What Made You Think the Rally Wouldn’t Get Sold?: Taking Stock

What Made You Think the Rally Wouldn’t Get Sold?: Taking Stock

(Bloomberg) -- An 18% jump in three days would be great for the highest-beta asset, let alone a gauge of 500 of the largest companies in the U.S.

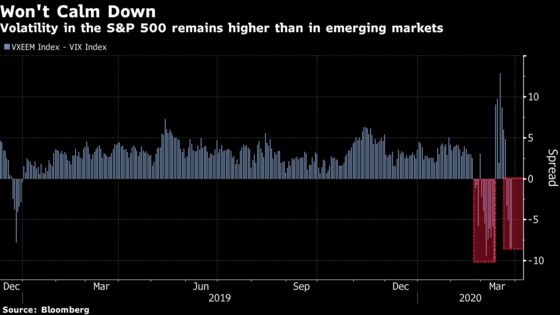

The S&P 500 has gained that much since Tuesday, pushing through a number of resistance lines at light speed and clocking the biggest three-day run since 1933. The VIX Index, which measures projected volatility over the next 30 days, has lost half a point (or 1%) in the same time.

Price swings aren’t likely to subside when investors are going through a range of conflicting emotions a dozen times a day. Millions have lost jobs, the economy is faltering and the U.S. now has more confirmed cases than any other country in the world. But a package of stimulus should provide some relief, and the market caps of companies have jumped by billions of dollars a day this week, recouping some of what they lost in recent, similar plunged.

The same rally would look a lot more sustainable if the VIX was at 35 and not 60, Tallbacken Capital Advisors says.

Certainly, it’s a good to see half of the S&P’s industry groups up 20% or more since Tuesday and the Dow Jones up 21% during that time. But without concrete data on the state of corporate earnings and the economy, yet alone the ETA of a peak in the outbreak, it doesn’t mean all too much. Not a single stock in the Dow Jones is trading above its 50-day moving average, even as the index is on track for the best week since 1931. Caterpillar withdrew its financial outlook for the year and Boeing moved by tens of billions of dollars a day, showing the firm’s true value is a mystery.

In and Out

Analysts will also have to square the stock market advance with data from EPFR Global that showed investors pulled $18.7 billion from U.S. equity funds in the week ending Wednesday, the biggest outflow since at least the beginning of the year.

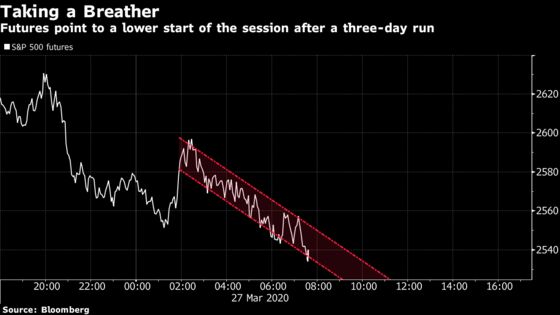

Futures are taking a breather with what has become a modest decline of 2.9% on Friday. Italian stocks fell the most in two weeks as the nation’s business newspaper reported, citing parliamentary documents, that the country may need new economic stimulus in addition to the package already discussed. China posted the biggest fall in industrial profits on record but the Shanghai Composite still eked out a gain.

Today’s final University of Michigan consumer sentiment for March may offer a good view into how bad consumer spending may be in the coming months. Data on Thursday showing last week’s jobless claims quadrupled to a record 3.2 million all but guarantees spending will slow.

So why did stocks rally after an unprecedented spike in jobless claims? Investors could’ve thought the terrible print is as bad as it’s going to get, or that weak economic releases in the weeks ahead are already factored in.

On Tap For Next Week:

And next week will be busy with economic announcements. We’ll get U.S. pending home sales on Monday, a measure of signed contracts (not closings) that’s a good leading indicator of closings that are at least one month out. Shortly after that we’ll get March Dallas Fed Manufacturing Activity. But we’ll have to wait until Friday for the most important one -- the monthly jobs report.

The jobs data is expected to show U.S. payrolls fell in a negative territory in March for the first time in almost a decade. Still, the figure surveys people on the second week of the month, in this case, before the surge in claims triggered by the nationwide shutdown, and won’t likely be a good indicator of the real state of events.

“The April-May data will provide a clearer perspective on the extent of damage inflicted on the labor market,” says Bloomberg Economics’ Eliza Winger.

Consumer confidence print on Tuesday will provide a good lens into how negative consumers’ opinions are on current economic conditions. And we’ll see a final PMI manufacturing print for March on Wednesday, together with ISM manufacturing, construction spending and mortgage applications.

The week will be relatively light in terms of earnings, but Constellation Brands (before the bell on Friday) and Walgreens Boots Alliance (Thursday) will be the ones to keep an eye out for.

Sectors in Focus:

- KB Home is up 8% after a blowout quarterly report after the bell Thursday. Watch peers for a reaction.

- Watch General Motors after the firm announced in a memo (described to Bloomberg News after the bell) that the firm’s salaried staff will have 20% of pay deferred starting April 1 through the fourth quarter of this year or first quarter of 2021, in a move to preserve cash.

- Lululemon reported an acceleration of sales growth in the latest quarter, but refrained from offering an outlook for the current year, in a move that caused a target price upgrade at Piper Sandler and a cut at Guggenheim.

Notes From the Sell Side

Caterpillar was cut to neutral from buy at BofA, which cited the heavy machinery company’s exposure to the energy sector, as well as uncertainty stemming from the coronavirus.

The company recently pulled its forecast due to the pandemic, as have Cummins and Deere, “which only underscores the degree of demand and supply side uncertainty emanating from the COVID-19 outbreak.” Caterpillar “has a strong balance sheet and nearly 4% dividend yield, but so do a lot of other companies,” the firm wrote, adding that a strong yield “is not enough” in the current environment.

Goldman sees a risk from Caterpillar’s energy exposure, noting that it has seen “one major capital spending cut after another from the large E&Ps, as well as pipeline project deferrals in the midstream space.”

Separately, JPMorgan raised its view on Deere & Co., citing valuation after a recent pullback, though the firm continues to see risks for the machinery company.

Analyst Ann Duignan remains “cautious on the structural challenges facing U.S. agriculture,” along with the impact of a strong dollar and ethanol fundamentals. However, Deere’s “balance sheets were in a strong position coming into this crisis and our revised [free cash flow] assumptions suggest they will still be in decent shape coming out of it.”

PepsiCo was upgraded by two notches at Credit Suisse, to outperform from underperform, at Credit Suisse, which cited the food company’s valuation and “near, medium, and long-term drivers.” In the near-term, the pandemic “highlights defensive nature of PepsiCo,” including its “strong positions in water, sports drinks, juice brands and beneficiary from snack pantry loading.” Over the longer term, analyst Kaumil Gajrawala sees PEP’s beverage business improving.

Tick-By-Tick to Today’s Actionable Events:

- 8:00 Robert Kaplan, Federal Reserve Bank of Dallas President, on Bloomberg Radio

- 8:30am -- Feb. Personal Income, Personal Spending

- 10am -- March Final U. of Mich. Sentiment

- FTSV/GILD - HSR expires

- AVX/6971 JP- Tender offer expires

©2020 Bloomberg L.P.