Walgreens Mulls Historic LBO as Debt Markets Start to Wilt

Walgreens Mulls Historic LBO as Debt Markets Start to Wilt

(Bloomberg) -- The prospect of the biggest leveraged buyout in history comes at a precarious time for debt bankers as investors grow increasingly picky in who they’ll lend to and as warnings intensify that corporate borrowing has gotten out of hand.

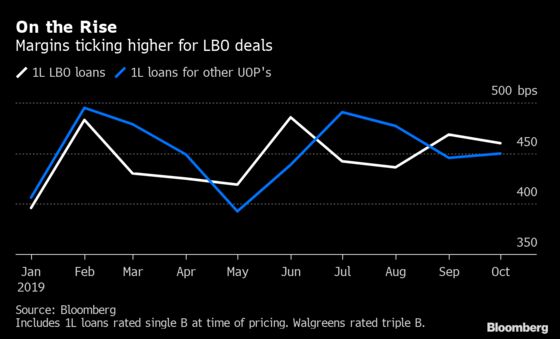

And then there’s the not-so-distant memory of the last time a big pharmacy chain raised a lot of debt to fund an LBO. On the eve of the financial crisis in 2007, banks including Deutsche Bank AG and JPMorgan Chase & Co. were left holding the bag on some $10 billion of risky loans that funded the buyout of what was then Alliance Boots Plc.

Now it’s Walgreens Boots Alliance Inc. -- created almost five years ago from the combination of the Walgreens and Boots chains -- that’s considering going private, people familiar with the matter said. A deal could require it to sell some $55 billion of debt, according to CreditSights Inc. estimates, which if all raised in the junk markets would amount to the biggest such sale ever.

That money would likely have to come from markets where banks in recent months have struggled to find buyers for some of their riskier deals -- particularly LBOs -- as investors weigh the risks of lending at the peak of a record-long credit boom.

As Walgreens shares soared Tuesday on news of the talks with private equity firms, debt investors were already ticking off a list of potential red flags that could make them balk.

“We are skeptical,” said Bill Zox, chief investment officer for fixed income at Diamond Hill Capital Management, which oversees $22.4 billion in assets including junk-rated debt. “Not just due to size but also due to the current price of the equity, already best-in-class margins in the U.S. business and market-share losses to CVS.”

CreditSights bases its $55 billion debt estimate on a 15% premium to Walgreens’ market value and 30% of equity funding. Even that large of an equity check would take Walgreens leverage to as high as 7 times a key measure of the company’s earnings, said James Goldstein, an analyst at the debt-research firm.

The company’s enterprise value, which includes its debt, is about $72 billion and Walgreens had adjusted earnings before interest, tax, depreciation and amortization of $7.65 billion in the year through the end of August.

“The market will be skeptical of any massive leveraging transaction for retail,” Goldstein said in an interview. “If you had to lever up some kind of retailer, a pharmacy retailer is better than department store retail, but I don’t think the market is going to be super receptive to the idea that this will thrive.”

Still, the company may have more levers to pull when it comes to financing a deal, Goldstein said. The owner of Boots in the U.K. could sell of some parts of the business to help fund the transaction, he said. The deal would top the largest leveraged buyout in history: the 2007 sale of utility TXU Corp. to KKR & Co. and TPG, which was worth about $45 billion including debt, according to data compiled by Bloomberg.

Club Deal

A transaction could potentially be put together, said Stephen Schwarzman, Blackstone Group Inc.’s chief executive officer, speaking at an event on Wednesday.

“Is it possible? It might be possible,” he said, adding “It’s a huge stretch, doing things over $50 billion.”

Given the transaction’s magnitude, it may have to take the form of a club deal where a number of private equity groups provide capital, Scott Rostan, founder of Training The Street, which offers technical training to financial firms and business schools, said on Bloomberg TV.

“They’d probably have to club together which brings up other issues around control and joint strategy,” he said. “Club deals also have some bad track records over the past decade. They were scrutinized from an antitrust perspective in recent years.”

The markets for leveraged debt have shown signs of weakness in recent months as the trade war with China stokes fears that a recession is coming.

Unwanted Debt

Banks were left holding more than $2 billion of unwanted debt on their books at the end of October, Bloomberg News reported last month. Among them were some loans for Apollo Global Management Inc.’s buyout of photo-printing company Shutterfly. Jefferies Financial Group Inc. was also forced to fund most of a $650 million loan it had agreed to provide for General Atlantic’s acquisition of a majority stake in eye-shadow retailer Morphe, as demand for riskier credits waned.

Funds that invest in leveraged loans have hemorrhaged cash. An index that tracks loan prices is bouncing around ten-month low. And an increasing rate of credit-ratings downgrades relative to upgrades is constraining some of the biggest buyers of the debt. Even in the more-accommodating market for junk-rated bonds, investors aren’t bending to every deal.

Walgreens also faces pressures that are rippling through both the health-care and retail industries, according to Michael Terwilliger, a portfolio manager at Resource Credit Income Fund. E-commerce giants like Amazon.com Inc. are reshaping how consumers buy medicine, while regulatory and public scrutiny of drug prices has restricted increases.

“Either way, there is good reason to be circumspect,” Terwilliger said.

--With assistance from Lisa Lee, Lara Wieczezynski and Katherine Doherty.

To contact the reporter on this story: Sally Bakewell in New York at sbakewell1@bloomberg.net

To contact the editors responsible for this story: Natalie Harrison at nharrison73@bloomberg.net, Dan Wilchins, Allan Lopez

©2019 Bloomberg L.P.