Emerging Markets Meet Tighter Money

Emerging Markets Meet Tighter Money

(Bloomberg Businessweek) -- Emerging markets are suffering their worst slump since 2015. The MSCI Emerging Markets Index entered a bear market in early September after dropping 20 percent from its early 2018 peak. A benchmark index of emerging currencies has dropped more than 8 percent from its high on April 3, while the Bloomberg Barclays Emerging Market dollar-bond index is on track for only its second annual loss since the global financial crisis.

Argentina has made a desperate push to stabilize itself, raising interest rates to 60 percent. Turkey saw its stock market value tumble by $114 billion this year through August. India’s rupee slid to an unprecedented low this month, while Indonesia’s currency hit its weakest level against the dollar since the Asian financial crisis two decades ago.

While each country has its own challenges—Turkey’s president, for example, has unnerved investors by arguing that lower interest rates can pull down inflation—the U.S. Federal Reserve has played a key, if unintentional, role in triggering the stress. It’s all about the Fed’s campaign to move off its emergency policy settings dating from the aftermath of the financial crisis a decade ago.

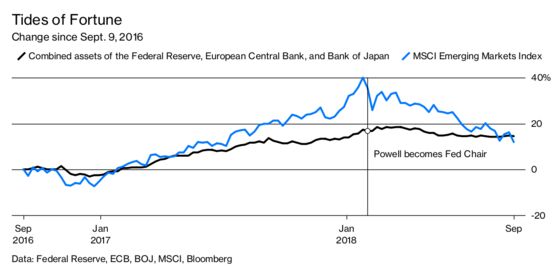

With the American economy enjoying a strong upswing, the Fed has been raising interest rates. It’s also been unwinding its bond-buying policy, known as quantitative easing or QE, by not replacing all the bonds it owns when they mature. In effect, this is shrinking the outstanding supply of U.S. dollars. The Fed’s counterparts in Europe and Japan are simultaneously scaling back their stimulus programs. While the big three central banks pumped an extra $1.82 trillion into the global financial system from January through August 2017, this year the tally is just $99 billion.

The Fed is having an outsize impact because of the dollar’s crucial role in the world economy. As the Fed’s bond purchases pulled down the cost of borrowing in dollars, companies in emerging markets were among those that took advantage of the cheap funding. Developing nations had $3.8 trillion of overseas bonds—mostly in dollars—outstanding at the end of March, up from just $1.3 trillion at the start of 2010.

The Fed’s policy turn has left emerging-nation borrowers scrambling to get more costly greenbacks to service their debt. “You can’t blame what’s happening in emerging markets on growth—like, there’s not some massive China slowdown,” says James McCormick, global strategy coordinator at NatWest Markets in London. But now that the sell-off has started, growth is at risk, too, as countries raise their interest rates to give their currencies support.

The Fed, led by Chairman Jerome Powell, has been pressing ahead, because the U.S. economy is near full employment and inflation is close to its 2 percent target. And from a domestic standpoint, U.S. monetary policy remains in easy mode. Even after repeated increases, the Fed’s 1.75-to-2 percent target range for the federal funds rate is well below the 2.9 percent that policymakers reckon is neutral for the economy.

Emerging markets are facing “a stressful time,” but the U.S. central bank should continue to hike rates given the strength of the American economy, Dallas Fed President Robert Kaplan said at an energy conference in September. Boosted by President Donald Trump’s tax cuts and increased government spending, the U.S. is on course this year to rack up its fastest growth since 2005. Fed officials, including Powell, have long maintained that the best way they can help global financial stability is by keeping U.S. growth on track, while communicating clearly about where policy is heading to avoid surprises.

What might get the Fed to call off its tightening? “It’s quite important what happens to China,” says David Hensley, director of global economics for JPMorgan Chase & Co. in New York. “If it were to look like it were slowing dramatically or to have some real problems with financial stability, that would change the equation.”

Some analysts do worry that the pain in emerging markets is an early indicator of trouble for other kinds of investments as central banks tighten. Although assets in the U.S. aren’t threatened by a rising dollar the way those in emerging markets are, investors are constantly on the lookout for signs that the era of easy money is over. “For a long time we were pleased with the positive impact on asset prices of QE—at the same time, we always harbored this concern of the negative consequences when it was withdrawn,” says Stephen Jen, chief executive of hedge fund Eurizon SLJ Capital Ltd. in London.

If the Fed stays on track, then “we’re going to see the pressure spread” beyond emerging markets, says Jen, who served as an International Monetary Fund economist in the 1990s. But it’s hard to gauge what will happen next, in part because rising rates haven’t led investors to flee Treasury bonds. NatWest’s McCormick and other analysts had expected such a sell-off in the U.S. bond market this year as the Fed tightened. But while Treasuries did drop early in the year, they’ve been largely stable for months.

Emerging markets and Treasuries were just two of the asset classes that benefited from the liquidity expansion engineered by the Fed and its fellow central banks. Corporate bonds saw historically low interest rates, while U.S. stocks have surged. As Goldman Sachs Group Inc. strategists put it in a research note, “all boats were lifted by the liquidity wave.” The unprecedented nature of the Fed’s actions in the past decade makes historical comparisons less reliable, Goldman warns. Their best guess? “A long period of relatively low returns across financial assets.”

To contact the editor responsible for this story: Pat Regnier at pregnier3@bloomberg.net

©2018 Bloomberg L.P.