War or Not, Bond Investors Are Taking Their Chances in the Gulf

War or Not, Bond Investors Are Taking Their Chances in the Gulf

(Bloomberg) -- Bond investors can’t resist the allure of Gulf debt even as the region teeters on the brink of conflict between the U.S. and Iran.

Staring down about $13 trillion of negative-yielding global debt, investors are going for the payout on bonds in the Gulf Cooperation Council, a six-nation bloc arrayed across from Iran. Their inclusion in JPMorgan Chase & Co.’s emerging-market indexes also means there’s consistent demand for sovereign debt from the region, which boasts an average credit rating of A+. Saudi Arabia sold its first-ever euro bonds on Tuesday.

Tensions in the Gulf spiked since the U.S. exited a nuclear accord with Iran a year ago and reimposed crippling sanctions. Following the Iranian downing of an American drone, President Donald Trump called off retaliatory airstrikes minutes before the action was set to start.

“Obviously, opportunities come with risks,” said Carl Wong, head of fixed income at Avenue Asset Management Ltd. in Hong Kong whose holdings include securities sold by Saudi Arabia, Qatar and energy giant Aramco. “I don’t think President Trump wants to initiate a war.”

Despite the backdrop, Saudi Arabia’s debt risk measured by five-year credit-default swaps has wiped out almost all increases from May, while the premiums investors pay to hedge against the risk of a default by other Gulf countries have fallen from recent highs.

GCC bonds gained 2.3% in June, the biggest monthly return in more than eight years and just short of the average 2.7% return for emerging-market dollar debt, according to Bloomberg Barclays indexes.

“We are defensive, not bearish GCC,” said Patrick Wacker, a fund manager at UOB Asset Management Ltd. in Singapore. “Our base case at this juncture is no outright military conflict between the U.S. and Iran, including no significant disruption of oil shipments through the Strait of Hormuz.”

UOB Asset remains “modestly overweight” in Gulf bonds even after trimming its wagers following the first set of attacks on oil tankers in the Persian Gulf in May, said Wacker, whose emerging-market debt fund has outperformed the market this year with a gain of almost 11%. It shifted to shorter maturity bonds from longer-dated ones, which would be more vulnerable to geopolitical risk.

Investors who can’t avoid the region should put their money in stronger sovereigns such as Saudi Arabia and Qatar, and reduce their holdings in Bahrain and Oman, which have the weakest finances in the Gulf, according to Arqaam Capital Ltd., a Dubai-based investment bank.

- The yield on Qatar’s bond maturing in 2029 was at almost 3% in London trading hours Wednesday, roughly 20 basis points lower than Indonesia’s debt of similar maturity -- even though the Gulf monarchy is rated five levels higher than the Asian nation

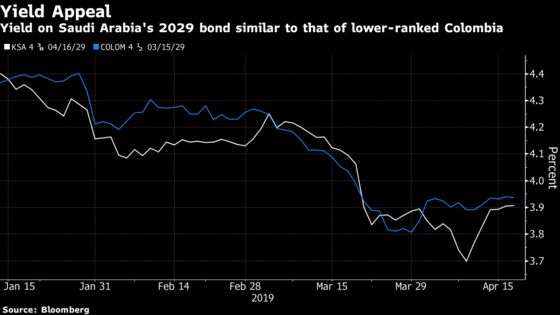

- The yield on Saudi Arabia’s 2029 debt is similar to that of lower-ranked Colombia and Panama

“If your mandate requires you to be invested in the region, we believe you are best served by sacrificing yield for safety,” said Abdul Kadir Hussain, head of fixed-income asset management at Arqaam Capital.

A possibly bigger risk might be the Federal Reserve striking a less dovish tone at its next meeting at the end of the month, said Sergey Dergachev, senior portfolio manager at Union Investment in Frankfurt, who said he remains “constructive” on GCC debt as he expects tensions in the region to eventually calm down.

“If the conflict escalates, it will be one of global scale and will impact all risky asset classes,” Dergachev said.

To contact the reporter on this story: Netty Ismail in Dubai at nismail3@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, Paul Abelsky

©2019 Bloomberg L.P.