Walmart Misses Out on 2021 Stock Rally That Has Boosted Target, Home Depot

Veteran watchers of the mighty retailer are struggling to understand how Walmart missed out.

(Bloomberg) -- Walmart Inc., the engine of the world’s largest family fortune, is missing out on the stock-market rally that has propelled rivals to record highs this year. Veteran watchers of the mighty retailer are struggling to understand why.

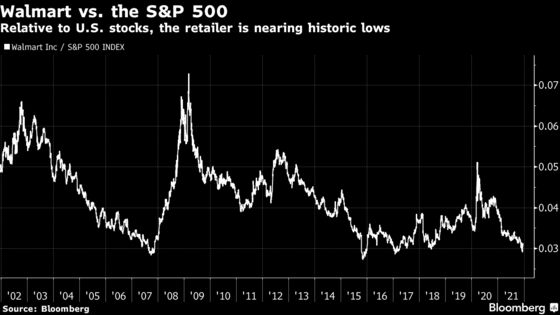

The share price has risen just 1% this year through Wednesday, while the S&P 500 index has advanced 25%. That is Walmart’s worst lag compared with U.S. stocks since 2015, and the gap is wider still with other large retailers. Target Corp. has jumped 34% this year and Costco Wholesale Corp. is up 50%. Home Depot Inc. has surged 54% in a rally that lifted its market value above Walmart’s last month.

“I’m actually taken aback by how weak the equity is, it’s been a terrible stock,” said Scott Mushkin, chief executive officer of researcher R5 Capital. Mark Stoeckle, CEO of Adams Funds, called Walmart’s poor performance “remarkable” and said it was one of the reasons he added shares in August.

The lackluster returns contrast with Walmart’s improving earnings outlook and Wall Street’s call to buy the shares. Based on an average of analyst ratings, the consensus recommendation on Walmart is at the highest in more than a decade. That’s a bet that the company will entice more shoppers with everyday low prices amid rising U.S. inflation, while also making progress on new initiatives from digital advertising to health care.

“There’s this outlook that’s better than it was before,” said Kate McShane, an analyst at Goldman Sachs Group Inc., who added Walmart to the bank’s “conviction buy” list in October. “Now you have an omnichannel retailer that’s well in the game, competing with Amazon and with a more refined international portfolio. That’s a lot of change.”

Walmart declined to comment on its shares.

Improving Outlook

Though investors have largely shunned Walmart this year, the company’s earnings outlook has strengthened. Analysts are predicting adjusted earnings of $6.41 a share for the current fiscal year, which ends in early 2022. That’s 64 cents more than they predicted a year ago. During the same period, estimates for the next fiscal year rose 50 cents a share.

The improving profit estimates combined with the falling stock price mean that Walmart’s earnings multiple has contracted. At the end of last year, investors were willing to buy Walmart shares for more than 25 times blended forward 12-months earnings. That number is now down to less than 22. So by that metric, Walmart is cheaper than it was before.

It’s possible that Walmart’s share performance will perk up, at least relative to U.S. stocks and rival retailers. Mushkin, the R5 Capital CEO, slammed Walmart early this year for shortcomings in customer experience, product freshness and supply chain. But he abandoned his sell rating after the Bentonville, Arkansas-based company did “a great job fixing that.”

Investment Headwinds

While observers are surprised by the extent of the stock’s underperformance this year, there’s been no lack of headwinds for Walmart shares, from the global supply-chain squeeze to the winding down of the U.S. government’s pandemic-era stimulus programs. Also, assets riskier than Walmart enticed investors during much of the year.

In the grocery business, Albertsons Cos. and Kroger Co. have offered more “earnings growth and earnings upside,” said Andrew Gwynn, an analyst at BNP Paribas Exane, who has the lone sell rating on Walmart among recommendations compiled by Bloomberg. Bill Smead, chief investment officer at Smead Capital Management, which oversees about $3.7 billion, is betting that Target will continue to outperform Walmart.

“Going forward, the college-educated mom is the best customer, and Target has an advantage with that person,” said Smead, who holds shares in the Minneapolis-based retailer. “That’s the sweet spot.”

Then there’s the insider selling. The descendants of Walmart’s late founder, Sam Walton, have liquidated shares worth about $6 billion this year. Walmart has said those sales are motivated in part by the family’s desire not to increase its percentage ownership as the company buys back stock. But outside investors typically think twice when insiders are selling.

Food and Gas

Stoeckle, the CEO of Adams, predicts Walmart’s lower- and middle-income customers will hold their own even as government stimulus fades. They’ll also check prices more carefully at the supermarket. That will push them to Walmart, he said. Despite higher labor and supply-chain expenses, Walmart said last month that it was intentionally eating some of the elevated costs instead of passing them along to shoppers.

“Where is inflation going to hit people fastest? It’s food and gas,” Stoeckle said. “Where does Walmart have a big advantage? Food and gas.”

If the Federal Reserve starts raising interest rates and economic growth moderates next year, Walmart will look more attractive, said Walter Todd, chief investment officer at Greenwood Capital in South Carolina. The shares make up a small part of his portfolio and offer “downside protection,” he said.

“Right now, everybody’s looking for the shiny object,” he said. “Walmart is not sexy, and so it’s not what people want today. At some point, they will.”

©2021 Bloomberg L.P.