UBS Says Investors Should Prefer Green Bonds Over Regular Debt

UBS Says Investors Should Prefer Green Bonds Over Regular Debt

(Bloomberg) -- Sustainable bonds are a “defensive opportunity” that credit investors should favor over non-green, investment-grade corporate notes, said UBS Global Wealth’s head of credit, Thomas Wacker.

Most industries that have been overwhelmed by the impact of the coronavirus and a slump in crude oil prices -- including oil and gas, basic materials, consumer discretionary and autos -- are “pretty much nonexistent” in the green bond market, Wacker said in a telephone interview Friday. Instead, sustainable debt issuance has been highly concentrated among more conservative sectors like utilities, banks and to a lesser degree, cyclical industrial names.

“This is the defensive nature essentially of that market, and that has led to significantly smaller drawdowns now on the correction,” Wacker said.

A company’s sustainable bonds tend to have tighter bid-ask spreads compared to its non-green notes, and that’s still evident despite the current market turmoil, said Wacker. While risk premiums have blown out for both types of securities, the widening hasn’t been as pronounced for green debt.

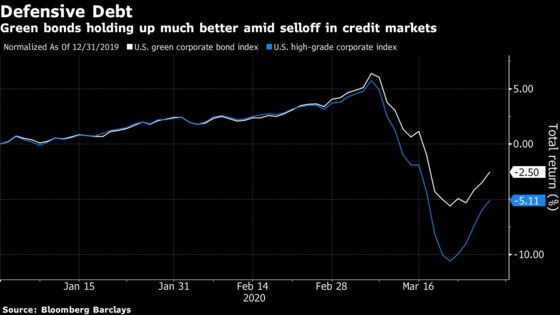

The Bloomberg Barclays U.S. Green Bond Index is down 2.5% so far this year -- far less than the 5.1% drop seen in the investment-grade, corporate debt benchmark. Before credit markets were hit by the coronavirus-oil price hammer blow, broad credit was returning more than environmentally-friendly debt, according to data compiled by Bloomberg.

Moreover, investors that own green bonds tend to hold on to sustainable debt when selling down a portfolio because of their scarcity. This can be of benefit because buyers like big pension and wealth funds allocate a certain amount of their investments to sustainable finance. These funds are still active in the market, Wacker said.

“They are not trading-oriented,” said Wacker. “They are not the ones to drop the bonds in this environment.”

Green Refinancing

Wacker doesn’t expect green bond issuance to be significantly hurt by volatility because borrowing is linked to specific projects. Companies like utilities also tend to have a very long planning horizon for these initiatives. Consolidated Edison Inc., for example, sold $1.6 billion of sustainable debt last week to fund new and existing expenditures.

“If you build a wind park, that’s not something that’s hugely affected by the disruption that we currently see,” Wacker said. “These projects are happening, they’re being funded and those are very long-term commitments.”

Issuers may consider tapping the green bond market to refinance their green debt if they see that green bonds have been “holding up more steady” in the secondary market during a crisis episode, he added.

“That can, for the issuer, be an argument to use green bonds as a funding vehicle if they have qualifying assets already,” Wacker said. “It could also be a positive for green issuance over the medium term.”

©2020 Bloomberg L.P.