We’re at Ground Zero a Year After Booms and Busts: Taking Stock

We’re at Ground Zero a Year After Booms and Busts: Taking Stock

(Bloomberg) -- News that China grounded all domestic Boeing 737 Max planes (Indonesia just followed suit) after the second model crash in five months (this time tragically resulting in the deaths of 157 people in the flight from Ethiopia), sent Boeing shares and Dow futures lower early. Despite the developments, S&P futures still have an upward bias following further developments in U.S./China trade discussions.

Other major news having an impact this morning include Mellanox (up 9% on a report, now confirmed, that Nvidia is to buy the Israeli data center, Nvidia down 1.2% pre-market) and Apple (up 1.7%; BofAML analysts upgraded the stock to a buy with a price target of $210, which implies a ~21% advance from Friday’s close).

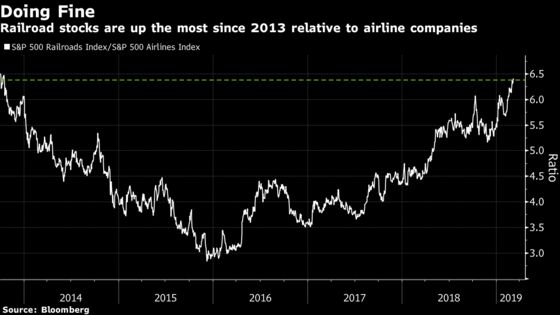

Rail, Rail, Don’t Derail

There were hardly any major sell-side shops that didn’t have a comment about weakening transportation stocks last week, and certainly an 11-day streak of declines in the sector will prompt a reaction. Yet pop the hood and you see a divergence between different members of the Dow Jones Transportation Index, a composite that provides clues about the strength of the economy. As truckers and airlines are tanking, railroads (UNP, NSC, KSU, CSX) are doing just fine - up 18% this year and down just 3.2% since their February record high. Three of the four heaviest-weighted stocks in the TRAN Index are railroad firms; and their advance may be the saving grace. But if they follow airlines and truck companies in their slide, the index’s drop (-4.9% since Feb. 22) may turn into a free-fall.

But then, there is little question that the U.S. economy is moderating (though top White House economic adviser Larry Kudlow said we are “on a roll” in a Friday interview to CNBC), and this week’s retail sales, construction spending and inflation prints will help to figure out just by how much (retail in particular is tricky in light of the shock number last month). But then, all of it could be noise. Considering how much has happened between March 9, 2018 and March 9, 2019 (the Fed hiked four times then turned dovish, a near 20% market selloff rocked portfolios in nearly all asset classes -- and the list goes on) we still find the S&P 500 is exactly where it was a year ago (a 0.15% gain can be treated as noise).

My colleague Felice Maranz on how other parts of the macro picture may shake out:

- Banks and homebuilders may get a boost from Powell’s remarks on CBS’s "60 Minutes" on Sunday. The chairman said he’s in no hurry to change rates, and said the U.S. economy’s outlook is "favorable.” Domestic-focused firms, like regional banks, may also benefit from Powell’s view that the "principal risks" to the U.S. now seem to be coming from slower growth in China and Europe, and from events like Brexit.

- Homebuilders and construction companies may also look a little healthier after Friday morning data showed January new-home construction jumped by 18.6% m/m, the most since 2016. That might mean the worst is over for a group that fell in nine of the past 11 months

- The sailing may not be entirely smooth for regional banks. Wells Fargo CEO Tim Sloan will face a hostile Congress on Tuesday and the bank’s chief technology officer is departing following a days-long system outage last month (after smoke was detected at one of the bank’s facilities). The New York Times over the weekend trashed the bank’s efforts at reform and highlighted worker frustrations, too. Softer deposits at Comerica -- which released slides late Friday ahead of a conference presentation on Tuesday -- might also raise some eyebrows.

- Get ready for a new fiscal fight in Washington, with Trump due to propose a U.S. budget that wouldn’t balance for 15 years, along with deep domestic spending cuts that have little chance of passing Congress. Trump’s budget also sets aside $8.6 billion for the Mexico border barrier. The release is worth watching for signals about policy priorities, and plenty of analysis will follow.

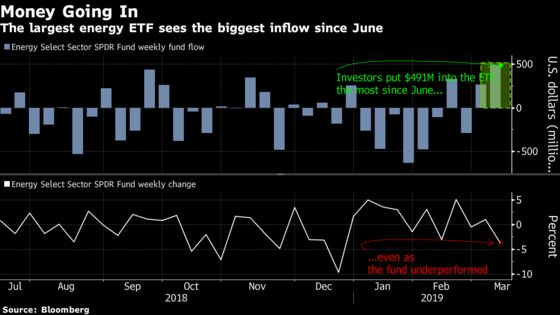

Energy Stocks’ Inflow

Energy is another sector on traders’ radar this week. The group posted its worst week in 2019, counter to an uptick in crude, in part due to a report Norway’s sovereign fund, the world’s largest, is selling $7.5 billion worth of its holdings in oil producers (including APC, CHK, TLW LN, CNE LN to name a few). The second-best performer in the S&P this year through Feb. 20, energy has since dropped to the fifth place, behind industrials, tech, real estate and communication services. Hard to say how long the slump will last, but some investors used this breather as a buying opportunity, putting $491 million into the XLE ETF last week (doesn’t sound like a lot, but it’s the biggest weekly inflow since June). Watch Schlumberger and Baker Hughes after Goldman Sachs initiated the stocks’ coverage with a buy, putting a price target that implies a 33% bounce for the former stock and 40% for the latter.

Notes From the Sell Side

There were a pair of major bullish calls in the technology sector, as BofAML upgraded Apple to buy, citing “10 reasons” to be bullish. The optimistic commentary touched on a number of factors, including valuation, an “overshoot in negative estimate revisions,” a growing base of users and a re-acceleration in the company’s services division. BofAML also had good things to say about the company’s critical iPhone line, which has been the subject of investor anxiety given demand issues, particularly in China. Analysts said they were seeing “stability of supply chain order cuts,” as well as a “large reversal of inventory overhang in iPhones.”

Separately, Facebook added another bull to its ranks of analysts as Nomura Instinet upgraded the stock to buy, citing the transition to the company’s Stories product, which the firm said “appears to be occurring more quickly than we expected, lessening our concern.” Analyst Mark Kelley also boosted his target to $215 from $172 and upped his Ebitda forecasts for both 2019 and 2020. The positive view on the Stories transition came from both industry events and internal data, he wrote. Shares of the social-networking company are up 1.7 percent pre-market.

Analysts are just starting to weigh in on Boeing, and you can see one such synopsis here. Also watch Boeing’s biggest suppliers this morning following the tragic plane crash. Spirit AeroSystems relies on Boeing for 78% of its revenue, according to Bloomberg’s supply chain data, Triumph Group (31%), and to a lesser extent United Technologies (5.4%) and Honeywell International (3%).

Your 63-Hour ICYMI

Here’s some items you might have missed since Friday’s close:

Interest rates can remain on hold as the Federal Reserve waits to see how conditions abroad evolve, chair Jerome Powell said during CBS News’ “60 Minutes,” which was aired on Sunday; a year after the U.S.-China trade spat started, the NYT published the “Will Trump Trade the Future for a Hill of Beans?” editorial that questions whether China’s concessions would be big enough to let Trump achieve the outcome he pursued in starting the trade war; the $134 billion American Balanced Fund-A got the first place in Barron’s ranking of best active managers in 2018; Nvidia was said to be nearing an agreement to buy a $5.9 billion Israeli chipmaker Mellanox (now confirmed); Helen of Troy put its beauty unit up for sale, the WSJ reports; Alexandria Ocasio-Cortez called capitalism an “irredeemable” system that is to blame for income inequality; the U.S. media’s stories on markets and economy are near the most negative since 2011, according to Jefferies’ model, the firm’s analysts said in a Sunday note; UNC Tar Heels posted a season sweep of Duke basketball for the first time in 10 years, earning a share of the ACC regular-season championship.

Tick-by-Tick Guide to Today’s Actionable Events

- 8:30am -- Jan retail sales

- 9am -- VIAB annual meeting

- 9:30am -- RCII/Vintage: final hearing

- 10am -– December business inventories

- 11am – Survey of consumer expectations

- 5pm -- SFIX, COUP, ADT earnings call

- IEA releases its Oil 2019 report

- Cowen Healthcare Conference (March 11-13)

- NIO lockup expires

- Deutsche Bank Media, Internet and Telecom Conference starts in Palm Beach, Florida (March 11-13); companies include AKAM, AMCX, AMT, ATUS, CBS, CCI, CCOI, CHTR, SMLS, CONE, CTL, DLR, EROS, FOXA, GLUU, GTN, I, IAC, IPG, LBTYA, LGF/A, NEWM, NXST, OUT, QTT, SIRI, SSP, T, TIVO, TMUS/S, TNGA, TRIP, UNIT, VIAB, VZ, YNDX, ZAYO, ZG, ZNGA

--With assistance from Felice Maranz and Ryan Vlastelica.

To contact the reporter on this story: Elena Popina in New York at epopina@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Brad Olesen, Steven Fromm

©2019 Bloomberg L.P.