Wall Street’s Bullish ‘Illusion’ Shattered by Bad-News Onslaught

Wall Street’s Bullish ‘Illusion’ Shattered by Bad-News Onslaught

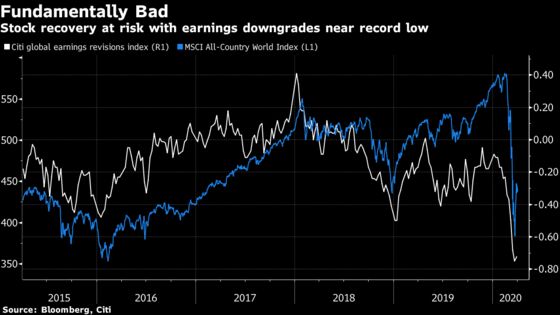

(Bloomberg) -- Companies prepping to cut billions in shareholder payouts. Earnings downgrades hovering near the worst on record. High-frequency labor and manufacturing data flashing the fastest economic shock in decades.

For any money manager betting the market has more or less discounted the unfolding coronavirus crisis and its stimulative offset, the reality checks are coming thick and fast. Small wonder stocks are back in sell-off mode just days after the best week for the S&P 500 since 2009.

As the death toll continues to climb across the U.S. and Europe, corporate boardrooms are facing pressure without precedent. HSBC Holdings Plc and Standard Chartered Plc have announced a halt to dividends and share buybacks, while German car-parts giant Continental AG abandoned its outlook altogether. Factory gauges Wednesday showed global manufacturing activity collapsing.

With some of the world’s largest economies prolonging lockdowns, there’s set to be a deluge of data chronicling a pronounced crash in consumption and investment.

Dip-buyers can take solace in extreme underweights, historic discounts and the sheer tenacity of bullish forces in the pre-virus stage of the business cycle. But investors may yet find valuations are far from cheap enough to cushion a crisis on this scale.

“The American stock markets seem again rocked by a soft-maintained illusion by the Fed,” wrote Jacques Lemoisson, head of global macro at CbH Asset Management, in a note referring to the recent rally spurred by monetary stimulus. “The problem with illusions is that it doesn’t always last very long.”

Other asset classes are signaling a deep downturn. Over the past week, WTI crude has plunged about 16% while 10-year Treasury yields have dropped some 20 basis points. Everyone’s favorite haven currency, the greenback, has rebounded again.

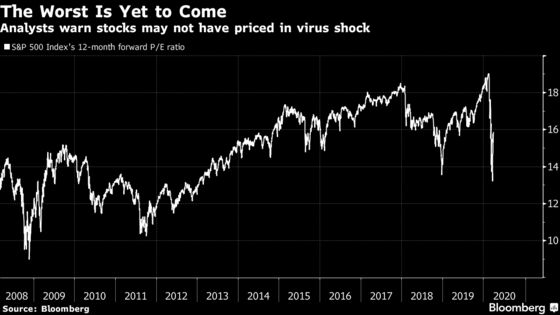

Even using current earnings estimates that are likely to be slashed further, the S&P 500 is trading at 16 times the coming year’s profits, far above the troughs in 2008 and 2011 and still higher than the decade average.

Of course, bond yields are also lower, making shares relatively more attractive. But with earnings projected to drop 36% this year, the equity risk premium -- or the compensation investors receive for holding stocks over Treasuries -- is high but far from historic levels, according to Sanford C. Bernstein strategists.

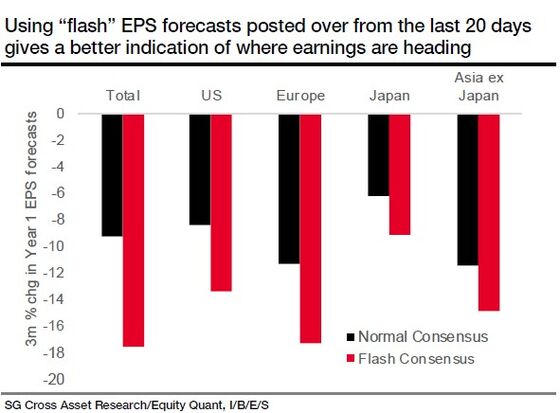

Societe Generale SA’s analysts sounded a similar alarm. By replacing “stale” earnings forecasts with the latest ones, this year’s global price-to-earnings ratio shoots up to 16 times from 14.6 times, a team led by Andrew Lapthorne wrote in a note.

“That’s a fully valued market in normal times, let alone a crisis!” they said.

The other threat to the optimistic case is a slower-than-expected path to recovery. The coronavirus may be a drag on Europe’s growth for the next few years, economists at Nomura Holdings Inc. have warned. Even in China, which is recovering from the virus hit, consumption is taking time to normalize amid financial pressures and persistent caution.

“The COVID-19 crisis will persist longer than many investors suspect and that the economic damage will be deeper and potentially longer-lasting,” Ronald Temple, head of U.S. equity at Lazard Asset Management, wrote in an email. “The best approach is to concentrate capital in companies with the strongest balance sheets and funding profiles and the ability to sustain returns on capital better than their peers.”

As the corporate drag becomes evident, there’s a chance investors will take even more money out of risk assets, according to Alastair Pinder at HSBC Securities. Institutional active funds and passive products may see more redemptions. The new U.S. rule allowing individuals to withdraw up to $100,000 from their retirement plans without a penalty could fuel another $50 billion of outflows, he suggests.

Meanwhile, a drop in stock buybacks may also result in $300 billion of lost stock inflows over the next two quarters, according to HSBC.

The upshot? Just because it’s been terrible doesn’t mean it can’t get worse.

“It is too early to the call the bottom,” Pinder wrote. “From a positioning perspective we still believe there hasn’t been a full capitulation.”

©2020 Bloomberg L.P.