Volatility Maven Harley Bassman Sees Risks in Bond-Market Tranquillity

Volatility Maven Harley Bassman Sees Risks in Bond-Market Tranquillity

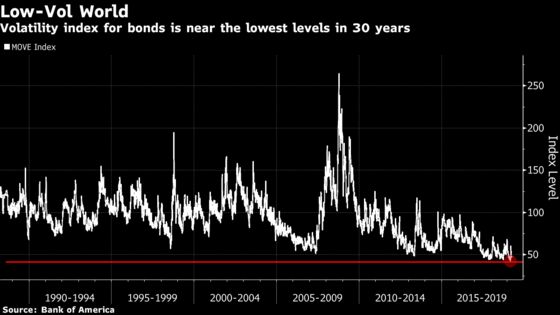

(Bloomberg) -- Harley Bassman invented the MOVE Index, Wall Street’s most widely watched benchmark for U.S. Treasury market volatility, and views its current levels near record lows with trepidation.

The Merrill Option Volatility Estimate Index, which Bassman created while working at Merrill Lynch & Co. in the early 1990s, isn’t a recession indicator. But low volatility tends to run with a dangerous crowd, including a flattening Treasury yield curve and tightening credit spreads.

“Low volatility, by itself, is not a sign of bad things to come,” Bassman said in an interview. “But together with low rates and a flat curve, all three send the same message: Volatility is going to rise as things become problematic with the economy.” A recession isn’t imminent, but mid-2020 “would be a fine time for historical indicators to reprise their prescience,” he added.

From currencies to mortgages and bonds, volatility has plummeted to multiyear lows as major central banks have turned dovish. Morgan Stanley is among banks warning that the days of low volatility are numbered. The MOVE index reached its lowest level of around 42.5 on March 20, and was at 47.6 on Tuesday.

Bassman, 59, worked at Merrill Lynch through its acquisition by Bank of America and capped his career with three years at Pacific Investment Management Co. before retiring in 2017. He calls himself “The Convexity Maven” and writes market commentary from his home in Laguna Beach, California. He’s a font of analogies for the MOVE index.

Loitering

Low implied volatility doesn’t cause market disruptions, but it’s often “found loitering near the scene of the crime,” Bassman says. It’s associated with negative convexity, a sort of accessory after the fact that can accelerate a market move in progress.

But a flattening yield curve followed by tightening credit spreads usually precede it, and are the usual suspects when the economy winds up in the tank.

Gasoline

You can also think of low volatility as fuel, Bassman says. As a sign of ebbing demand for risk-management products and overexposure to risky assets such as triple-B-rated bonds (thus the tightening credit spreads), it’s necessary for the explosion, but “is not the match, it’s the gasoline.”

Egg Salad

On the chicken-or-the-egg question about whether low volatility or a flattening yield curve comes first, the answer is neither. “Ultimately, this is egg salad since the two are fundamentally related.”

--With assistance from John Gittelsohn.

To contact the reporter on this story: Vivien Lou Chen in San Francisco at vchen1@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Elizabeth Stanton, Nick Baker

©2019 Bloomberg L.P.