France's Bad Boy of Telecoms Joins the Geriatric Set

(Bloomberg Opinion) -- Xavier Niel is supposed to be the bad boy of French telecoms. He never finished college, once ran an online sex-chat service, and shook up incumbents like Orange SA with cheap pricing when he launched Free Mobile in 2012.

That makes one element of his push to extend control over Free’s parent Iliad SA particularly surprising: the implicit admission that the Paris-based company is becoming just like any other boring telecom company. It's an overdue acknowledgement of market realities.

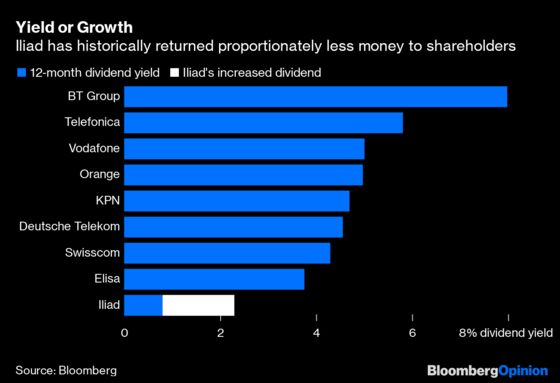

It all comes down to the dividend. Mobile carriers have appealed to investors over the past decade not for their growth prospects but their generous dividend payouts. European telecommunications firms will have an average dividend yield of 5% this year, according to estimates compiled by Bloomberg. That compares with the 3.3% average of the broader Stoxx 600 Index of European companies.

Iliad has differed from the crowd. Its 12-month yield has averaged 0.8% since 2009. That’s because it promised growth — the stock climbed almost three-fold between 2009 and 2017. But the past two years have been a different story. Before today, the shares had fallen 63% from their 2017 peak as French rivals reclaimed market share from the low-cost upstart.

On Tuesday, Niel announced plans to boost his holding in the firm by as much as 20 percentage points. The complicated structure will see Iliad buy back up to 1.4 billion euros ($1.5 billion) of stock for 120 euros per share, then issue new shares of an equivalent amount that Niel has pledged to buy, in a rights issue to which other shareholders can also subscribe.

At the same time, Iliad announced it would increase the dividend by a chunky 189% to 2.60 euros, bringing the yield to more than 2%. That’s still very much at the low end of its peers but a substantial change in policy, particularly at a time when the region’s giants — Vodafone Group Plc and Deutsche Telekom AG — are cutting their dividends as they anticipate increased spending on 5G networks.

For Niel, it’s a canny way of using the company’s stronger balance sheet to extend his control. Iliad is expecting proceeds of more than 2 billion euros from the sale of infrastructure assets this year. If he increases his stake to above 70% from the current 52%, as the buyback and rights issue might allow, he can expect annual dividend proceeds exceeding 100 million euros. That can help him service the personal debt that he’s likely assuming to fund the rights issue. The move may also strengthen Niel's hand and his financial upside, should the perennial on-again, off-again efforts to consolidate the French market resume.

The steps at Iliad don’t particularly disadvantage existing shareholders financially, even if they do seem to be very much in Niel’s interest. They’re under no obligation to sell, and have already benefited from a jump in the share price, which climbed 18% on Tuesday. Nor does the increased payout significantly weaken the firm’s finances: The dividend payout will top 154 million euros. Net debt of 3.7 times Ebitda will fall closer to 2.5 times Ebitda. And it’s far less outrageous than the self-interested efforts of fellow French billionaire Vincent Bollore and his family to extend control over Vivendi SA. The Bollores are simply carrying out a buyback of the media conglomerate’s shares, then canceling them, leaving the family with a bigger stake without increasing their financial risk.

But for all of Niel’s assertions that the investment reflects his “confidence in the company’s industrial project,” he will likely need Iliad to continue the more generous dividend payouts to service his greater debt. That will gradually chip away at Iliad’s ability to engage in costly price wars to drive market share. Instead, it’s becoming more like its rivals, generating steadier, more predictable returns, rather than promising stratospheric stock growth.

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2019 Bloomberg L.P.