BlackRock’s Decade: How the Crash Forged a $6.3 Trillion Giant

BlackRock’s Decade: How the Crash Forged a $6.3 Trillion Giant

(Bloomberg Businessweek) -- Our memories of the 2008 U.S. financial crisis primarily concern losses: Bear Stearns, Lehman Brothers, homebuyers, insurers that made reckless bets, and American taxpayers who shouldered billions of dollars in bank bailouts. What about the big wins? One stands out.

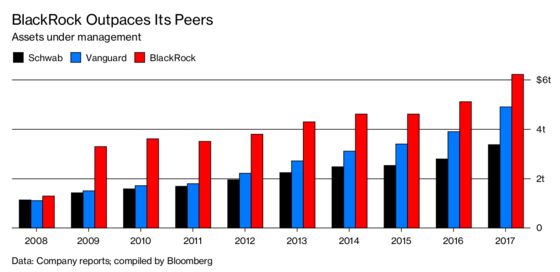

BlackRock Inc., the world’s largest money manager, may never have grown as far and as fast as it did without the unprecedented changes brought about by the recession. The business now towers over its competitors; its $6.3 trillion in assets under management exceeds the size of Germany’s economy.

The story of how BlackRock reached its current position is also the story of the financial industry over the past 10 years. The rise of exchange-traded and index funds and low-fee investing; lower risk tolerance on consumers’ part and higher anxiety within institutions; the government’s scramble to understand this crash and prevent future ones—all of these played to BlackRock’s benefit.

BlackRock declined a request to interview Chief Executive Officer Larry Fink or any company executive for this story. Asked to comment on how the crisis shaped 10 years of growth, BlackRock spokesman Brian Beades offered, “We have always worked to anticipate our clients’ changing needs, and we deliberately evolve our business to meet them.”

The tale of that evolution post-crisis begins with Barclays Plc, which was looking to boost its capital reserves after rejecting U.K. government bailout money. The bank put up one of its crown jewels for sale: the iShares ETF unit, part of the fast-growing, San Francisco-based fund management subsidiary Barclays Global Investors Ltd. (BGI).

BlackRock was no stranger to transforming itself through deals, including previous acquisitions of Merrill Lynch Investment Managers and State Street Research & Management Co. When iShares came up for sale, BlackRock was able to seize the opportunity in a big way, sweeping in with a $13.5 billion cash and stock offer—not just for the ETF unit, but for all of BGI. “They were in a position to play offense while everyone else was scrambling,” says Kyle Sanders, an analyst at Edward Jones & Co.

The 2009 deal more than doubled BlackRock’s assets under management and has proved hugely valuable since: Riding a wave of investment in passive products, iShares had $1.8 trillion in assets as of the end of June. That gives BlackRock a commanding lead on its closest competitors, Vanguard Group and State Street Corp., which had about $936 billion and $639 billion in ETF assets, respectively. IShares accounted for 28 percent of BlackRock’s assets under management at the end of 2017, according to the company’s yearend report. Plenty of growth potential remains: ETFs are still nascent outside the U.S. The company predicts the global market for the funds will more than double by the end of 2023, to $12 trillion, driven by continued downward pressure on financial advisory fees and investors’ rising willingness to use bond ETFs for easy exposure to fixed-income markets.

At the same time, as the U.S. financial system was struggling to get back on its feet, BlackRock found new opportunities to sell its financial risk software, known as Aladdin. Called an “X-ray machine” for financial portfolios by BlackRock Chief Operating Officer Rob Goldstein, Aladdin can predict what a variety of worst-case scenarios would do to a portfolio, including how a 2008-style crash would affect a client’s holdings today. Its users include pension funds, insurance companies, and competing asset managers who pay to license Aladdin based on which of its capabilities they use.

By 2010, the software already was a vital growth area for BlackRock. “We’re having more conversations with more institutions as they reassess what they need under this new regulatory environment,” Fink said during an earnings call that year. In the throes of the recession, Aladdin was used on about $7 trillion of positions, according to a report released by the company. Today it watches over more than $18 trillion. Thirty percent of Aladdin business revenue comes from outside the U.S. BlackRock’s technology unit, of which Aladdin has become the linchpin, saw about 12 percent compound annual growth over the past five years, driven in no small part by network effects—few rivals can match its reach. Technology remains just 5 percent of overall revenue, but Fink told Bloomberg Markets last year that he’d like to see it grow to 30 percent by 2022.

The most significant development in BlackRock’s business, however, may have been the one least likely to show up in its balance sheet: The crisis gave it new clout and gravitas. Fink understood the complicated derivatives that tanked the financial system better than most; his early career was spent structuring and trading mortgage-backed securities, the same kinds of products that triggered the collapse. When the New York Federal Reserve needed a firm to manage Bear Stearns’s portfolio of toxic assets, it turned to BlackRock—not just because of Fink’s stature, but also because it lacked the conflicts of interest a bank could have had in accepting the job. Timothy Geithner, who was president of the Federal Reserve Bank of New York before becoming U.S. Treasury secretary in 2009, maintained close contact with Fink. In one 18-month period from 2011 to 2012, he was in contact with Fink more than any other corporate executive, according to a Financial Times analysis of his publicly available diary.

Fink’s influence didn’t hurt when BlackRock and other asset managers worked to convince the Financial Stability Board, a global regulatory body whose members include the Federal Reserve, that their business shouldn’t be deemed “too big to fail.” The designation comes with higher capital requirements and recurring stress tests. Because they manage other people’s assets, the argument went, they don’t take the kind of high-stakes bets with house money that led banks to seek bailouts.

BlackRock’s elevated profile on Wall Street remains evident. When Fink wrote CEOs a letter earlier this year warning that they should be able to explain how their companies contribute to society, it made international headlines. He routinely meets with world leaders, including in July, when he participated in a dinner U.K. Prime Minister Theresa May hosted for President Donald Trump.

Yet BlackRock hasn’t entirely avoided scrutiny—its cozy relationship with Washington officials has been a source of more attention. The Campaign for Accountability, a Washington, D.C.-based organization, launched a project in June tracking the revolving door of BlackRock executives in and out of halls of power; these include Brian Deese, a climate adviser to the Obama administration who joined BlackRock to run sustainable investing in 2017, and Carol Lee, who went from BlackRock’s compliance department to be securities compliance examiner at the U.S. Securities and Exchange Commission last year. “At BlackRock, understanding local market, policy, regulatory, business, and investment dynamics is integral to serving our clients,” says Beades.

BlackRock’s post-crisis success might be easy to overlook, especially as it’s competing with government-reconstituted giants including JPMorgan Chase & Co. On top of that, private equity firms have vastly increased the scope of their investments in the last decade—particularly Blackstone Group LP, the firm BlackRock spun out of—and tech companies such as Google and Amazon.com Inc. have begun flirting with asset management.

Despite the fierce competition, BlackRock’s growth is among the starkest examples of how a financial company can build itself into an empire, even as the system is upended. With the Trump administration’s continued rolling back of protections put in place after the 2008 recession, that skill may yet prove its value again.

To contact the editor responsible for this story: Jillian Goodman at jgoodman74@bloomberg.net

©2018 Bloomberg L.P.