Wells Fargo CEO Charlie Scharf Kicks Off Tenure With More Legal Costs

Wells Fargo CEO Charlie Scharf Kicks Off Tenure With More Legal Costs

(Bloomberg) -- Wells Fargo & Co. may have a new leader, but the work of reinvigorating the firm after years of troubles is far from over.

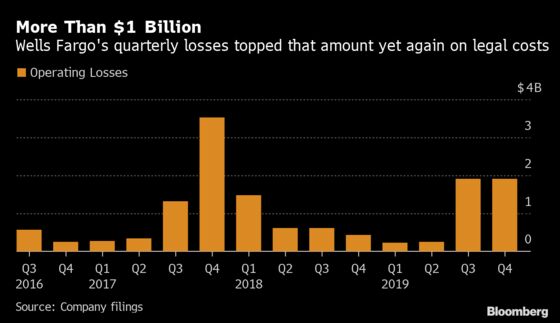

In Charlie Scharf’s first quarter at the helm, Wells Fargo reported $1.5 billion in expenses for litigation as the lender works through its problems, the second straight quarter where earnings were hit by major legal costs. That drove a 53% drop in net income from a year earlier, missing analysts’ estimates.

“Please recognize that it is still early days -- I don’t have all the answers yet, but I will share more as I learn more and as the year progresses,” Scharf, the company’s new chief executive officer, said on a conference call Tuesday. Wells Fargo will “take whatever actions are necessary” to complete the work that lies ahead, he said.

Scharf, who took over in October following a six-month search, has been conducting a wide-ranging review of the firm. He said Tuesday that he has been spending nearly all of his time on regulatory issues, and that there is still much to be done. The bank still faces a bevy of probes and consent orders, including a Federal Reserve-imposed cap on asset growth.

“We have just begun conducting what are really both budget and broader business reviews,” Scharf said, citing technology and efficiency as key themes. “It will take time -- much of this year -- to complete our work.”

The San Francisco-based firm’s longer-term strategy has been in flux since former CEO Tim Sloan stepped down in March. Scharf and Chief Financial Officer John Shrewsberry stopped short of providing time frames and targets, but acknowledged that expenses are too high and revenue and customer growth too low. Revenue fell 5.3% to $19.9 billion, missing analysts’ estimates of a 4.3% decline.

Stock Slumps

Wells Fargo shares fell 3.9% to $50.09 at 11:47 a.m. in New York, their biggest intraday decline since August. Analysts have issued a flurry of downgrades on the stock in recent weeks, pushing their collective outlook to the worst since the financial crisis. The stock has climbed 3.3% in the past year, making it the second-worst performer in the 24-company KBW Bank Index, which is up 23%.

Net interest income, Wells Fargo’s biggest source of revenue, fell 11.4% to $11.2 billion in the quarter. Analysts predicted an 11.1% decline as lower rates continue to hit results. Shrewsberry said Tuesday that net interest income this year is likely to drop by a percentage rate in the low- to mid-single digits from 2019.

Non-interest expenses climbed 17% to $15.6 billion in the fourth quarter. Executives have said costs are likely to remain elevated through 2020 as the lender works through its myriad legal and regulatory issues.

“This is a kitchen sink quarter for the new CEO,” Kyle Sanders, an analyst at Edward Jones, said Tuesday in an interview.

Excluding the legal costs, net income totaled 93 cents a share in the fourth quarter, less than the $1.14-a-share average estimate of 11 analysts in a Bloomberg survey.

“Fundamentals are still pretty weak compared to the other banks,” Sanders said, citing JPMorgan Chase & Co.’s and Citigroup Inc.’s strong results Tuesday. Wells Fargo is “lagging peers in terms of execution.”

JPMorgan and Citigroup both beat estimates, partly on the strength of their consumer units. Wells Fargo’s consumer-banking revenue fell 8% from a year earlier, while JPMorgan’s rose 3%. Revenue also fell 5% in Wells Fargo’s wholesale bank, while gaining 3% in its wealth-management unit.

Also in Wells Fargo’s fourth-quarter results:

- The bank’s efficiency ratio, a measure of profitability, worsened to 78.6% from 69.1% in the third quarter. The firm had been targeting 55% to 59% in the long term, excluding litigation costs, though Scharf may set a different goal.

- Period-end loans and deposits both increased from a year ago, and the number of primary consumer checking customers rose for the ninth consecutive quarter.

To contact the reporter on this story: Hannah Levitt in New York at hlevitt@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, Daniel Taub, Steve Dickson

©2020 Bloomberg L.P.