A Strong U.S. Economy Will Boost Global Growth in 2019

A Strong U.S. Economy Will Boost Global Growth in 2019

(Bloomberg Businessweek) -- Judging by recent headlines, the global economy is on a wild roller coaster that’s going mostly downhill. There are Brexit, trade wars, Italy’s fight with the European Union, renewed U.S. sanctions on Iran, a Chinese debt bomb, jittery stock markets, intermittent capital flight from developing nations, and more.

The data tell a calmer and happier story. According to the International Monetary Fund, the global economy is on track to grow a healthy 3.7 percent in 2018. That’s exactly how fast it grew in 2017. The IMF’s forecast for 2019? Again, 3.7 percent. It’s a plateau, all right, but a high plateau—call it the Altiplano of economics.

The contrast between the negative daily buzz and positive underlying conditions is sharpest in the U.S., where the expansion of the world’s largest economy has actually strengthened as it’s lengthened: Annualized growth rates in the two middle quarters of 2018 were 4.2 percent and 3.5 percent. In October alone, the economy generated 250,000 jobs.

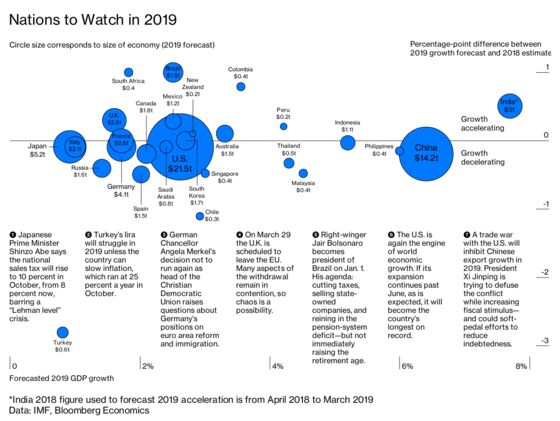

That kind of growth isn’t sustainable in a rich nation with a slow-growing workforce and lackluster productivity growth. Still, if the U.S. makes it past June without a recession, the uptrend will exceed 120 months. That would surpass the 1991-2001 expansion to become the longest since at least 1857, the beginning of records maintained by the National Bureau of Economic Research.

So the outlook for 2019 is better than one might expect given the minicrises breaking out left and right. Strong growth in the U.S. isn’t only good for Americans; it’s good for workers in countries that produce goods and services for sale to the U.S. In fact, the U.S. is largely responsible for keeping global growth ticking along at an even pace despite the slowdown of many other major economies.

On the other hand, the U.S. outperformance has downsides. It puts pressure on vulnerable nations such as Argentina and Turkey, which rely on an inflow of foreign capital. Global investors, who put their money wherever they think it will earn the highest return, are more likely to choose the U.S. over other countries if it’s thriving. Meanwhile, the Federal Reserve is raising short-term interest rates to keep the U.S. economy from overheating, making the nation’s yields increasingly attractive. To compete for funds, vulnerable countries with chronic trade deficits are forced to raise their own interest rates, which suppresses growth. Bloomberg Economics forecasts, for example, that Turkey’s economy will grow just 0.8 percent in 2019.

There could be political problems as well. The U.S. trade deficit is widening because the country’s appetite for imports is growing faster than foreign demand for American products and services. The IMF projected in April that the negative balance on the U.S. current account—the broadest measure of trade in goods and services, plus investment income—will widen to 3.4 percent of gross domestic product in 2019, up from 3 percent in 2018. That would be the biggest gap since 2008.

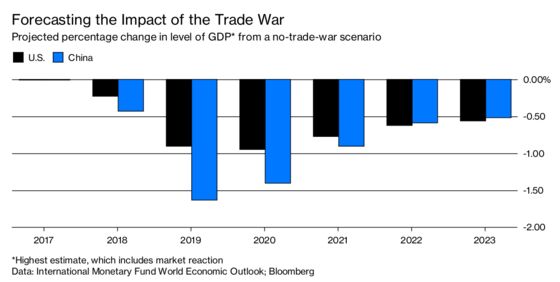

President Trump tends to regard the U.S. trade deficit as evidence of foreign malfeasance. He could impose even more tariffs, which would harm both trading partners and American consumers. At the Bloomberg New Economy Forum in Singapore in early November, 68 percent of the 400 delegates identified trade war as the biggest story for 2019; former U.S. Treasury Secretary Henry Paulson warned of an “economic iron curtain” if the U.S. and China don’t reconcile.

Democrats’ capture of the U.S. House of Representatives in the midterm elections on Nov. 6 won’t moderate America’s pugnacity on trade for two reasons: Trump can act without Congress on trade, and a lot of Democratic lawmakers agree with him anyway. On the plus side, the Congress that sits in January is considered a strong bet to ratify the United States-Mexico-Canada Agreement, Trump’s moniker for the successor to the North American Free Trade Agreement.

For economists, the most important date on the 2019 calendar is March 29, when the U.K. is scheduled to leave the European Union after 46 years. Brexit’s impact on the U.K. economy will have a lot to do with decisions made before then on economic integration between the U.K. and the EU. The worst outcome would be a chaotic “no deal” exit. In August, Matt Hancock, the U.K. health secretary, told drugmakers to stockpile medicines in the country in case there’s no deal and imports are delayed. It’s more likely that some kind of agreement will be struck. Bloomberg Economics predicts the U.K. will grow 1.6 percent in 2019, a bit faster than the estimated 1.3 percent this year. One way or another, Brexit “is going to be extremely difficult,” says Duncan Edwards, chief executive officer of the British American Business Council.

Europe will have more than Brexit to worry about in 2019. European Central Bank President Mario Draghi, who saved the euro in 2012 by vowing to do “whatever it takes,” will complete his term in October, and the jockeying to succeed him is fierce. In Italy, a populist coalition government is defying EU demands to shrink the country’s projected 2019 budget deficit. Other EU members, including Germany, have violated deficit caps without serious consequences, but the European Commission is playing tough with Italy. The leaders of the two populist parties, the League and the Five Star Movement, show no sign of backing down. An angry standoff over deficits could lead to Italy’s following the U.K. out the EU’s back door, but that’s considered unlikely and almost certainly won’t happen in 2019. Bloomberg Economics predicts Italy will expand 1 percent in 2019, continuing a long trend of weak growth. It forecasts Germany growing 1.7 percent.

China’s outlook for 2019 sparkles in comparison, with Bloomberg Economics projecting GDP growth of 6.4 percent. But that would be the lowest figure since the lull following the Tiananmen Square democracy protests of 1989. A big factor is the Trump tariffs, which cover more than half of Chinese exports to the U.S. Another headwind is the government’s effort to shrink the pile of debt accumulated by Chinese families, businesses, and governments. Nonfinancial debt has doubled as a share of GDP since 1998, to 200 percent. If deleveraging threatens to weaken 2019 growth too much, count on the government to ease up on its balance-sheet-cleansing campaign and spend enough to make sure the economy grows at least 6 percent.

Another growth lever China’s leaders can pull is to allow the yuan to depreciate, which makes Chinese goods more competitive against those of rivals such as Japan and South Korea. One U.S. dollar bought 6.9 yuan in early November, up from 6.3 yuan in April. But that strategy has its limits. If the yuan breaches 7 to the dollar in 2019, panic selling could result that would make the currency weaker than authorities want. A weak yuan would raise the burden of dollar-denominated debt—and equally concerning, damage China’s ambition of making the yuan a global reserve currency on par with the dollar and the euro.

Growth in Japan has been strong in recent years, despite a lack of labor force growth. GDP grew at an annual rate of 3 percent in the second quarter. But Japanese governments have a habit of choking off their expansions by raising taxes. Another hike in the sales tax is set for October. That and weakening export growth are two reasons Bloomberg Economics forecasts growth to retreat to 0.9 percent in 2019.

Asia’s growth champion is now India (which, to be sure, remains far behind China in GDP per capita). Prime Minister Narendra Modi needs to keep the expansion rolling as he seeks a second term in 2019. He’s pressing the central bank to worry more about growth and less about inflation—echoing Trump.

And so it goes, with nations’ fates influenced by both global and local forces. In Brazil the outlook depends on whether Jair Bolsonaro, a right-wing former army captain, can get a grip on Latin America’s biggest economy when he takes office as president on Jan. 1. He might take notes from Indonesian President Joko Widodo, another hardscrabble populist, who will run for a second term in 2019. The rupiah cratered along with other developing nations’ currencies in 2018, but it partially rebounded as investors recognized that Indonesia’s trade deficit was a byproduct of investment for growth, not just consumption, says Patricia Perez-Coutts, a lead portfolio manager at Toronto-based Westwood International Advisors.

In September 1998, Federal Reserve Chairman Alan Greenspan said in a speech at the University of California at Berkeley that “it is just not credible that the United States can remain an oasis of prosperity unaffected by a world that is experiencing greatly increased stress.” The U.S. did manage to avoid a recession then, and its momentum is stronger now, not to mention that the stress in the emerging markets is lighter, says Nathan Sheets, a former U.S. Department of the Treasury official who is chief economist for PGIM Fixed Income in Newark, N.J. Still, says Sheets, a big question for 2019 will be “How does this divergence play out?”

To contact the editor responsible for this story: Howard Chua-Eoan at hchuaeoan@bloomberg.net, Eric Gelman

©2018 Bloomberg L.P.