Fast Money Is Stuck On Sidelines Thanks to VaR Aftershocks

Volatility ‘Earthquakes’ Keep Lashing Wall Street’s Risk Models

(Bloomberg) -- Market tremors from this once-in-a-generation volatility shock are whipsawing risk models across Wall Street, suppressing the appetite of fast-money investors to buy the dip for potentially months to come.

The coronavirus crisis is spurring an epic spree of deleveraging among those wedded to a stable value-at-risk measure, a model pioneered by JPMorgan Chase & Co. which projects the vulnerability of a portfolio by estimating trading losses based on historical data. While the formulas vary, in general the models require investment firms to rein in risk when market turbulence increases.

Risk-sensitive players could now find themselves stuck on the sidelines in any recovery. Unprecedented cross-asset price swings are lashing investing strategies anchored to calm markets and those traders tied to VaR models which guide allocation decisions.

For these kind of reasons, Grace Lo in her newly improvised home office in Maryland is drawing little comfort from last week’s biggest three-day equity rally since 1933.

“High volatility can manifest if markets go up and down, up and down,” said the risk manager at Campbell & Company LP with $1.9 billion in assets. “If you broaden the risk definition to one that’s not just about the system measuring the market move but also about the liquidity, operational risks -- those are the things we don’t quite think are improving yet.”

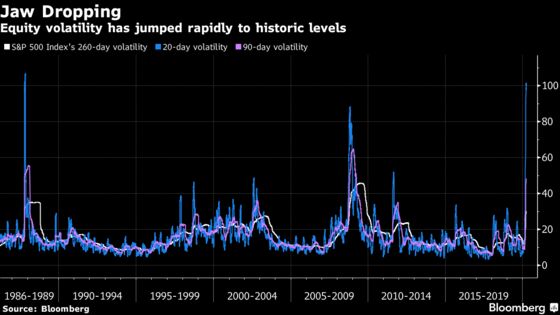

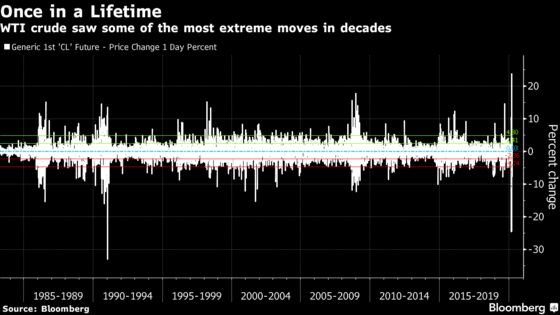

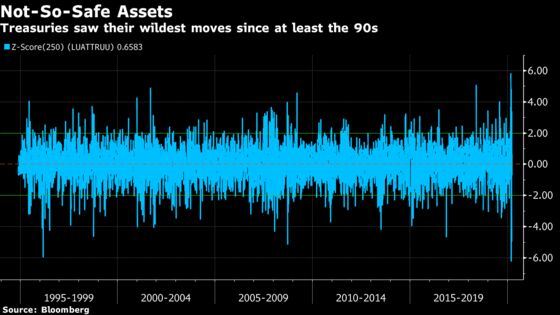

A volatility shock for the history books sparked historic selling across systematic and discretionary funds, despite extraordinary monetary and fiscal measures. Treasuries have staged both the biggest gain and loss for a single day in data going back to the 1990s, in standard-deviation terms. It’s a similar story for the S&P 500 Index. Stocks, bonds, gold and oil have all seen precipitous drops in defiance of conventional hedging logic.

Consider risk-parity managers, who have a ring-side seat to the crisis since volatility guides how much they put into each asset class. This cohort -- estimated to oversee up to $400 billion -- has cut positions by more than 85%, according to Citigroup Inc. That’s spurred a doomloop, in which VaR-induced deleveraging has fueled ever-larger market swings, say Citi analysts.

With implied and realized price gyrations near historic highs, volatility-sensitive quantitative investors have little flexibility to ramp up risk-on exposures anytime soon, even as markets rebound. The S&P 500 was on course for another big gain on Monday, rising 3.2% as of 3:23 p.m. in New York.

While stocks and credit look cheaper these days and options are pricing in smaller swings, models like VaR won’t give the green light for risk-taking for months yet, says Rebecca Cheong, a strategist at UBS Group AG.

“The value-at-risk is going to continue to be very high for some time,” the head of equity derivatives strategy for the Americas said on a recent “Battle of the Quants” webinar. “It’s actually more about the constraint of portfolio management that will force them to not be able to buy that aggressively.”

That’s partly why her stock playbook is akin to 1987: several market bottoms over two months before any recovery.

There are multiple interlinked drivers of deleveraging. Beyond those forced to cut positions as higher volatility pushes up VaR, client redemptions and margin calls also mean many funds have little choice but to downsize portfolios.

Every crisis spurs hang-wringing over the efficacy of risk models. One reason VaR is popular is its apparent transparency. The formula suggests for example that a fund can at most lose $50 million on a given day 95% of the time. The remaining 5% is the tail risk, the ignored possibility that renders these models essentially useless according to the likes of David Einhorn and Nassim Nicholas Taleb.

There is good news. Those less sensitive to VaR such as sovereign funds, insurers and households might help break the vicious cycle between volatility and forced deleveraging, JPMorgan strategists suggested recently. The VaR-tethered cohort which typically includes the likes of hedge funds, banks and market makers have already offloaded much of their risk exposures, according to the U.S. bank.

All told, to the likes of Francesco Filia, VaR models have only made things worse by giving traders an illusion of calm that encouraged excessive risk taking.

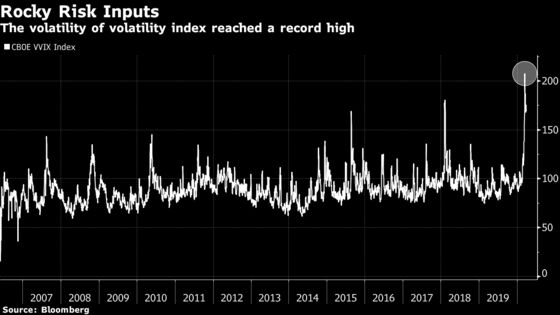

“Stability is destabilizing -- it’s exactly after long periods of low volatility that you get systemic risk,” said the chief executive officer of hedge fund Fasanara Capital. “The VIX exploded all of a sudden like an earthquake.”

©2020 Bloomberg L.P.