Zambia’s Debt-Relief Vote Sets Tone for Stormy Restructuring

Zambia’s Debt-Relief Vote Sets Tone for Stormy Restructuring

(Bloomberg) -- Zambia looks set to move closer to being Africa’s first sovereign default since the onset of the coronavirus pandemic, with bondholders expected to reject a request to put off payments for six months.

A key vote Tuesday by holders of Zambia’s $3 billion of Eurobonds will also be keenly watched by other poor nations considering how to involve commercial creditors in debt-relief talks. The southern African nation said it needs breathing space while it plots a restructuring strategy that strikes a balance between bondholders and bilateral, mostly Chinese, lenders.

A core group of Eurobond holders has already said it wouldn’t support the proposal without assurances of transparency and a credible plan to get the International Monetary Fund’s endorsement. Rafael Molina, an adviser to the group, declined to comment on Monday, stating that its expectations and position had not changed.

“In all likelihood the vote will fail,” said Anthony Simond, a portfolio manager at Aberdeen Standard Investments in London, which has a “small position” in Zambian Eurobonds. “The feeling is that the Zambians haven’t given bondholders sufficient evidence that it has a coherent fiscal plan that brings debt sustainability back on track.”

He wouldn’t comment on how Aberdeen would vote.

While the coronavirus pandemic added to Zambia’s woes, with the economy forecast to shrink this year for the first time since 1998, its debt problems started years earlier.

The government borrowed heavily since 2012, building up nearly $12 billion in external debt and ignoring warnings from the IMF of growing debt distress risks. It took money, often from state-owned Chinese lenders. to build roads, schools and even military housing.

Zambia skipped a $42.5 million coupon on Oct. 14, leaving it 30 days’ grace to make the payment before triggering a default that would allow bondholders to demand immediate repayment of the principal.

Eurobond holders have raised questions over the transparency of loans from Chinese banks, and fear any relief they grant to Zambia could go to servicing these debts, or be used to finance more projects aimed at winning votes in elections set for August. Zambia said it will treat all creditors equally, and by April had already accrued $201 million in arrears to Chinese lenders.

“The Zambian authorities should engage with the bondholders and be clear about what it is they are trying to achieve,” said Richard Briggs, an investment manager at GAM Ltd. in London, which holds the country’s Eurobonds. “The coupon delay in isolation, without a plan, doesn’t do that, particularly given a lack of detail around the progress on an IMF program and visibility on Chinese lending.”

The six-month payment holiday would cover about $120 million of coupons. Zambia’s first principal repayment, of $750 million, is due in 2022. Without relief, the government would also have to pay $854.3 million to banks in the world’s second-largest economy through the end of next year.

‘Rubber Stamp’

It’s not a given that bondholders will refuse Zambia’s payment deferral request. Because the government already skipped last week’s coupon payment, tomorrow’s vote could just be a “rubber-stamping exercise,” according to Ilke Smit, an economist at Pinebridge Investments Europe Ltd. in London.

“We don’t think there will be serious objections to the government’s proposals,” she said. “In the event of a successful restructuring and a prospective IMF deal, its fundamentals can improve quickly.”

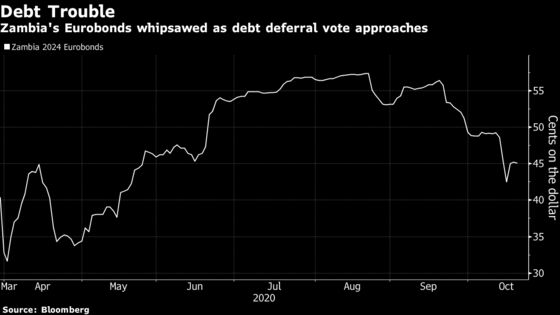

Zambia’s $1 billion of Eurobonds due 2024 slipped on Tuesday after gaining for a second day on Monday. The notes dropped to a four-month low last week and are trading at less than half their face value.

The voting starts at 10 a.m. in London, with separate polls for each of the three Eurobonds. Should holders reject the request, the road to restructuring may be long. The elections, in which President Edgar Lungu will seek a fresh mandate, will make a quick deal with the IMF difficult.

“Politics will play a major role as the presidential election in 2021 could limit the government’s fiscal efforts that would be required for an IMF program and a successful negotiation with creditors,” said Federico Kaune, the New York-based head of emerging markets fixed income at UBS Asset Management. “Negotiations won’t be easy.”

©2020 Bloomberg L.P.