Wall Street’s Trading Desks Endure Worst First Half in a Decade

Wall Street firms in recent quarters have swung between complaining about too much volatility and too little.

(Bloomberg) -- Bank investors could be forgiven for mistaking executives on recent earnings calls for sports commentators. Their new favorite way to describe trading clients: “on the sidelines.”

Goldman Sachs Group Inc. CEO David Solomon led his analysis for the past two quarters with that phrase, which has caught on with top executives at JPMorgan Chase & Co., Citigroup Inc. and Morgan Stanley as well. Benchwarming by hedge funds and other investors is taking the blame for global banks’ worst first-half trading revenue in more than a decade.

Uncertainty about trade-war politics and Federal Reserve rate moves is making clients extra cautious. But those are the types of macroeconomic events that, in the past, have spurred more trading, not less -- raising the question of whether the “sidelines” problem is a permanent or temporary phenomenon. It can’t be explained away by plunging markets: stocks and bonds keep climbing.

“It’s more of a subdued up than sort of the animal spirits you would generally characterize in this type of environment,” Morgan Stanley Chief Financial Officer Jon Pruzan said in an interview Thursday. “We haven’t seen some of the traditional things in a market like this -- we haven’t seen a lot of people repositioning their portfolios, we haven’t seen leverage increase.”

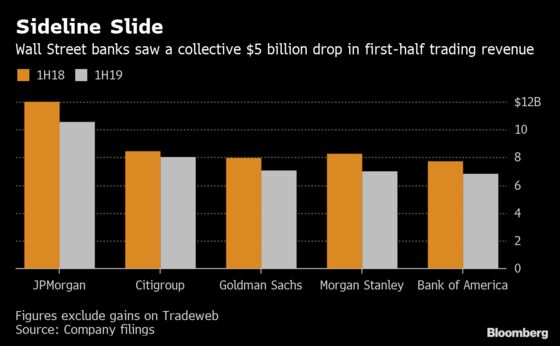

Trading revenue at the five biggest Wall Street banks dropped 8% in the second quarter, following a 14% slide in the first three months of the year. Their European counterparts are expected to post even bigger declines when they start reporting results next week.

That’s likely to push revenue from equity and fixed-income trading at the 12 largest global investment banks below the $60.8 billion they posted in the first half of 2017 -- the post-crisis low -- according to data from Coalition Development Ltd. Those firms generated $77.5 billion as recently as the first half of 2012.

Several factors have weighed on trading desks in recent years. Hedge funds, typically banks’ most active clients, have suffered outflows as they struggled to beat the markets. New rules limited lenders’ ability and willingness to make principal bets with their own money. And technological advancements have narrowed spreads in many areas of trading.

Cost Cuts

Wall Street firms in recent quarters have swung between complaining about too much volatility and too little.

“I’m not sure what the Goldilocks scenario is for the banks,” said Jim Shanahan, an analyst at Edward Jones. “Part of the problem is that it’s too late to hedge interest-rate volatility, there’s not currency volatility to hedge. Speculators need volatility to hedge and enter the market.”

Banks have responded by cutting costs. Front-office headcount in trading units has fallen in each of the past five years, the Coalition data show. And other divisions, including consumer lending and wealth management, have picked up the slack and led banks to record profits. The six biggest U.S. banks set another high-water mark with $32.6 billion in net income in the second quarter.

That doesn’t offer much solace to traders listening to executives like Citigroup Chief Financial Officer Mark Mason describe the sluggishness of their business.

“Many of the investor clients remained on the sidelines,” Mason said Monday.

--With assistance from Jenny Surane, Michelle F. Davis and Sonali Basak.

To contact the reporters on this story: Michael J. Moore in New York at mmoore55@bloomberg.net;Elizabeth Rembert in New York at erembert@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, Steve Dickson, Daniel Taub

©2019 Bloomberg L.P.