Wirecard Flourished in Regulatory Blind Spot That’s Growing

Wirecard Flourished in Regulatory Blind Spot That’s Growing

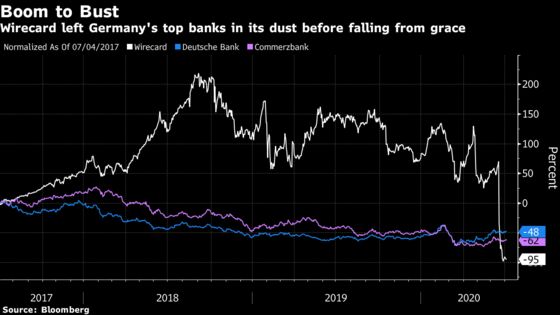

(Bloomberg) -- Wirecard AG’s collapse displayed a growing blind spot for the guardians of the world’s financial system: how do you regulate a firm that acts like bank, but isn’t really a bank?

For years, Germany’s supposed fintech star escaped strict scrutiny because financial watchdog BaFin was focused on its banking unit rather than Wirecard as a whole. With the scandal undermining Germany’s reputation as a place to do business, the government is overhauling who regulates who, but it could also spark a regulatory rethink with consequences for the broader fintech industry.

As banks retrenched after the 2008 financial crisis and spent billions on settling the resulting litigation, rather than new technology, other companies stepped in. Wirecard and competitors like Adyen NV process payments far quicker than traditional banks while also offering clients services to manage their risk and learn more about their own customers. Technology giants like Amazon.com Inc. and Google parent Alphabet Inc. are also increasingly offering financial services.

Swathes of the fintech sector are currently unsupervised, particularly in the area of cryptocurrencies. Around 31% of fintech firms in Europe are not subject to any regulation, according to the European Banking Authority.

“We need regulation that addresses banks and non-banks on a level playing field,” says Benoit Coeure, head of innovation at the Bank for International Settlements, better known as the central bank for central banks. Fintech companies play an important role in wider financial markets and not just in payments, he said in an interview with Bloomberg TV’s Nejra Cehic on Friday.

At issue is whether fintechs and other digital payments firms should be subject to the same type of strict regulation as the banks and financial companies they are trying to disrupt. There are already some regulatory overlaps in many cases but some experts say more gaps need to be covered to ensure the digital companies are supervised as financial firms.

In Europe, a company crosses the line into finance and all the regulatory scrutiny that entails when more than 50% of its business is associated with financial activities like lending and taking deposits, according to the EBA. Banks have faced tougher reporting and compliance obligations since the financial crisis.

Wirecard wasn’t classified as a finance company in previous assessments by BaFin and other institutions. While its German bank and its U.K. unit were supervised by local regulators, oversight of the group company was essentially limited to whether it met the disclosure obligations of a German listed company, watched over by BaFin.

BaFin President Felix Hufeld has described the collapse of Wirecard as a “massive fraud.” But for some, the debate about changing or increasing regulation is a distraction from the failure by authorities like BaFin to enforce existing rules.

A Wirecard spokeswoman declined to comment on Hufeld’s characterization.

“The real issue is that BaFin didn’t use the powers they had already,” said Sven Giegold, a member of the European Parliament for the Green party. “This is negligence by the supervisor, so this doesn’t need a new approach to financial regulation of fintechs.”

While classifying Wirecard as a financial company would have given BaFin more access, the regulator was already able to pursue red flags at Wirecard. BaFin received documents alleging irregularities at the company in January 2019 and asked Germany’s accounting watchdog to look into it. Yet that group failed to deliver a report before Wirecard itself disclosed the 1.9 billion euros of missing cash in June this year. BaFin has also been faulted for moving too slowly.

Hufeld has acknowledged that BaFin is among institutions that fell short in the supervision of Wirecard and has pledged to review any failings. Germany’s Justice Ministry canceled its contract with the accounting enforcement watchdog, known as FREP, while the Finance Ministry has said investigative powers should be handed to BaFin.

To get a license to process payments, companies like Wirecard need to provide documentation on governance to national regulators and are required to keep their customer funds separate from their own revenues. Management also need to be screened by regulators and the banking arms need to maintain a certain level of financial strength.

“The regulatory framework that’s there is fit for purpose,” said John Ahern, a partner at law firm Covington & Burling, who advises clients on financial regulation. “The question is whether the supervision of regulated entities is sufficiently effective.”

Hufeld said he has been pressing the issue of oversight over technology companies for two years, but that ultimately it’s a political decision. Germany took over the rotating presidency of the European Union this month, meaning it could press for changes, although it may be more focused on the response to the coronavirus pandemic.

Wirecard exposed a failure in oversight both by accountants and regulators, but Europe’s regulatory structure also contains gaps which will be more in focus as electronic payments grow, says Huw van Steenis, senior adviser to the CEO at UBS Group AG.

“Europe has been so keen to drive open the payments market to break the banks’ monopoly that the regulatory change has meant that payments firms fall between the cracks,” he said in a Bloomberg TV interview. “Addressing this payments regulatory gap is going to be ever more important in the post-pandemic economy.”

©2020 Bloomberg L.P.