Fine Print in Leveraged Loans Sparks Market Backlash

Fine Print in Leveraged Loans Sparks Market Backlash

(Bloomberg) -- Some of the largest investors in the $1.2 trillion market for risky corporate loans say they’re being given too little time to comb through the hundreds of pages of documents that govern the deals, leaving them exposed to potentially dangerous loopholes.

Now many are urging the industry’s main trade group to do something about it.

GSO Capital Partners, the credit arm of Blackstone Group Inc., is working with roughly a dozen other buy-side firms as well as underwriters including JPMorgan Chase & Co. and Bank of America Corp. to propose new industry standards, according to people with knowledge of the matter.

Money managers often have only a day or two to sift through reams of loan documentation before deciding how much to buy -- a timetable intentionally set up by borrowers seeking the best possible terms. The pushback follows a number of high profile transactions in which private equity sponsors took advantage of weak investor protections to shift assets and cash flow out of reach of creditors, catching them off guard and fueling bitter clashes.

“A 24-hour shot clock is obviously too short of a window to effectively go through these documents,” said Bill Housey, a senior portfolio manager at First Trust Advisors who is not involved in the discussions. “If assets or collateral can be stripped from lenders through various loopholes, we want to make sure we are paying very close attention upfront.”

Representatives for GSO, Bank of America and JPMorgan declined to comment.

The GSO-led group, which was created in June as a subcommittee of the Loan Syndications and Trading Association, is discussing a proposal to update guidance the industry group first issued nearly 15 years ago, according to the people, who asked not to be identified because the talks are private.

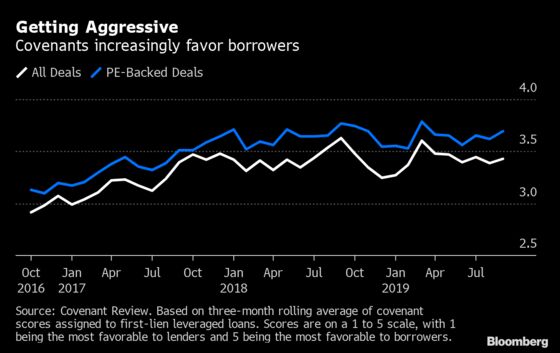

The market for leveraged loans has roughly doubled in size over the past decade as investors looking for higher returns piled into riskier debt. Borrowers have been able to chip away at traditional investor protections amid the surging demand for deals. That has left some of the largest private equity firms in a tug of war with their own credit arms over deal terms.

Loans for buyouts are typically marketed to investors over a two-week period that begins with a presentation from the arranging banks and ends with a commitment deadline, by which time investors need to submit their orders for a chunk of the debt.

One of the proposals under consideration calls for a draft of the credit agreement to be shared with investors when a new syndication launches, similar to what happens with bond offering prospectuses, the people said.

Interested buyers now usually receive only a marketing term sheet when deals launch, which contain an outline of the loan’s key terms but often lack details around specific provisions, where loopholes can be hidden.

Some of the group members regard the proposal as too ambitious, and have expressed skepticism that any new guidelines could be effective without including private equity firms in the discussions, the people said.

Credit Suisse Group AG, Eaton Vance Corp., Octagon Credit Investors, HPS Investment Partners and the credit arm of buyout giant Apollo Global Management Inc. are also part of the GSO-led group, the people said.

“As part of our ongoing efforts to assess and enhance market standards, we’re continuously working to achieve consensus among all market participants and update guidance in this particular area,” Lee Shaiman, the LSTA’s executive director, said in an emailed statement.

Representatives for Credit Suisse, HPS and Apollo declined to comment, while Eaton Vance and Octagon weren’t available to comment.

Four Days

The LSTA’s current guidelines recommend issuers give borrowers at least four business days to review a draft of the credit agreement “unless circumstances require a shorter review period.” They also call for issuers to provide prospective lenders with “a reasonable amount of time” to examine and comment on material changes to the draft.

Yet investors say that on deals private equity firms expect will have broad appeal, the draft is sometimes shared less than 24 hours before commitments are due, and a final version of the agreement may not be available until after the cutoff.

While investors can put in orders that are subject to documentation, weeks of fundamental analysis may go to waste should they object to the final credit-agreement language.

J. Crew, PetSmart

In recent years investors watched struggling companies owned by private equity firms execute asset transfers, spinoffs, carve outs and other controversial moves as a result of allowances inserted into the fine print of loan documents.

Retailer J. Crew Group Inc. established one of the best known precedents nearly three years ago when it transferred its intellectual property, including its brand, outside of creditors’ reach as part of a debt restructuring, prompting a legal fight with lenders.

More recently, PetSmart Inc. was taken to court by creditors after it transferred part of its stake in online unit Chewy.com away from lenders as it struggled to turn around its brick-and-mortar business. Some of the debt holders dropped their litigation after reaching a deal with the company.

While most details buried in loan documents rarely come into play for companies with healthy balance sheets, a turn in the credit cycle could leave businesses struggling to repay lenders and their private equity owners scrambling to protect their investments from creditors.

“These are living and breathing documents that will be tested in the next downturn,” Housey said. “Understanding those provisions is going to be very important.”

--With assistance from Sally Bakewell, Kelsey Butler and Paula Seligson.

To contact the reporter on this story: Davide Scigliuzzo in New York at dscigliuzzo2@bloomberg.net

To contact the editors responsible for this story: Natalie Harrison at nharrison73@bloomberg.net, Boris Korby

©2019 Bloomberg L.P.