America Isn’t Building Enough New Housing

The shortage is being aggravated by low unemployment, which is making it hard to hire workers.

(Bloomberg Businessweek) -- If you’re looking for good news in the housing market, there’s this: Prices aren’t likely to crash the way they did in the historic bust of 2006-09. During the last boom, buyers, lenders, and builders were swept up in speculation, and prices soared even as a flood of new homes came onto the market. That unsustainable combination doesn’t exist today. “A crash is just not something that I see in the cards, even at the local level,” says Greg McBride, chief financial analyst for Bankrate.com.

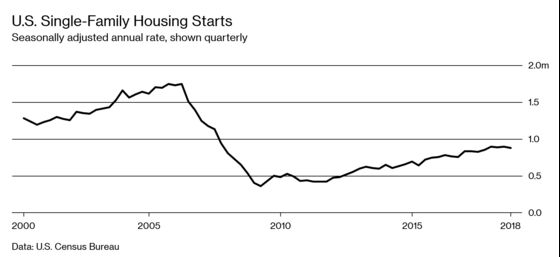

Rather than heading for another bust, we’re still feeling the effects of the last one. Aggressive homebuilders were wiped out, and the survivors are cautious about working on spec. Smaller builders that rely on borrowing can’t supercharge construction, even if they want to, because their bankers are afraid of making loans. Even after a gradual rebound from its nadir in early 2009, the rate of starts on erecting single-family residences remains below the level of the early 1960s, when the U.S. population was less than 60 percent of what it is today.

Instead of an oversupply of homes, there aren’t enough being built. That’s propping up prices at levels that exclude many Americans from ownership. “We are underhoused,” says Aaron Terrazas, a senior economist for Zillow Group Inc.

The shortage is being aggravated by low unemployment, which is making it hard to hire workers. Not-in-my-backyard zoning rules are exacerbating the issue of an already small pool of construction-ready lots, and developers claim regulation is driving up costs. In March the National Association of Home Builders told Congress that edicts involving lead paint, endangered species, and worker safety go too far.

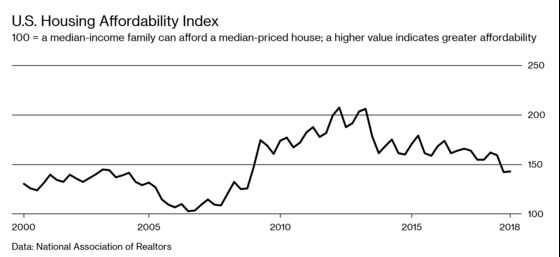

A tight supply has caused housing prices to climb steadily. Owning a home is simply out of reach in some cities. In the Los Angeles and San Francisco areas, the number of houses sold in December was the lowest for the final month of the year since 2007. In Manhattan the median price of a condo has topped out at about $1 million. People who want to buy a place are forced to keep renting, live with their parents, or move to an area with more stock for sale at lower prices. Pending home sales were down 9.8 percent in December, pushing them to their lowest level since December 2013.

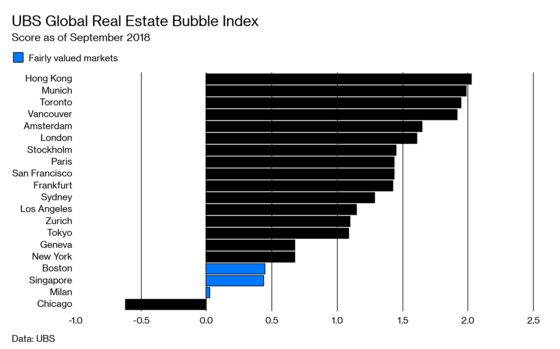

Bubbles, which generally involve overbuilding, are more of a risk in other countries. Last year, Hong Kong was No. 1 in UBS Group AG’s Global Real Estate Bubble Index, followed by Munich, Toronto, Vancouver, Amsterdam, London, Stockholm, and Paris. San Francisco was the sole U.S. city to make the top 10. Below it were Los Angeles, New York, Boston, and Chicago—the only city on the global list rated undervalued (and that was before the polar vortex). The index takes into account price-to-income and price-to-rent ratios, among other factors, to determine how frothy markets are.

But even outside the U.S., there hasn’t been a lot of speculative building, says Jonathan Woloshin, head of Americas real estate investment strategy at UBS Global Wealth Management. “Nobody asked the question back during the bubble, ‘What would happen if prices went down?’ ” he says. “Better questions are being asked today.”

Tighter regulation has ended dangerous practices, such as no-documentation loans, which got people into houses they couldn’t afford. Down payment requirements are mostly higher. These changes have made it harder for people to buy a house, which isn’t necessarily a bad thing. When Fannie Mae, the government-controlled mortgage-buying giant, surveyed housing lenders recently, only 1 percent blamed tight standards for credit and underwriting for the weakness in sales. Forty-eight percent cited an “insufficient supply.”

The government is still cleaning up the mess from bad loans made before the bust. The U.S. Department of Justice has accused many companies, including Quicken Loans Inc. and Freedom Mortgage Corp., of improperly underwriting Federal Housing Administration loans and then filing claims for government insurance after borrowers default. (Freedom Mortgage settled for $113 million in 2016. Quicken, calling the complaint a “shakedown,” is fighting it in court.)

Rising mortgage rates also depressed the market in 2018. While strong economic growth gives more people the wherewithal to buy, it leads the Federal Reserve to raise interest rates, which makes mortgages pricier. Tendayi Kapfidze, chief economist for LendingTree Inc., says higher rates also shrink the inventory of homes for sale: People are less willing to move if their next purchase will have a costlier mortgage. On Jan. 30 the Federal Open Market Committee signaled it will be patient about raising rates further. In 2019, that will just have to count as optimism.

To contact the editor responsible for this story: Bret Begun at bbegun@bloomberg.net, Max Chafkin

©2019 Bloomberg L.P.