Wells Fargo Reports Revenue Drop, Extended Ban on Asset Growth

Wells Fargo's Revenue Declines as Loan Balances Shrink Again

(Bloomberg) -- For Wells Fargo & Co. investors who were hoping for a turnaround quarter, better luck next time.

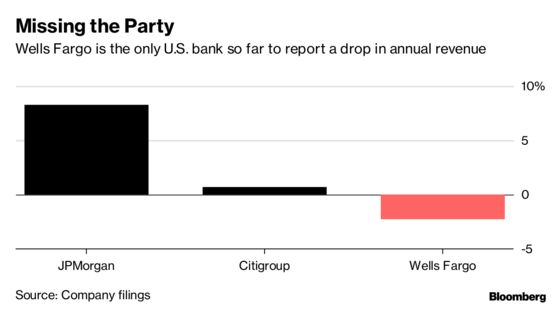

Revenue at the San Francisco-based bank fell 5 percent, the third drop in the past year, dragging the bank to an annual decline as peers boasted growth. Chief Executive Officer Tim Sloan also said the bank now plans to operate under a Federal Reserve asset cap through the end of 2019, rather than just the first half of the year, as previously forecast.

Lower revenue and an extended ban on asset growth beyond end-of-2017 levels show that the bank has yet to bounce back from its problems. Sloan is trying to turn Wells Fargo around following a series of consumer scandals that erupted in 2016 with the revelation that employees may have opened millions of accounts for customers who didn’t want them.

“The extension of the Fed’s asset cap was disappointing, and we think it was a reminder that Wells still has a lot of work left to remediate improper business practices,” Kyle Sanders, an analyst at Edward Jones, said in an emailed statement. Sanders has a buy rating on the stock, and reiterated that “over the long term, we are confident that Wells will emerge from the current regulatory challenges.”

Wells Fargo shares were down 1.4 percent at 12:57 p.m. in New York, the worst performance in the 68-company S&P 500 Financials Index and pushing the bank’s decline for the past year to 24 percent.

Total average loans sank 1 percent in the fourth quarter, driven by a decline in consumer lending, while average deposits fell 3 percent. Meanwhile, Citigroup Inc. and JPMorgan Chase & Co. showed growth in both metrics. The drop in Wells Fargo’s deposits included $1.8 billion associated with the sale of 52 branches in the U.S. Midwest that closed in the fourth quarter.

Provisions for bad loans fell 20 percent, the ninth consecutive quarterly decline and a sign of strength in the economy even amid rising rates and turbulent markets.

Fees from mortgage banking, which drove Wells Fargo to record profits a few years ago, fell by half from a year earlier, reflecting heightened competition and a shift from refinancing to loan origination as rates rise. Mortgage woes are common across the industry: Fees from mortgage banking at JPMorgan also fell by nearly 50 percent in the fourth quarter.

Other Key Results:

|

To contact the reporter on this story: Hannah Levitt in New York at hlevitt@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, Daniel Taub, Steve Dickson

©2019 Bloomberg L.P.