Don’t Let Bristol-Myers’s Megamerger Fool You

Dealmaking in 2019 may be in like a lion, out like a lamb, as acquirers try to digest five years of megadeal madness.

(Bloomberg Opinion) -- Just when the megamerger megacycle looked like it was coming to an end, bam! A $74 billion deal gets announced three days into the new year. (It’s precisely why you should never say never when it comes to dealmaking — I’m looking at you, biotech analysts.)

On Thursday, Bristol-Myers Squibb Co. made a surprise announcement that it’s buying biotech giant Celgene Corp. for $74 billion plus debt. It marks the largest acquisition to ever arrive so soon in a new year.

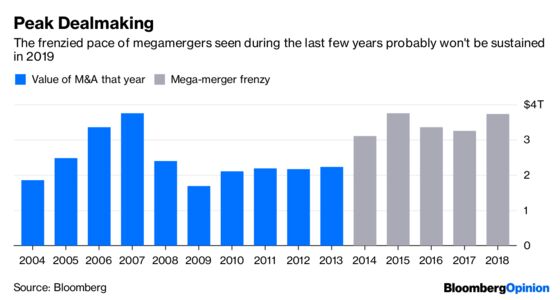

But truth be told, this type of bold takeover activity will probably start to calm down in 2019 throughout the industries that were M&A trailblazers in recent years — media, telecommunications, beer, industrial chemicals and pharmaceuticals. Those areas have nearly reached their consolidation limit following a deal boom that began in early 2014, when a wide range of companies all began to pursue giant acquisitions. The earliest movers included Charter Communications Inc., Japan’s Suntory Holdings Ltd., Facebook Inc., AT&T Inc. and Pfizer Inc.

Megadeals — at one time a rarity — have been popping up ever since, as acquirers struggled to augment sales of their own products and services, and while debt funding was cheap. Most recently, toward the end of 2018, software maker International Business Machines Corp. offered $34 billion for Red Hat Inc., and cigarette producer Altria Inc. made a $12.8 billion investment in Juul Labs Inc.

Bristol’s acquisition of Celgene looks smart and could turn out to be a bargain price. (It may even light a fire under AbbVie Inc. or other rivals to go after deals of their own.) But most buyers in transactions this large haven’t been so lucky. Shares of a majority of the leading acquirers of the last few years have fallen since their deals were struck:

That’s not unusual either. An analysis my team and I did in 2013 also found that acquisitions exceeding $20 billion since 1996 tended to generate losses for shareholders of the acquiring companies. In fact, the buyers lagged behind the MSCI World Index by a median of 13 percentage points in the three years after completing their deals. Other studies over the years have come to similar conclusions, but that’s somehow never stopped acquirers with a big appetite.

So if the megamerger frenzy is winding down, now what? This year will still likely bring a few more large transactions here and there, but the pace should be slower. Notable exceptions include CBS Corp. and Viacom Inc., which will likely finally merge now that Les Moonves is out of the picture. It’s possible that if T-Mobile US Inc.’s deal with Sprint Corp. gets blocked by regulators, other suitors may swoop in for the wireless carriers. Warren Buffett may also spot an opening to do a big acquisition that makes use of Berkshire Hathaway Inc.’s swelling pile of cash. And given Altria’s sudden hunger for deals, one can’t rule out a recombination with Philip Morris International Inc.

Otherwise, it will largely be a year of companies trying to manage their debt, digest their deals, and prove they were worth all that money. Their stock prices reveal that it may be time to give their balance sheets a little TLC.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tara Lachapelle is a Bloomberg Opinion columnist covering deals, Berkshire Hathaway Inc., media and telecommunications. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.