Venezuela's Russian Bank Grows Assets as U.S. Sanctions Hit Home

Venezuela's Russian Bank Grows Assets as U.S. Sanctions Hit Home

(Bloomberg) -- A small state-run bank in Moscow which is half-owned by Venezuela’s government was one of Russia’s fastest growing lenders last year at a time when President Nicolas Maduro tries to work around U.S. sanctions and asset freezes that are crippling his country’s finances.

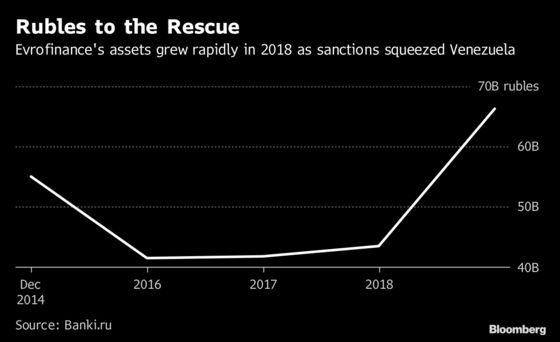

Evrofinance Mosnarbank, owned by Venezuela’s development bank and Russia’s state-controlled Gazprombank and VTB Group, was in the top ten percent of Russia’s 100 biggest lenders last year in terms of growth in assets. Its net assets surged 52 percent to 66 billion rubles ($1 billion), making it Russia’s 82nd largest, according to Banki.ru calculations based on central bank data.

Evrofinance’s explosive growth comes after a series of U.S. sanctions curtailed Venezuela’s ability to operate in the global financial system, making the Moscow-based lender an ideal option to handle payments to its suppliers and as a safeguard for deposits. In meetings held in Caracas last year, private banks were encouraged to open accounts with Evrofinance by government officials in order to perform transactions abroad, according to people who attended the meetings and asked not to be named discussing the topic publicly.

This month Maduro was sworn in for a second six-year term that his foes and at least 60 countries around the world deem to be illegitimate due to questions around the election. The U.S., which has become the strongest voice against Maduro’s regime, has recognized National Assembly leader Juan Guaido as the rightful leader of Venezuela and is handing over Venezuelan government accounts in the U.S. to him. The U.S. also banned imports of Venezuelan crude and exports of refined goods essential to Venezuela’s domestic fuel industry.

Russia, which has backed Venezuela both politically and financially, has thrown its full support behind Maduro.

With just $8.4 billion of international reserves, most of which is in gold, Venezuela is trying to fend off the moves to asphyxiate its finances. A request to repatriate $1.2 billion of gold held at the Bank of England has been denied.

Fast growth is unusual among Russian banks amid anemic economic growth and an ongoing purge of the financial industry that has consolidated power among the biggest players. Evrofinance is not currently subject to sanctions.

Evrofinance’s press department didn’t respond to a request for comment. Venezuela’s Finance Minister Simon Zerpa declined to comment about the bank.

The bank was set up as as a joint venture in 2011 to build on the alliance between Vladimir Putin and the late Hugo Chavez. In 2011, Chavez, riding a wave of sky-high oil prices and confidence, bought a stake of 50 percent minus two shares in Evrofinance through the FONDEN development bank. Originally viewed as a bilateral bank to fund joint oil and infrastructure projects, Evrofinance obtained a local banking license, opened an office in Caracas and even advised on more than $3 billion of bond sales.

VTB Chief Executive Andrey Kostin said this month that he would like to sell VTB’s Evrofinance stake but any deal would be difficult because the lender is regulated by an intergovernmental agreement, Interfax news agency reported.

--With assistance from Fabiola Zerpa.

To contact the reporter on this story: Jake Rudnitsky in Moscow at jrudnitsky@bloomberg.net

To contact the editors responsible for this story: Torrey Clark at tclark8@bloomberg.net, Daniel Cancel

©2019 Bloomberg L.P.