Yidai Shuts Shop Amid China Crackdown on P2P Lenders

Yidai is the latest to exit the business as China reins in its $176 billion experiment with this riskier form of financing.

(Bloomberg) -- Yidai, an online peer-to-peer lending intermediary, is the latest to exit the business as China reins in its $176 billion experiment with this riskier form of financing.

The company set up a committee to start refunding its lenders after “months” of losses, Yidai said in statements over the extended holiday weekend. It has about 32,000 lenders with an outstanding principal balance of 4 billion yuan ($581 million), and expects to repay them in three-to-five years.

Yidai, which received investment from SB China Capital (SBCVC) in 2014, also said shareholders and executives aren’t allowed to leave the country.

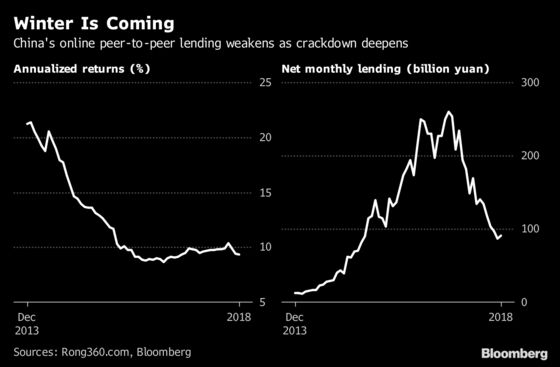

Chinese leaders are dramatically shrinking a market that spawned the nation’s biggest Ponzi scheme, protests in major cities, and life-altering losses for thousands of savers. Authorities are planning to wind down small- and medium-sized P2P lending platforms nationwide, people with knowledge of the matter had earlier said.

Tougher regulations and rising bankruptcies have spooked investors, and lending on those online platforms has plummeted, according to data from Rong360.com, a provider of information about financing and loan products. Analysts from China International Capital Corp. said they expect the number of P2P lenders to contract to fewer than 200 in three years’ time.

The move is in line with President Xi Jinping’s broader crackdown on shadow banking. In China, P2P platforms comprise one of the riskiest and least regulated slices of the system. The lack of oversight allowed for world-beating growth, with outstanding P2P loans ballooning from almost nothing in 2012 to 1.22 trillion yuan in December 2017.

To contact the reporter on this story: Jeanette Rodrigues in Mumbai at jrodrigues26@bloomberg.net

To contact the editors responsible for this story: Sam Mamudi at smamudi@bloomberg.net, Jeanette Rodrigues, Arijit Ghosh

©2019 Bloomberg L.P.