What's a Private Company? China Banks Grapple With New Rules

In a country where the state’s influence is felt everywhere, there remains little consensus on what defines a “private” company.

(Bloomberg) -- Some Chinese banks are struggling to comply with unprecedented regulatory targets for credit to private companies because they aren’t sure who to lend to, a sign that authorities’ urgency to reverse an economic slowdown is muddying policy.

The confusion stems from China Banking and Insurance Regulatory Commission chief Guo Shuqing’s statement on Thursday that at least a third of new loans should go to private companies, with the ratio going up to 50 percent in three years. The missive sent bank stocks falling.

The problem, according to senior executives at three banks who spoke on condition of anonymity for fear of alienating regulators, largely boils down to this: In a country where the state’s influence is felt everywhere, there remains little consensus on what, exactly, defines a “private” company. That leaves the new policy open to misinterpretation and even potentially to gaming, they said.

Investors and bank executives alike are concerned that setting specific targets for lending to private businesses -- something authorities refrained from even during the height of the 2008 financial crisis -- could result in a pile-up of bad debts. Bond defaults by non-state companies, an indicator of stress in the private sector, jumped fourfold this year from 2017, Bloomberg-compiled data show.

Authorities sought to mitigate the market fallout on Monday, with official newspapers carrying front-page reports saying there won’t be specific targets for each bank. Yet bank stocks traded in Hong Kong failed to reverse Friday’s tumble.

“The market doesn’t like this policy, and neither do I,” said Chen Shujin, an analyst at Huatai Financial Holdings (HK) Ltd. “While it makes sense to offer a temporary, emergency liquidity backstop to struggling private businesses, it won’t help solve the underlying issues by imposing long-term lending targets.”

The CBIRC didn’t reply to a fax seeking comment.

As U.S. tariffs kicked in over the past months and China’s equity market slumped, President Xi Jinping pledged “unwavering support” for the private sector, which contributes about 60 percent of the nation’s gross domestic product. The sector had borne the brunt of his two-year campaign to reduce risky lending as banks preferred the perceived safety of government-backed borrowers.

Official categories for lending currently include “state-owned,” “collectively owned,” “individually owned,” and “foreign-owned,” so targeting private firms is tough, said the bankers familiar with the matter. Each bank has its own definition of what a private company is, they added.

One large bank, for instance, uses the denomination for companies that are at least 80 percent owned by private investors, according to one executive with direct knowledge of the matter. The bank considers lending to state-owned enterprises as much safer and is concerned that mandatory credit to private companies could cause bad debts to rise, this person said.

The two other bankers said going strictly by type of investors is problematic, because many companies have shareholders who in turn are owned by state-related entities. It’s also not always clear whether all investors wield proportional influence, the executives said.

A senior executive at a smaller bank said the company is awaiting guidance from regulators on what defines a private company. The lender’s management is debating whether to reduce credit to SOEs to make room for more private-business lending, the executive said.

Policymakers appear to have taken note of the confusion. Banks will be able to conduct their own due diligence rather than comply with lending requirements “unconditionally,” the China Securities Journal reported Monday, citing an unidentified regulatory official.

Concerns about bad loans have dogged China’s banking system ever since the global financial crisis a decade ago, which Chinese authorities effectively countered by flooding the economy with credit. While the official non-performing loan ratio has increased marginally in the past few years, it remains at less than 2 percent -- far below levels seen during the 1990s bad-debt debacle that forced Beijing to bail out its banks.

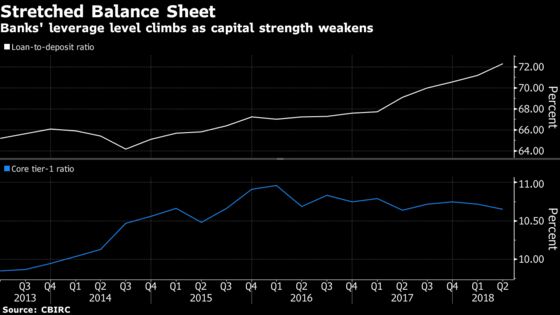

Even so, a system-wide weakening in capital strength coupled with an increase in loan-to-deposit ratios means banks remain sensitive to any acceleration in soured credit.

The government’s long-running campaign to bolster credit for small and micro firms may foreshadow the difficulties facing its private-lending push.

Average borrowing costs for small and micro firms fell 70 basis points in the third quarter from the first quarter, while growth in outstanding loans to such companies was slower than the increase in overall lending in September from a year earlier, according to data from the CBIRC. And some banks have gotten around a requirement that they increase their number of small-business customers by splitting one loan into several to the same borrower, analysts have said.

Jiang Liangqing, a Beijing-based fund manager at Ruisen Capital Management, who owns Chinese bank stocks, said executives won’t just rush blindly to comply with the latest edict and put their own stability at risk.

“Banks may not be as complacent as the policies stipulate,” he said. “They will be diligent in risk management and try to find a way around risks.”

--With assistance from April Ma.

To contact Bloomberg News staff for this story: Jun Luo in Shanghai at jluo6@bloomberg.net;Miao Han in Beijing at mhan22@bloomberg.net

To contact the editors responsible for this story: Sam Mamudi at smamudi@bloomberg.net, Jeanette Rodrigues, Philip Lagerkranser

©2018 Bloomberg L.P.

With assistance from Editorial Board