Dollar Funding Squeeze Set to Get Worse After Basis Swap Blowout

Where Have the Dollars Gone? Funding Squeeze Enters Crunch Time

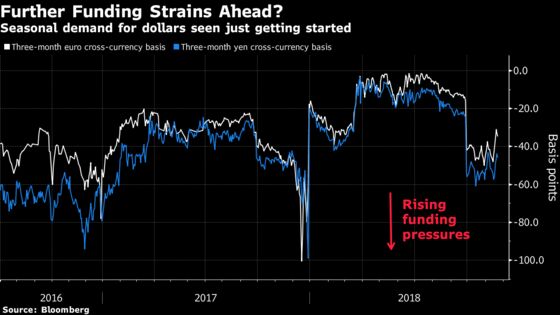

(Bloomberg) -- Dollar funding strains took center stage earlier than normal this year, and if the recent past is any guide, the worst of the squeeze is still to come.

Further efforts by banks to shore up their balance sheets are likely to exacerbate a year-end shortage of the U.S. currency in the financial system, according to firms including Bank of America Corp. and TD Securities. That’s even after the three-month cost to convert payments from euros into greenbacks using cross-currency basis swaps swelled in late September by the most since 2009, as market participants sought to preempt what’s now become an annual year-end crunch.

The dash for dollars is set to reverberate across the globe, making it costlier for companies and banks from Europe to Japan to source the liquidity they need, while affording investors with U.S. currency to spare the chance to turbocharge overseas returns. While few expect a repeat of last year, when the basis blew out to the widest in six years in the final weeks of December, it begs the question -- just how can a world awash in trillions of dollars in greenback liquidity be running short, again?

“Some of our traders see year-end funding levels continuing to show increasing signs of pressure, especially right around the turn,” said Mark Cabana, head of U.S. interest-rate strategy at BofA. “As Libor rates continue to widen, we think that would see similar funding pressures through cross-currency basis swaps.”

Investors can largely blame the Basel III regulatory regime adopted in 2014 for the seasonal rush for greenbacks.

As a result of new capital requirements, global systemically important banks, or G-SIBs, now tend to dramatically reduce their dollar-lending activity in the closing weeks of the year -- mostly in an effort to lower their surcharges. The result is that firms such as JPMorgan Chase & Co., Citigroup Inc. and Morgan Stanley -- among the world’s largest lenders of dollars -- are hoarding greenbacks before they report their balance sheets.

“There’s a real disincentive for some of the biggest banks to lend out dollars over the turn of the year,” said Gennadiy Goldberg, senior U.S. rates strategist at TD Securities. “It’s a profitable trade for them to do throughout most of the year, but by the end of the year, they will in essence try to pare some of that activity to get more favorable regulatory treatment.”

Prior to 2014, abrupt widening episodes were primarily confined to periods of extreme risk aversion, such as in 2008 after the collapse of Lehman Brothers Holdings Inc., and in 2011 amid the euro-zone debt crisis.

Funding Frenzy

On the other side, foreigners have been left holding the bag. Multinationals are forced to pay up for routine business operations, such as hedging their FX exposure. Moreover, overseas firms need to window-dress their balance sheets too. That can be a costly undertaking given the proliferation of dollar-denominated debt overseas, according to Peter Cecchini, chief global market strategist at Cantor Fitzgerald.

“Financial institutions in Europe need to convert euro-denominated assets into dollars in order to match dollar-denominated assets and liabilities,” Cecchini said.

In addition to banks, global bond investors are also feeling the strain. One consequence of the dollar shortage is that hedging costs become more expensive for European and Japanese investors. Benchmark 10-year Treasury yields have dwindled to minus 0.22 percent for yen-based buyers protecting against currency swings. For European buyers, it’s even worse at minus 0.35 percent, near the lowest this year.

The sky-high hedging costs have investors such as Bill Gross and Jeffrey Gundlach suggesting that waning foreign demand for U.S. debt could help drive yields higher.

Yet for those willing to lend out their dollars, the surge in demand means that there’s never been a better time to invest abroad. U.S.-based investors can lock in historically high returns in Europe and Japan after hedging their bond purchases, even though yields in the two markets are among the lowest in the developed world.

Market Risks

Signs of dollar demand are already cropping up elsewhere. The gap between the three-month London interbank offered rate and the overnight index swap rate -- another gauge of global dollar funding costs -- has risen to 33 basis points, from a low of 17 basis points last month. And the rates on 30- and 90-day AA-rated financial commercial paper continue to climb as issuance by foreign banks looking to secure funding over year-end seemingly outstrips demand.

The December squeeze could be more painful than expected if the current turmoil in equity and oil markets worsens as U.S.-China trade tensions continue to linger. TD’s Goldberg says that the seasonal greenback shortage could potentially aggravate any bouts of risk aversion in which banks are wary of lending dollars.

“Let’s say there’s a shock event, there’s an enormous risk-off move, and investors are scrambling for safe havens, trying to raise dollars to shore up their holdings,” Goldberg said. “It’s an extremely difficult environment to do that.”

--With assistance from Liz Capo McCormick and Alexandra Harris.

To contact the reporter on this story: Katherine Greifeld in New York at kgreifeld@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Boris Korby, Jenny Paris

©2018 Bloomberg L.P.