Zion Prayers Align With This Rally’s Destiny: Taking Stock

Zion Prayers Align With This Rally’s Destiny: Taking Stock

(Bloomberg) -- S&P futures would likely be higher this morning given the relatively positive developments that are emanating from trade discussions, but a few key hiccups are holding it up.

Nike and JNJ ran into some overnight issues weighing on shares (the former having one of its shoes split in a very high-profile manner with the #1 NBA draft prospect Zion Williamson suffering a mild sprain as a result of what was a nationally televised mega-matchup; the latter is staring down subpoenas and inquiries on its talc baby-powder products from the Justice Dept and SEC). Shares in both are down nearly 2%.

Otherwise, there were a few decent earnings reports (save what appears to be some company-specific woes at cyber security player Carbon Black) including hospital operator Community health, cruise line player Norwegian Cruise Line (up 5% thus far) , Avis Budget and purported M&A target Jack in the Box. For the rental cars, however, Morgan Stanley says its time to "fade another rally" as there was no new reason to get bearish -- signs a potential squeeze could arise. Short interest in Avis stood at 14% of float, while the short interest in peer Hertz neared 37%, according to financial analytics firm S3 partners, likely accounting for the outsized moves pre-market in the names (CAR +10%, HTZ +6% in sympathy).

Other potential earnings on the docket that may serve up interesting developments include gambling and entertainment facility operators Caesars Entertainment and Boyd Gaming in the post market. The former not only services thousands of hotel rooms, but also serves as a hotel for hedge funds (nearly 43% of shares are held by hedge fund managers, according to data compiled by Bloomberg), and Icahn’s disclosed interest just two days ago adds to the intrigue that began last year with Golden Nugget casino owner Tilman Fertitta’s voiced interest.

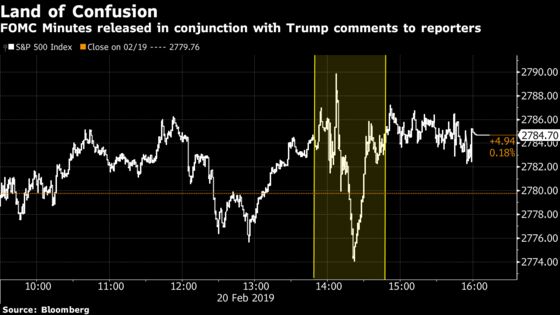

FOMC’s (Dovish) Dud

That’s not a nod at the former NY Fed President, but instead at the minutes that had captivated the market action for much of this holiday-shortened week. Given the unorthodox nature of the release (no prior press lock-up, which meant the release was being parsed by all participants in real time vs the controlled release of media outlets), meant we could observe the chaotic mental gymnastics of aggregate market (is it dovish? too hawkish? how’s growth? inflation? jobs? squirrel!).

Adding to the confusion was President Trump’s simultaneous meeting with reporters that in many cases could have been overlooked, in which he threatened to levy car tariffs on EU imports if a trade deal could not be reached. Given that the threat comes days after he received a report from the Commerce Dept. that is widely believed to serve as justification for said tariffs in the instance in which it is desired, the comments may carry leverage. The contents of the report are as of yet unknown.

But when the dust settled, we were back to where we started in the S&P. Goldman Sachs analysts wrote that their probability models were unchanged, with the baseline expectation of one hike in 2019 (a net hike of 0.6). We were informed of incremental nuggets about how the FOMC had to revise down its growth forecasts just one month after its latest forecasts, downside risks had increased thanks to concerns over trade, fiscal policy and the Government shutdown and that officials were generally unsure on the need for rate hikes in 2019. On the balance sheet issue, minutes stated that, “almost all participants thought that it would be desirable to announce before too long a plan to stop reducing the Federal Reserve’s asset holdings later this year."

Seeking Affirmation

And while we’re on the topic of duds, the bally-hooed CAGNY conference this week has proved to be much ado about nothing, with countless affirmations of prior views, though there are still tea leaves out there to be read.

GIS, Kellogg, Hershey, JM Smucker, and cigarette makers Philip Morris and Altria all reaffirmed their expectations, and to some extent it was not a surprise. Bernstein analysts wrote that with Tuesday’s presentations, "it was telling" that just two firms presented (on what is normally a busy day) given the ongoing disruption in packaged food.

That disruption in packaged food isn’t limited to that product vertical. Waves are also being made at both cigarette and beverage companies. Constellation Brands, which has made investments in cannabis company Canopy Growth, plummeted into the close, citing weaker than expected beer sales. PM and MO, though having both reaffirmed, still led in the top sub-subsector of performance Wednesday, as Altria defended its stakes in marijuana and vaping companies as areas of growth. Household products names Clorox and Procter & Gamble are due to present later today.

Clean Sox

Results later today from IT juggernaut Hewlett Packard Enterprise should help provide a taste of the server and hyperscale environment into January, after the debacle we witnessed with Nvidia and Intel in the server supply chain. The cautious narrative was briefly erased when Microsoft and Alphabet later demonstrated that cloud spending was alive and well, and most recently, when Arista Networks’ results were "better than feared." The Philadelphia semiconductor index has broadly shaken off the growth concerns from Asia with its rebound, sitting just 7% below its all time highs set in March of last year. Gains seen Wednesday can partly be attributed to Analog Devices, which beat most analyst estimates for the first quarter.

RBC analysts last week highlighted that concerns surrounding hyperscale spending weren’t materializing -- at least when it came to Arista’s results for the period ended December. The “cloud titan” group was strong, and RBC analysts led by Mitch Steves wrote that the networking giant was “seeing traction on the enterprise side as well” in a note aptly titled, “If There is a Spending Pause Jayshree Isn’t Seeing It,” in a reference to Arista CEO Jayshree Ullal.

This may set the stage for HPE which has substantively recovered from the 4Q market meltdown, but will now provide that insight into January. Keeping in mind in the above described FOMC minutes, the latest U.S. economic forecasts were trimmed from just a month prior. Morgan Stanley analysts expect a "mixed quarter" for the memory and server manufacturer. Analysts led by Katy L. Huberty see downside risks for results, citing macro concerns and recent results from NetApp that discussed a slowdown in purchasing in January. The average price target among analysts tracked by Bloomberg anticipate just 5% upside over the coming 12 months.

Sectors in Focus Today

- Mining sectors after the base metals popped Wednesday given the dollar index is vulnerable to Fed speak-related volatility; TXG CN, HL, MUX, NEM report pre-market, with ELD CN post market

- Health care supply chain after a trio of misses wiped out billions in market cap in the segment Wednesday (thanks to CVS, OMI, HSIC). Look for possible relief rally given the magnitude of the losses

- Lithium players SQM, LTHM after Albemarle beat 2019 adj. EPS estimates

- Accessory players after Garmin yesterday soared 15% as smartwatches were "on fire"

- UK exposed firms after Fitch warning the UK’s AA rating could be cut

- Student loan-exposed firms (SLM, NNI) after Canyon Capital withdrew its expression of interest to acquire Navient

- Optical stocks after LASR reported a forecast that missed expectations

- Hospitals after small cap CYH reported (though enterprise value sits at more than $14B)

Notes from the Sell Side

Biogen shares are indicated lower after a cut at Stifel to hold from buy as the firm now faces elevated risk from the Roche crenezumab futility and Tecfidera IPR institution. Analyst Paul Matteis writes that there’s now decreased confidence in Alzheimer’s, which, combined with a potential Tecfidera legal issue, conviction is now lacking. Price target goes to $346 from $397 (Bloomberg avg $382).

Homebuilders are the subject of cautious commentary at Wedbush, with Lennar and DR Horton being downgraded to neutral from outperform. DR Horton shares are indicated lower by nearly 1% as Jay McCanless cites the recent recovery in the shares and current valuation. The recent pullback in mortgage rates has likely provided a boost to shares in the stocks, he writes, and though the catalyst may remain for some time, McCanless is skeptical any new catalysts will emerge to nudge his price target much higher.

Tick-by-Tick Guide to Today’s Actionable Events

- CAGNY conference

- Barclays Industrial Select conference

- Citi Global Industrials conference

- 7:50am -- Fed’s Bostic speaks on the economy and monetary policy

- 8:30am -- Feb Philly Fed business outlook, initial jobless claims, continuing claims,

- 8:30am -- Dec Durable goods

- 8:30am -- CAR, WEN earnings call

- 9:00am -- RGNX analyst and investor meeting; PG at CAGNY conference

- 9:10am -- ADT at Barclays Industrial Select conference

- 9:45am -- Bloomberg consumer comfort, Feb Markit PMI

- 10:00am -- Jan leading index, Jan Existing home sales

- 10:00am -- NEM, NCLH earnings call; CHD at CAGNY conference

- 10:55am -- SHW at Barclays Industrial Select conference

- 11:00am -- CYH earnings call

- 11:30am -- JACK earnings call

- 2:00pm -- SPB at CAGNY conference

- 2:03pm -- Tiger Woods tees off at WGC-Mexico Championship

- 2:45pm -- CMI at Citi Global Industrials conference

- 3:00pm -- CLX at CAGNY conference

- 3:30pm -- JBHT at Citi Global Industrials conference

- 4:00pm -- INTU, FSLR, CZR earnings; THS at CAGNY conference

- 4:03pm -- DBX earnings

- 4:05pm -- HPE, ZG earnings

- 4:20pm -- ROKU earnings

- 4:30pm -- INTU, FSLR earnings call; BIDU earnings

- 4:40pm -- ED earnings

- 5:00pm -- HPE, ROKU, ZG, DBX earnings call; KHC earnings

- 5:30pm -- KHC earnings call

- 5:45pm -- CZR earnings call

- 8:15pm -- BIDU earnings call

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.