(Bloomberg Opinion) -- The American Economic Association’s new online discussion forum gives the outside world the occasional glimpse of the way economists talk among themselves about important policy issues. One example is a recent conversation thread initiated by Massachusetts Institute of Technology professor and former International Monetary Fund chief economist Olivier Blanchard and joined by several other prominent researchers. The topic was whether low interest rates had led to excessive risk taking.

With rates finally rising, the question might not be of immediate importance. But it was a crucial question during the recovery from the Great Recession, and will inevitably be brought up again the next time a recession strikes.

From the end of 2008 through 2015, the Federal Reserve kept short-term interest rates at or near zero:

The Fed also engaged in successive rounds of securities purchases, or quantitative easing, and used other operations to lower long-term rates. At the time, monetary hawks like Federal Reserve Bank of Philadelphia President Charles Plosser and Stanford University economist John Taylor warned that low rates could encourage investors to “reach for yield,” putting their money into risky high-return companies and financial products that would later crash in value, harming the economy.

Some research does show that low rates induce people to put their money into riskier investments. This tends to lead to higher absolute returns, but lower risk-adjusted returns.

But as Harvard’s Jeremy Stein points out in Blanchard’s thread -- and as many others have pointed out before -- this is exactly how lower rates are supposed to pull an economy out of a recession. There are some projects out there -- a new office building, perhaps, or an oil-drilling company -- that are so risky that when interest rates are high, investors would prefer to avoid these projects and play it safe by investing in government bonds.

When the central bank drives down the rates on government bonds, investors will tend to look on those marginal projects more favorably and put their money into things they turned up their noses at before. As a result, new office buildings will get built, new oil companies will start drilling -- and demand for workers will rise, giving the economy a lift. Some of those projects will inevitably fail -- some offices will sit vacant, some oil companies will collapse when oil prices fall. But investors presumably know that going in. Presumably, they also know that when the Fed eventually tightens, more of those risky project will fail, since higher rates make it harder for borrowers to service their debts.

That’s the simple, textbook case. But it’s also at least theoretically possible that investors aren’t so rational. Instead of measuring the discounted cash flow from a potential investment, as textbooks say they ought to, most investors probably use rules of thumb. If those rules of thumb don’t adjust when interest rates change -- for example, if investors keep believing that they ought to be able to make a 10 percent return even when interest rates fall from 5 percent to 0 percent -- then low rates can induce them to take more risk than would be rational. Claudio Borio of the Bank for International Settlements basically makes this case in response to Blanchard.

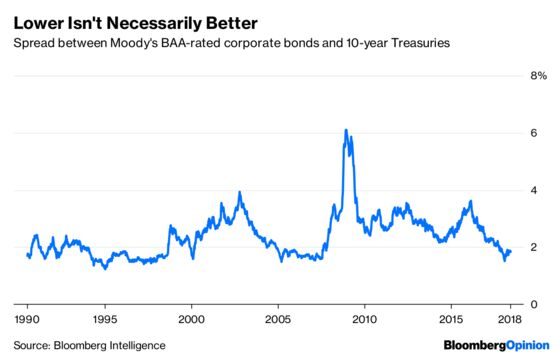

History, however, doesn’t seem to bear out these worries. Japan has had extremely low interest rates since its land and stock bubbles burst three decades ago, and it hasn’t experienced any bubbles or crashes during that time. As for the U.S., low rates and quantitative easing might have compressed credit spreads (the difference between risky bond rates and safe bond rates) a bit in 2013 and 2014, but those spreads soon rebounded:

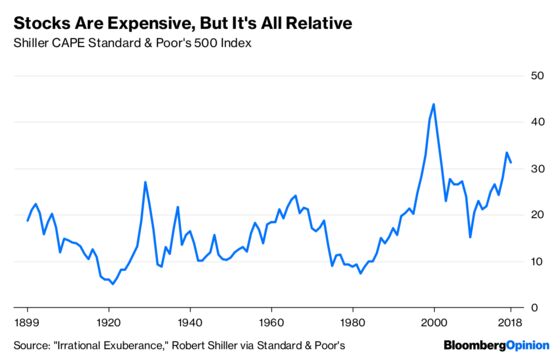

As Ricardo Caballero of MIT points out on the AEA discussion thread, U.S. stocks have risen to historically high earnings multiples during the period of low rates:

During the recovery, there were in fact a few bubbles. Gold rose in 2010 and 2011, then crashed in 2013. There might have been a very minor bubble in tech startups in 2013 and 2014. Bitcoin had some small bubbles in 2011 and 2013. And in 2015-16 there was a mild slowdown in economic activity, probably due to a pullback in the energy industry. But nothing big enough to justify the worries of people like Taylor and Plosser.

Interestingly, it’s only since the recovery turned into a boom, and interest rates started to rise, that appetite for risk has really taken off. Credit spreads, after rebounding in 2015 and 2016, have begun to fall in earnest, approaching dangerous levels. Stocks look more overvalued now than when QE was in full swing. Some research also indicates that reaching for yield is most pronounced during boom times, as irrational exuberance permeates the national mood.

So the answer to whether low rates encourage excessive risk-taking might depend on when those low rates happen. It seems clear that keeping rates low in response to sluggish growth won’t turn an economy into a frenzied bubble. But during an expansion, it might behoove central banks to be a little less cautious about raising interest rates.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2018 Bloomberg L.P.