018. The White House cites an academic study published in March that shows the top 1% fail to report 20% of their income. Under-enforcement throws away easy money and erodes compliance across the board by making taxpayers wonder why they should pay when others are cheating.

Even if it passes, Biden’s plan may not live up to supporters’ expectations. The collection of bank account data that’s intended to increase compliance threatens to drown the IRS “in a sea of unproductive information,” Steven Rosenthal, a senior fellow at the Urban-Brookings Tax Policy Center, wrote on May 3. And the increase in capital-gains taxes may fall flat if rich families choose to postpone realizing gains on the chance that a future administration will restore the tax break at death, says Garrett Watson, a senior policy analyst at the Tax Foundation. “They’re trying to look at things holistically, but what’s the backup plan if it doesn’t work?” he asks.

Some Democrats are disappointed that the Biden plan doesn’t broaden the estate or gift taxes. Others from high-tax states such as New York want the president to restore full deductibility of state and local taxes (SALT), which the Trump legislation capped. “I want to get all this stuff done, but no SALT, no deal,” says Democratic Representative Tom Suozzi of New York.

Meanwhile, the forces opposed to raising taxes on the rich are digging in. “The 1 Percent is paying more than 40% of federal income taxes. Isn’t that enough?” Edward Yardeni, president of Yardeni Research Inc., wrote in a note to clients on May 3. Senate Minority Leader Mitch McConnell of Kentucky called Biden’s plan a “liberal wish list.” At the Tax Foundation, economist Erica York wrote on April 30 that “the Biden administration has chosen to pursue inefficient tax increases that would undermine economic growth and reduce U.S. competitiveness.”

Those aren’t the voices Biden is heeding. Instead, he’s listening to the likes of Natasha Sarin, 31, who took leave from the University of Pennsylvania in March to join the Department of the Treasury as deputy assistant secretary for microeconomics. In a November column for Bloomberg Opinion, Sarin wrote that research she carried out with former Treasury Secretary Lawrence Summers suggested stronger enforcement of tax laws “could generate more than $1 trillion in the next decade—more than enough to fund important policy initiatives like universal pre-K and paid parental leave.” A January working paper she co-authored suggested that “raising capital-gains rates to ordinary income levels could raise $1 trillion more revenue over a decade than other estimates suggest.” A trillion here, a trillion there, and pretty soon you’re talking real money.

While economists continue to disagree over taxation, the debate’s center of gravity has moved leftward over the past generation. “It would be a mistake to assume that household and firm behavior does not respond to tax rates, but the consensus estimates of the size of these responses have probably declined in the last 25 years,” writes James Poterba, who heads the National Bureau of Economic Research, in an email: “That is largely the result of an ongoing stream of research studies, many of which find that the impact of taxes on taxpayer behavior are somewhat smaller than earlier studies suggested.” (Case in point: Bloomberg News found that some rich New Yorkers who fled to low-tax Florida during the pandemic are returning.)

Daniel Shaviro, a professor of taxation at New York University School of Law, says when he worked as a congressional staffer on the landmark Tax Reform Act of 1986, the Chicago school ideology of free markets and small government reigned supreme in academia. Biden’s plan for corporate taxation, he says, reflects views that have become more prevalent in recent years. One is that much of the profit earned by big corporations is “excess,” that is, a product of monopoly power. Excess profits can be taxed away without stripping those businesses of the incentive to invest and grow, economists say.

“The academic economic literature on capital taxation has for decades relied on a few canonical optimal tax models that forcefully argued that capital taxes play a minor role in an optimal tax system,” wrote a pair of Swedish economists, Spencer Bastani and Daniel Waldenstrom, in an article published in the Journal of Economic Surveys last year. “In recent years, however, scholars have started to recognize that these models do a rather poor job of explaining actual inequality in wealth and capital income, and new theoretical perspectives and empirical observations are challenging the established conventional wisdom.” In an interview, Waldenstrom says the new thinking could go too far, saying some scholars are ignoring the harm that high tax rates can do. “It really is a pendulum,” says NYU’s Shaviro, who says he agrees with the emerging “progressive consensus” for the most part. “Each era thinks they’re the end of history.”

Biden is trying to make history by reversing a decades-long downward trend in taxation of the rich. He has a bunch of economists on board, and he’s designed a plan that deals with enforceability and political doability. It still might not happen, but the 1 Percent has reason to worry.

Read next: A Tax Code Optimized for White Wealth Leaves Black Americans Behind

©2021 Bloomberg L.P.