Fed Balance Sheet in Focus: These Are the Market Clues to Watch

Watch for These Market Clues as the Fed Pushes on With Unwinding

(Bloomberg) -- As the Federal Reserve’s balance-sheet unwind enters year two, it’s poised to impact everything from the Treasury’s borrowing needs to bank reserves to how policy makers control the world’s key interest rate.

Vice Chairman Richard Clarida on Tuesday weighed in on the debate over whether the drawdown might soon reach its limits, saying at an event in New York that he sees bank reserves as “obviously abundant,” a view that’s at odds with some in the market. Some believe that reserves are becoming scarce, potentially forcing the Fed to halt the balance-sheet runoff earlier than expected. But the New York Fed markets head Simon Potter, and now Clarida appear to be pouring cold water on that idea.

Clarida reiterated that while the Fed wants to operate with the smallest balance sheet it can to achieve its policy objectives, the central bank is not going to reduce its $4.1 trillion portfolio to the size it was before the financial crisis and its quantitative easing programs. Observers are also hoping the release this Thursday of minutes from the central bank’s November meeting may shed some more light on the Fed’s thinking, though there’s no guarantee of that.

Absent that, investors may be forced to rely on signals from markets. Here’s what funding-market analysts are looking to for signs of potential scarcity:

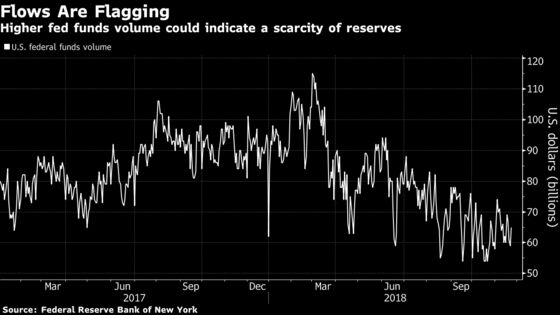

Interbank Lending Volumes

The Fed’s crisis-era bond investments created vast excess bank reserves. With all that money in hand, firms had far less need to borrow from each other in the federal funds market to satisfy regulatory and reserve requirements.

When the unwind begins to pinch, traders are likely to see a rise in volumes within that market from the current levels of about $60 billion per day. Banks increasingly will need to seek out overnight funding to back their deposits or avoid potential overdrafts, according to Alex Roever, head of U.S. rates strategy at JPMorgan Chase & Co.

The New York Fed’s Potter said last month it’s one of several signals he’s keeping an eye on.

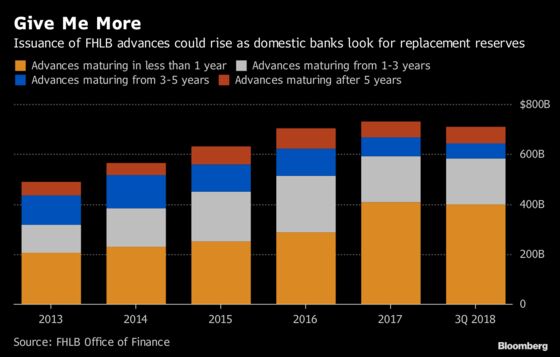

Federal Home Loan Bank Advances

Should reserves become harder to source, U.S. banks can also turn to the Federal Home Loan Banks, a system that provides funding to both large and small institutions to support community investment and housing financing.

Firms with access to FHLB advance loans, or advances, can borrow against their mortgage holdings at rates well below the three-month London interbank offered rate, and use the funds to buy top-tier high-quality liquid assets to meet their capital ratios.

The home loan banks issued about $708 billion of advances this year as of the end of September, with more than half maturing in less than one year, and a weighted-average rate of 2.25 percent, FHLB data show. As reserves become more scarce, the attractive rates and regulatory benefits should spur the FHLBs to issue more short-term advances, Barclays Plc strategist Joseph Abate wrote in a note to clients last month.

Commercial-Paper Supply

While U.S. banks have the benefit of the FHLBs for funding, foreign banks don’t, so they’re likely to lean more heavily on the commercial-paper market for short-term cash. In fact, the space may already be seeing some early effects of the normalization process.

More than a year into the Fed’s balance-sheet drawdown, bank-reserve balances have fallen by about $470 billion, with international institutions accounting for about half of the contraction. During the span, outstanding foreign financial commercial paper reached a record $314 billion. Should overseas banks continue to bear the brunt of the decline in reserves, they will have to continue to seek out alternative sources for short-term funding. TD Securities strategists see pressures in the commercial-paper market building in the third and fourth quarters of 2019 as issuance begins to outstrip demand.

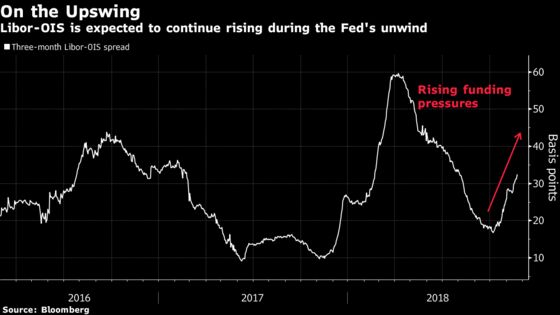

Libor-OIS Spreads

The upward pressure on commercial-paper supply should have a knock-on effect for unsecured funding rates, such as Libor, which is still regarded as a canary in the coal mine for tighter overnight lending markets. This is especially true now given recent changes in Libor’s methodology that tie the fixings closer to banks’ wholesale unsecured funding transactions. It also means the forward derivatives of Libor-OIS could start to rise.

“As reserve scarcity becomes more of an issue at foreign banks, it will be your classic signs of funding becoming more scarce,” said TD Securities rate strategist Gennadiy Goldberg. “So wider commercial paper spreads to OIS, wider FRA-OIS, because the expectation is Libor will track right along.”

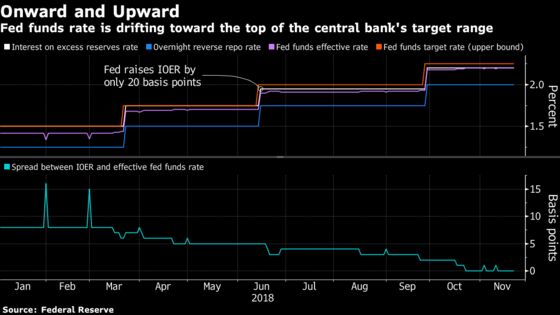

IOER Breaches

Ultimately, one of the clearest signs of stress will be in the rates that prevail in the fed funds market. Policy makers have largely blamed this year’s upward creep in the effective rate toward the top of the central bank’s target range on surging Treasury-bill issuance. It forced officials earlier this year to take the unprecedented step of reducing how much they pay on the excess reserves of deposit banks (the IOER rate) relative to the Fed’s upper bound.

But market participants are starting to suspect bank liquidity is playing a greater role in the drift than policy makers are willing to concede. With fed funds now level with the interest on excess reserves rate for the first time since 2009, some strategists say a major sign of reserve scarcity will be when the policy rate regularly breaches IOER, and begins to test the Fed’s upper bound.

“There will be a reallocation going on as reserves decline,” said Goldberg. “Cash, depending on where it’s going, can have a stabilizing or destabilizing effect.”

--With assistance from Jeanna Smialek, Brendan Murray and Christopher Condon.

To contact the reporter on this story: Alexandra Harris in New York at aharris48@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Boris Korby

©2018 Bloomberg L.P.