Virgin-O2's $38 Billion Deal Isn't All About the People

(Bloomberg Opinion) -- If you listen to the protagonists, Europe’s biggest telecoms deal in a decade is all about the customers. The details of the merger of Virgin Media, the British cable unit of Liberty Global Plc, and O2, Telefonica SA’s U.K. mobile carrier, tell a different story.

According to the companies, the 31.4 billion-pound ($39 billion) deal is aimed at creating a giant company that will give consumers the option of buying all of their broadband, television, mobile and fixed-line services from a single supplier. At the moment, only BT Group Plc provides a similar “converged” telecoms package in the U.K.

It’s true that the new Virgin-O2 will compete more closely with BT, but the structure of the joint venture suggests a different ambition too. Liberty, which is backed by the cable billionaire John Malone, and Spain’s Telefonica are approaching the deal in much the same way as a private equity firm, by saddling the new entity with debt and paying themselves a special dividend. The companies say the venture will be able to carry debt representing five times its Ebitda (a measure of operating performance), so they plan to add another 6.4 billion pounds of borrowings to the Virgin-O2 business. They will then split the proceeds.

Rather than aiming to cut consumer prices, Telefonica appears to be prioritizing its own strained balance sheet — which is understandable enough. Chief Executive Officer Jose Maria Alvarez-Pallete Lopez is urgently working to reduce his company’s mountain of debt, and he’s already had to call off a money-spinning initial public offering of O2 once. After the deal with Malone, Telefonica will get 5.7 billion pounds, including a 2.5 billion-pound payment from Liberty.

In fairness, O2 will no longer sit on Telefonica’s income statement, and the subsequent reduction in the Spanish parent’s earnings will counterbalance the benefits of any cut to its debt when you look at its leverage ratio (the level of a company’s debt relative to its earnings).

Nevertheless, the decision to saddle the new combined entity with a lot of new debt suggests it doesn’t plan to undercut BT aggressively on price. With its borrowings stretched to the upper limit, Virgin-O2 won’t be able to afford to dilute its profitability. Were it planning a serious attack on its rival’s market share, it would probably have left itself more firepower. A proposed 110 million pounds of annual “revenue synergies” — a slightly iffy measure of how many more sales two companies can generate when they join together — would only add 1% of the combined firms’ existing sales.

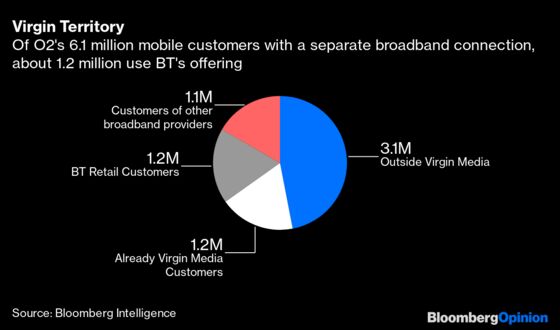

For all of the merger’s potential to cross-sell mobile services to broadband customers and vice-versa, and to save costs through sharing networks, the deal looks more like a clever piece of financial engineering. Indeed, Mark Evans, the O2 CEO, has often played down the appetite for converged telecoms offerings in the U.K.

If Virgin can convince O2 customers to merge their mobile-phone accounts with its longer-term broadband and home phone contracts, that would stop people from switching to other providers too regularly. The more predictable revenue stream would allow the new company to sustain its higher levels of debt.

There’s nothing inherently wrong with any of this. But let’s not dress it up as something that it isn’t.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2020 Bloomberg L.P.