Walmart Throws a Pipe Wrench Into Tesla’s Works

(Bloomberg Opinion) -- Solar-power developers often talk about a “pipeline” of projects, but this seems a bit too literal:

To ensure proper torqueing, inspectors should have used a special tool known as an MC4 torque tool. However, some inspectors were using a plastic MC4 tool, which is insufficient to ensure proper torque. Indeed, a Tesla inspector admitted that Tesla was using a plumbing tool (rather than an electrical tool) to tighten connectors ... [Emphasis mine.]

That was one of the more choice details from Walmart Inc.’s lawsuit against Tesla Inc. accusing it of “widespread, systemic negligence” with regards to solar-panel installations on more than 240 of the retailer’s stores, including seven connected to fires. And it is the choiceness of the details that matters here.

In its complaint, filed in New York late Tuesday, Walmart contends Tesla breached its contract to design, install, maintain and operate solar-power systems on the roofs of its stores. Aside from the fires — complete with photographic evidence — Walmart accuses Tesla of a pattern of negligence, obfuscation and, as in the instance with the plumbing tool being used to tighten electrical connectors, sheer incompetence. Tesla did not respond to requests for comment. However, in letters from its lawyer, included as exhibits, Tesla blamed Walmart for “breaches of contract, deliberate delay, and bad faith,” effectively blocking the inspection process for the solar installations and unnecessarily forcing the entire fleet shut down for months because of a handful of “thermal events.”

An unusual feature of Walmart’s complaint is that the “substantive allegations” section begins not with the fires or even the installation of the offending panels but an important chapter of Tesla’s own corporate history, namely the 2016 acquisition of SolarCity Corp. Walmart pulls no punches, characterizing the deal as a bailout of a struggling related party. This section reads like a dramatic prologue aimed at establishing the narrative that Tesla’s energy business was built on shoddy foundations, setting off a chain of unfortunate events that ultimately sparked those fires and put that plumbing tool in that inspector’s hand.

It remains to be seen how effective a legal strategy this turns out to be. One of the most interesting aspects of the fight concerns the demand that all of the systems be “de-energized,” something Tesla’s lawyer characterized as being granted for the sake of goodwill but outside the scope of Walmart’s contracted rights. (Investors in leased solar systems are typically paid based on how much energy they generate, so shutting them off is costly.) For its part, Walmart argues that even if only a few fires happened, they were still fires on the roofs of big buildings where masses of customers mill around buying stuff, so perhaps an abundance of caution was warranted (especially if you’ve lost faith in the contractor).

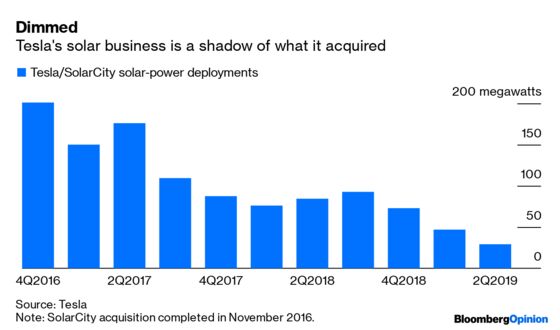

In any case, Walmart’s suit reopens old wounds for Tesla that never truly healed. SolarCity certainly was a struggling company. As I wrote in that summer of 2016, Tesla’s acquisition of it had more red flags than a Chinese embassy, with one proxy advisory firm characterizing it in Walmartian terms as a “thinly veiled bailout plan.” The deal flipped Tesla’s balance sheet from having net cash to net debt, including the $920 million convertible note that had to be settled for cash earlier this year. Since the deal, Tesla’s solar installations have dropped precipitously, with the second quarter’s figure merely one-seventh of what SolarCity deployed in its last quarter as a separate company. Tesla said it expects deployments to “stabilize and grow” in the second half.

Tesla doesn’t break out figures for its energy operations beyond the gross margin line. However, from the fourth quarter of 2016 through the second quarter of 2019, gross profit added up to about $486 million. Annualized, that equates to a return of just 3.6% on the $4.9 billion transaction value — at the gross margin line. Apportioning Tesla’s R&D and general expenses to the energy business in line with its share of revenue would imply cumulative losses at the operating level. Speaking on an investor call earlier this year, a usually supportive Wall Street analyst described the SolarCity deal as a “controlled detonation.”

Walmart’s suit comes mere days after Tesla introduced a new rental option to revive its solar business. Above all, it adds to the sense that SolarCity was a deal that Tesla didn’t need and which has ultimately burdened its resources and now maybe its reputation, too.

The latter is especially important for a company that spent a good portion of last year struggling with the manufacture of a core product, the Model 3 car, and has faced questions about its own safety claims for that vehicle as well as complaints about quality and service. It is also important because, despite record vehicle sales, Tesla’s losses mean its highly priced stock continues to trade less on fundamentals and more on narratives of disruptive genius. At the very least, Walmart’s competing narrative could throw a pipe wrench into those particular works.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.