Even College Graduates Can’t Afford a Home on the West Coast

Even College Graduates Can’t Afford a Home on the West Coast

(Bloomberg) -- College graduates earn a lot of money in San Jose but are still $100,000 short to afford a roof over their heads, according to data compiled by Bloomberg.

Soaring home prices, student loan burdens and slow wage growth are delaying many college-educated individuals from achieving the American dream. About a fifth in the decline in homeownership among young adults can be attributed to the increase in student loan debt alone, according to a recent report from Federal Reserve researchers.

Bloomberg used data from the U.S. Census Bureau, Zillow Group Inc. and Bankrate.com to quantify the annual income a college graduate would need to purchase a typical home in the largest U.S. cities.

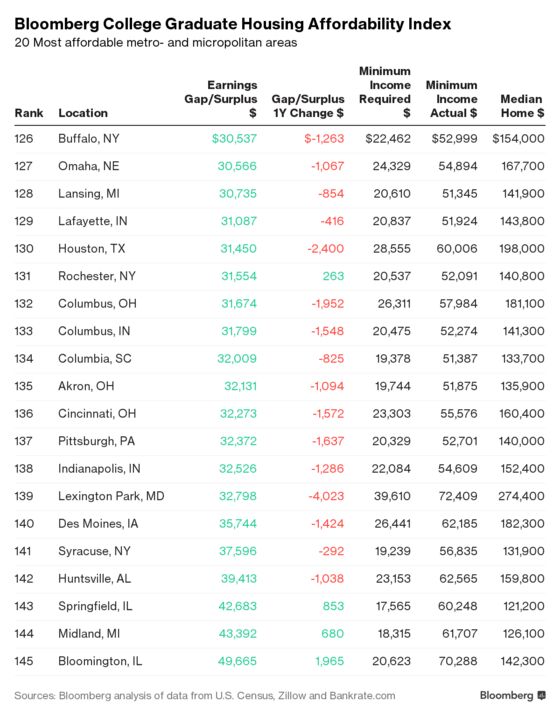

For complete data on all 145 areas, click HERE

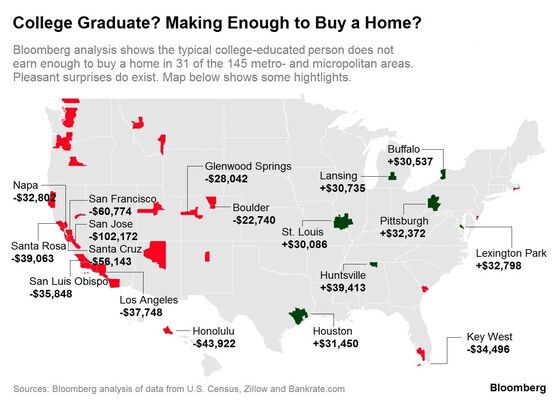

The Unattainable West Coast

The top three most exorbitant neighborhoods on the list -- San Jose, San Francisco and Santa Cruz -- for college graduates, relative to their earning power, along with No.5-ranked Santa Rosa, are located in the San Francisco Bay area. Further, the vast majority of the 31 locations with an affordability gap are located west of the Mississippi river.

In San Jose, a typical college graduate would need to more than double his/her income of $83,430 in 2018 to comfortably cover the mortgage on a typical home, assuming the 20% down payment is not an issue.

Bloomberg inferred the area’s break-even home value, a mortgage level for someone whose pay is around $83,000, to be $560,000. This is 45 percent below the regions median priced $1.25 million home.

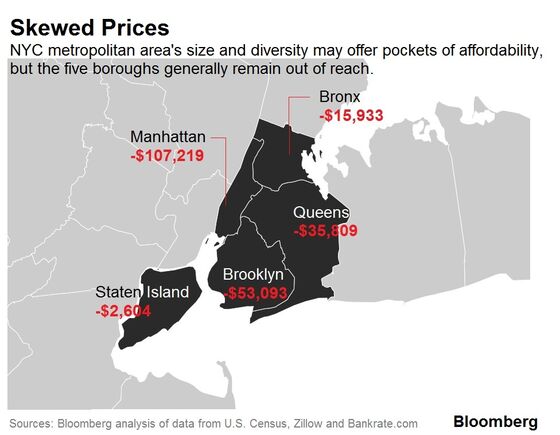

The Big Apple

Not all large cities are as uniformly pricey. The New York metropolitan area is made of 25 diverse counties and connected by extensive commuter systems, this leaves pockets of affordability in the outer boroughs and more remote suburbs.

All five boroughs are below the generally accepted affordability thresholds but variances are wide. The affordability gap for Manhattan, based on an estimated income of just above $80,000 and on a typical home priced at a cool $1.3 million, came out to be a whopping $107,000. But, in Staten Island, a median priced home can be affordable with the income of a typical college graduate.

In any event, if one considers an affordability surplus of less than $10,000 to be a borderline deficit gap -- not an unreasonable margin considering all the additional costs associated with home buying -- many more large cities would slide into the unaffordable territory.

For first-time buyers, it is even tougher. "With home prices climbing ever higher, and inventory yet to see sustained increases, getting a foot in the door is incredibly difficult,” said Justin LaJoie, RealEstate.com General Manager.

There’s Always Houston

Near the other end of the spectrum is Houston, one of the largest and fastest-growing metropolitan areas in the U.S. and where the would-be buyers might find hope.

The region’s monthly mortgage payment is estimated to be an attractive $800 on a median home priced at just shy of $200,000. The transaction would leave the typical college graduates with $31,000 to spare.

St. Louis, Pittsburgh, and Buffalo also rank among the most affordable and are also areas where wages are also rising in excess of 6 percent on an annual basis.

| Methodology: Research included all large U.S. metro- and micropolitan areas with at least 65,000 population with sufficient housing data from Zillow; Final result included areas where either half or more of the renter households have at least college degrees, or where one in three people age 25+ are college educated; U.S. Census data as of 2017; Median earnings by college degree holders excluded those with graduate/professional degrees as highest educational attainment, nor educated population under the age 25 with earnings; 2018 median earnings estimates based on the short-term (three prior years) regional nominal income growth pattern for the demographic group and the general 2017-2018 inflation escalation; Single family home values based on Zillow’s monthly median value for all homes including detached single family homes, condominium and co-operatives; 2018 value estimates based on January to October data; The mortgage payment calculation assumed a standard 20 percent down payment and state-based daily average of 30-year fixed rates, or jumbo rates if the home value was higher than $453,100 for 2018 and/or $424,100 for 2017; Minimum salary required was the inferred amount, assuming one-third of the pre-tax income goes to mortgage payment. |

To contact the reporters on this story: Alex Tanzi in Washington at atanzi@bloomberg.net;Wei Lu in New York at wlu30@bloomberg.net

To contact the editors responsible for this story: Kristy Scheuble at kmckeaney@bloomberg.net, Alex Tanzi

©2019 Bloomberg L.P.