Wall Street Is Getting Cut Out of Bond Market It Long Dominated

Wall Street Is Getting Cut Out of Bond Market It Long Dominated

(Bloomberg) -- The banks that have stood in the middle of the corporate bond market for decades are increasingly getting pushed aside.

Electronic marketplaces like MarketAxess Holdings Inc., Tradeweb Markets LLC and Liquidnet Holdings Inc. say that more of the company bond trades that happen on their platforms are between investors directly, without banks necessarily being involved. Known as all-to-all trading, this shift may weigh on revenues for banks that have long profited from being either buyers or sellers in just about every trade in the $9.2 trillion market.

For more than a decade, corporate-bond traders resisted efforts to carry out more transactions electronically even as most other corners of financial markets embraced the move to computerized buying and selling. But that’s slowly been changing as new rules have forced dealers to act more like machines, linking up buyers and sellers in almost real time as an exchange would, instead of buying securities from investors and hanging onto them.

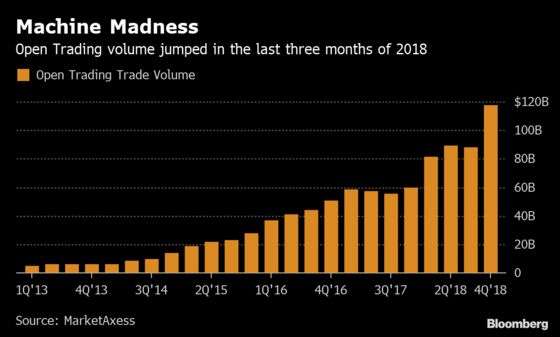

For MarketAxess, 27 percent of corporate bond trades were on its all-to-all platform Open Trading in the fourth quarter, up from 3 percent at the start of 2014, the company said. On Liquidnet’s all-to-all platform, more than 90 percent of volume is between investors. Electronic trading is still a relatively small part of a market dominated by dealers, but its share of trading is growing.

The switch to all-to-all trading may accelerate from here. The post-crisis regulations that have made it more expensive for dealers to hold onto corporate bonds have resulted in dealer inventories of the securities shrinking more than 55 percent over the last five years.

Surging levels of company debt have made many investors fearful that a corporate credit apocalypse is coming, and whenever the market starts to weaken, more money managers may look to offload securities however they can. It also saves investors money by eliminating the middle man: MarketAxess says clients cut $53.7 million in transaction costs in the fourth quarter by using Open Trading.

“It is the model of tomorrow for fixed-income trading,” said Rich Repetto, an equity analyst at Sandler O’Neill & Partners LP. All-to-all is gaining favor with investors because it gives them a new option of anonymously seeking any counterparty to their trade, not just a handful of dealers who know who you are and set their prices accordingly, he said. “All-to-all represents significant advancement in automation in the market.”

Read More: Growing Love for BBBs; Cutting out Wall Street

Investors polled by Greenwich Associates agreed, overwhelmingly saying all-to-all protocols would be the biggest factor helping trading over the next two years. Just as money managers have spent decades cutting their trading costs in equities, they’re looking to lower expenses in bond trading.

“We’ve opened the architecture so anyone can trade with anyone else,” Richard McVey, chief executive officer of MarketAxess, said in an interview. “The cost savings when they find a natural match are meaningful.”

Banks don’t have to panic yet. Electronic bond trading made up 26 percent of the market in the third quarter, according to Greenwich, but those trades are pretty much confined to transactions under about $4 million, which often aren’t profitable enough to be worth a bank’s time. Bigger trades, like those above $50 million, are still done with a bank over the phone or through instant-messaging.

One hurdle for many investors with moving to electronic trading is being sure they’re getting the best possible price and that it makes sense to trade now. A single company can have hundreds of individual bonds outstanding, many of which may not have traded for weeks or months. Money managers often need some hand holding and reassurance that they’re making the right call on big trades, Kevin McPartland, head of market-structure research at Greenwich Associates, said in an interview.

“People want to talk to people, and know they are doing the right thing” on transactions that are $50 million or $100 million, McPartland said.

That concern has been an issue for the scores of firms that have been trying for years to make more corporate debt trading electronic. Getting the right mix of participants has also been an obstacle. Goldman Sachs Group Inc. started and folded GSessions earlier this decade, while BlackRock Inc. found tepid support for its platform because too many customers were looking to buy, and not enough wanted to sell. In 2013 the asset manager linked up with MarketAxess to get access to Open Trading users.

New startups are trying to tackle some of those concerns. Elefant Markets Inc. is a digital broker-dealer that streams bond prices as often as every 10 seconds, based on three internal and external pricing signals. It allows money managers to get prices on a security continually throughout the day, which is harder when dealing with calling an actual human.

“It allows clients to have price information where there was none,” said Cactus Raazi, president at Elefant Markets, in an interview.

Falling Revenue

Banks are already grappling with dropping revenue in corporate bond trading. The world’s 12 largest dealers collected $2.2 billion from company bond and loan trading last year, down from $2.8 billion in 2017 and $3.9 billion the year before, according to data from Coalition Development Ltd., a financial analytics firm. The figures include junk debt but exclude distressed.

Electronic trading is only getting more important for fund managers doing their daily jobs, said Mike Nappi, a senior corporate bond trader at Eaton Vance Corp., which has $445 billion of assets under management. Eaton Vance was an early adopter of one of MarketAxess’s auto-execution tools for corporate bond trading.

“Years ago I would start making calls to trade. Now I do electronic trades at the same time as voice trades and need them to keep my head above the water,” Nappi said.

The pressure may increase as improvements in pricing data give asset managers more confidence that they aren’t getting ripped off when they want to trade without a bank. (Bloomberg LP, the parent of Bloomberg News, has a bond trading platform of its own.) All-to-all trading also makes electronic execution easier by opening up the possibility of dealing with firms or banks you don’t have a trading history with, said Chris Bruner, head of U.S. credit for Tradeweb. Tradeweb introduced all-to-all trading in March 2017, and saw a similar percent of its trades to MarketAxess done in that fashion in the fourth quarter. All-to-all won’t take over the U.S. corporate bond market overnight, but is an increasingly important part of it, he said.

“The all-to-all networks are really meaningful ways clients obtain liquidity,” he said. "It’s here to stay, it’s a big benefit to the market and it should continue to grow.”

--With assistance from Molly Smith.

To contact the reporter on this story: Matthew Leising in Los Angeles at mleising@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, Dan Wilchins, Sally Bakewell

©2019 Bloomberg L.P.