Venezuela Bondholders Are Gearing Up for Battle After Futile Year

Venezuela Bondholders Are Gearing Up for Battle After Futile Year

(Bloomberg) -- For the better part of the past year, Venezuela’s debt market has been dead. The bonds are in default and there are no restructuring talks, almost no trading and little action from creditors beyond grumbling in private.

But that appears about to change. In the past few weeks, one group of investors banded together to demand immediate payment on the notes they hold, another cohort hired a law firm to review their options and a separate creditor sued in U.S. federal court. Their impetus to act seems to stem from both fleeting patience and the realization that if they don’t move now, they may fall behind other creditors in the line to lay claim to Venezuelan assets.

“Bondholders are gearing up for a fight,” said Francisco Rodriguez, the chief economist at Torino Capital in New York. “They had been pretty quiet on the expectation that either some type of restructuring negotiation would emerge or that a change of political regime would occur in Venezuela. It seems like bondholders have decided that they have nothing to gain from continuing to wait.”

Venezuelan debt has been hovering around 25 cents on the dollar since President Nicolas Maduro announced in November 2017 that he was suspending payments and seeking talks with creditors. Those discussions never took place, due to U.S. sanctions that make doing business with the country difficult, and for the most part not much else was happening as the arrears piled up.

Now the urgency to act has increased after Houston-based ConocoPhillips and Canadian gold miner Crystallex International Corp. managed to wring payments worth a total of $1 billion out of Venezuela to partially satisfy claims over appropriated assets. If those entities were able to get paid, bondholders’ thinking goes, then debt investors should be able to get a piece.

The prize that creditors have their eyes on is the country’s largest U.S. asset, the refining company Citgo Holding Inc., which has been valued at $11 billion. Unsecured bondholders are likely to find themselves fighting with a long line of claimants. In addition to having to compete with businesses armed with international arbitration awards, state oil company bonds due in 2020 are explicitly backed by a stake in the refiner, giving those holders a strong claim on the asset.

“They’ve already shown there are ways of getting ahold of assets. That’s the trigger,” said Cecely Hugh, investment counsel in emerging-market debt at Aberdeen Standard Investments in London. “If you accelerate, you go to court and you’re in a better position than a creditor without a judgment. Now that they’ve started, you could see more activity next year.”

It’s all quite a dramatic turn of events for investors, who reaped decades of huge returns investing in Venezuelan debt before the socialist government finally ran out of money to pay them amid an economic collapse, a dollar shortage and the oil industry’s collapse. Hyperinflation has raged on, with a Bloomberg price index indicating it’s running at an annual pace above 200,000 percent.

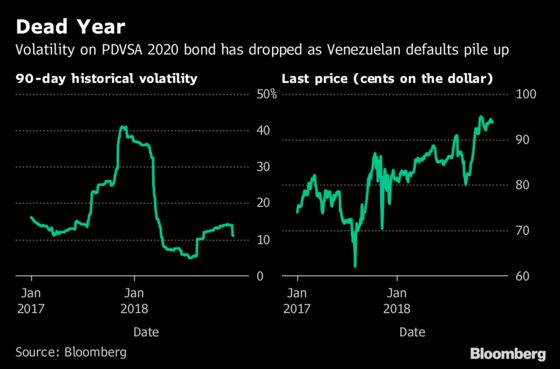

In the meantime, bonds are barely moving. The 90-day historical volatility on Petroleos de Venezuela’s bond due in 2020, the only one it continues to pay in a bid to hold onto Citgo, has declined to 11 percent from a high of 41 percent last November, according to data compiled by Bloomberg. It hit the lowest ever in mid-July.

While Venezuela has kept paying 2020 bondholders, “the government is only buying time,” said Francisco Ghersi, managing director of the Venezuela-dedicated hedge fund Knossos Asset Management. “It’s impossible to keep current with them much longer."

Aggressive legal actions from bondholders could also hinder PDVSA’s operations, Eurasia Group analyst Risa Grais-Targow wrote last week. Earlier this year, Conoco obtained attachment orders through Caribbean courts, where the legal system was relatively amenable to efforts to seize Venezuelan oil cargoes in vessels and storage tanks across the region. The order caused major disruptions in PDVSA’s oil exports and forced Venezuela to work on a deal with Conoco.

Maduro has said that he’s holding talks with bondholders and predicted this month that a deal will be struck next year. “We’re in the middle of a successful renegotiation process,” he told reporters in Caracas. “It’s going very well.”

In reality, there are zero signs of any such discussions. No bondholder contacted by Bloomberg News has been involved in any meeting of any kind in recent months. And analysts say there’s likely to be a lot more drama before anything is resolved.

Here are the bonds that Venezuela and its state companies are behind on:

| Bond | Coupon Value (Millions of USD) | Due Date | Grace Period End |

| VENZ 2019 | $96.70 | Oct. 13, 2017 | Nov. 13, 2017 |

| VENZ 2024 | $103 | Oct. 13, 2017 | Nov. 13, 2017 |

| VENZ 2025 | $61.20 | Oct. 21, 2017 | Nov. 20, 2017 |

| VENZ 2026 | $176.30 | Oct. 21, 2017 | Nov. 20, 2017 |

| VENZ 2023 | $90 | Nov. 7, 2017 | Dec. 7, 2017 |

| VENZ 2028 | $92.50 | Nov. 7, 2017 | Dec. 7, 2017 |

| PDVSA 2026 | $135 | Nov. 15, 2017 | Dec. 15, 2017 |

| PDVSA 2024 | $150 | Nov. 16, 2017 | Dec. 18, 2017 |

| PDVSA 2021 | $107.70 | Nov. 17, 2017 | Dec. 18, 2017 |

| PDVSA 2035 | $146.30 | Nov. 17, 2017 | Dec. 18, 2017 |

| VENZ 2018 7% | $35 | Dec. 1, 2017 | Jan. 2 |

| VENZ 2020 | $45 | Dec. 12, 2017 | Jan. 11 |

| VENZ 2036 | $162.50 | Dec. 29, 2017 | Jan. 29 |

| VENZ 2034 | $70 | Jan. 16 | Feb. 15 |

| VENZ 2031 | $251 | Feb. 5 | March 7 |

| VENZ 2018 13.625% | $72 | Feb. 15 | March 19 |

| PDVSA 2022 12.75% | $191 | Feb. 20 | March 22 |

| VENZ 2022 | $191 | Feb. 23 | March 26 |

| VENZ 2027 | $185 | March 15 | April 16 |

| VENZ 2038 | $44 | March 31 | April 30 |

| ELECAR 2018 (principal) | $678 | April 10 | April 10 |

| PDVSA 2027 | $81 | April 12 | May 14 |

| PDVSA 2037 | $41 | April 12 | May 14 |

| VENZ 2019 | $97 | April 13 | May 14 |

| VENZ 2024 | $103 | April 13 | May 14 |

| VENZ 2025 | $61.20 | April 23 | May 23 |

| VENZ 2026 | $176.30 | April 23 | May 23 |

| PDVSA 2022 6% | $90 | April 30 | May 30 |

| VENZ 2023 | $90 | May 7 | June 6 |

| VENZ 2028 | $92.50 | May 7 | June 6 |

| PDVSA 2026 | $135 | May 15 | June 14 |

| PDVSA 2024 | $150 | May 16 | June 15 |

| PDVSA 2021 | $107.70 | May 17 | June 18 |

| PDVSA 2035 | $146.30 | May 17 | June 18 |

| VENZ 2018 | $35 | June 1 | July 2 |

| VENZ 2020 | $45 | June 11 | July 11 |

| VENZ 2036 | $162.5 | June 29 | July 30 |

| VENZ 2034 | $70 | July 13 | Aug 13 |

| VENZ 2031 | $251 | Aug. 6 | Sep. 5 |

| VENZ 2018 (principal) | $1,053 | Aug. 15 | Aug. 15 |

| VENZ 2018 | $72 | Aug. 15 | Sep. 14 |

| PDVSA 2022 | $191 | Aug. 17 | Sep. 17 |

| VENZ 2022 | $191 | Aug. 23 | Sep. 24 |

| VENZ 2027 | $185 | Sep. 17 | Oct. 17 |

| VENZ 2038 | $44 | Oct. 1 | Oct. 31 |

| PDVSA 2027 | $81 | Oct. 12 | Nov. 13 |

| PDVSA 2037 | $41 | Oct. 12 | Nov. 13 |

| VENZ 2019 | $96.70 | Oct. 15 | Nov. 14 |

| VENZ 2024 | $103 | Oct. 15 | Nov. 15 |

| VENZ 2025 | $61.20 | Oct. 22 | Nov. 21 |

| VENZ 2026 | $176.30 | Oct. 22 | Nov. 21 |

| PDVSA 2022 6% | $90 | Oct. 29 | Nov. 28 |

| VENZ 2023 | $90 | Nov. 7 | Dec. 7 |

| VENZ 2028 | $92.50 | Nov. 7 | Dec. 7 |

| PDVSA 2026 | $135 | Nov. 15 | Dec. 17 |

| PDVSA 2024 | $150 | Nov. 16 | Dec. 17 |

| PDVSA 2021 | $107.70 | Nov. 19 | Dec. 19 |

| PDVSA 2035 | $146.30 | Nov. 19 | Dec. 19 |

| *VENZ 2018 (principal) | $1,000 | Dec. 3 | Dec. 3 |

| *VENZ 2018 | $35 | Dec. 3 | Jan. 2 |

| *VENZ 2020 | $45 | Dec. 10 | Jan. 9 |

--With assistance from Lucia Kassai.

To contact the reporters on this story: Patricia Laya in Caracas at playa2@bloomberg.net;Ben Bartenstein in New York at bbartenstei3@bloomberg.net

To contact the editors responsible for this story: Daniel Cancel at dcancel@bloomberg.net, ;Jeremy Herron at jherron8@bloomberg.net, Brendan Walsh, Randall Jensen

©2018 Bloomberg L.P.