Warren Buffett Owes Investors More Than a Memo This Year

Buffett has an opportunity to explain his interest in tech and what Berkshire plans to do with all that cash.

(Bloomberg Opinion) -- Warren Buffett’s annual letters to Berkshire Hathaway Inc. shareholders have felt a bit dry in recent years. Perhaps it was the noticeable reduction in dirty-grandpa humor, or the fact that the world’s most renowned dealmaker hasn’t had a transaction to crow about since 2016.

But for this year’s missive, expected to arrive on Saturday morning, Buffett has provided himself with plenty of fodder — if only he’ll use it to answer two nagging questions for investors:

- Should anything be gleaned about the future of Berkshire from its relatively new, and recently erratic, interest in technology investments?

- If Buffett didn’t find a significant acquisition in December’s market swoon, then when will he?

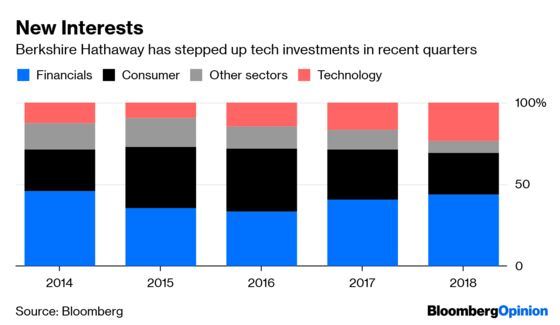

Buffett just hasn’t seemed like himself lately. Not only has the sharp rise in takeover valuations kept him on the M&A sidelines, but in the meantime Berkshire has become a top investor in some of the biggest software companies despite Buffett’s long aversion to tech-related bets. The company’s peculiar stock-picking moves in the fourth quarter, disclosed in a filing last week, added more intrigue: It bought shares of Red Hat Inc., dumped its short-lived Oracle Corp. stake and cut back on Apple Inc.

Berkshire’s jumping in and out of software investments is something a Buffett follower would have never predicted just a couple of years ago. It had a large position in International Business Machines Corp. that it exited in early 2018. Now, it has a stake in Red Hat, which IBM is acquiring. That $34 billion all-cash deal was announced on Oct. 28, so we’re left to assume that either Buffett is quite literally the Oracle of Omaha, or he’s playing merger arbitrageur (Red Hat shares were trading at a significant discount to IBM’s offer). And for an investor who has always preached about taking a long-term view, Berkshire also took a $2.1 billion stake in Oracle in the third quarter, then sold it the next.

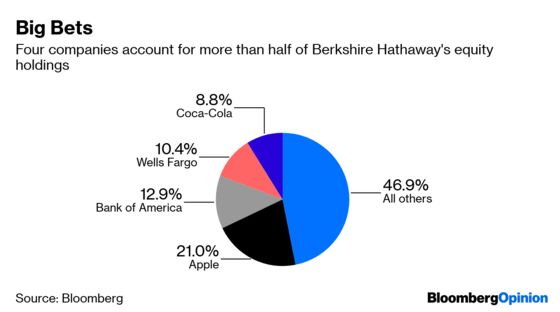

Some of Berkshire’s recent stock-market activity is explained by the increased responsibility Buffett has awarded to Todd Combs and Ted Weschler, his investing deputies. One of them turned him on to Apple initially, another purchase that came as a surprise to Buffett’s followers. Even though Berkshire sold nearly 3 million Apple shares in the latest quarter, it’s still 21 percent of the portfolio.

But with Buffett turning 89 this summer, one has to wonder whether these are early signs of how Berkshire will look when he’s no longer around and if its culture will always have that Buffett feel. His annual letters aren’t known for their element of surprise and have become almost formulaic, usually repeating affirmations about the health of the U.S. economy and conducting autopsies of past business decisions. Buffett should stray from that approach this year and use the letter to provide more transparency about the future of his company — especially when it comes to all its cash.

Berkshire had about $104 billion in cash as of September, which marked one year since it reached 12 figures. For Buffett, the ideal use would be another giant acquisition to add to his empire, and when stocks sold off broadly at the end of 2018, it seemed as if he finally had his opening. I suspected another Valentine’s Day deal. Berkshire’s 2013 buyout of HJ Heinz with 3G Capital was announced on the romantic holiday, which is also the day Berkshire reports its market holdings. Speaking of Heinz, Buffett would also be well served by explaining his plans for Berkshire’s big stake in Kraft Heinz Co., a deal that he helped orchestrate that has turned sour.

The longer Buffett waits to spend his cash pile, the more likely it is that this asset turns into an immense burden for his successor. No matter how skilled the next in line — Greg Abel? Ajit Jain? — is, they will be missing one crucial advantage that Buffett has long enjoyed in M&A negotiations: his name. The idea of selling to and working for him — instead of to another suitor that might have gut the business to save on costs — probably persuaded a lot of targets in the end, perhaps even to accept a lower offer than others would have made amid the U.S. takeover frenzy of the last few years.

Buffett hasn’t done enough yet to ensure a smooth transition. The next generation of leaders is clearly already leaving its mark on the company. His shifting stock investments are proof of that, and Combs even facilitated the Precision Castparts acquisition, Berkshire’s last significant deal.

Last year’s Buffett letter was the shortest one in more than two decades. He can afford to go a little long-winded this time to shed some light on the changes afoot.

That said, Buffett has always been drawn to companies with strong, durable brands like Apple's, and -- cover your ears, Apple shareholders -- the iPhone maker is more of a consumer-products company than a tech one anyway. Red Hat and Oracle are far more unusual for Berkshire.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tara Lachapelle is a Bloomberg Opinion columnist covering deals, Berkshire Hathaway Inc., media and telecommunications. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.