U.S. Supply-Demand Mismatch Risks Shortages and Higher Prices

(Bloomberg Opinion) -- New data suggest that the economy has been growing for the past two months, although the distribution of that growth has been uneven. Consumption has been recovering more quickly than production, a divergence that will need to be resolved during the next few months. Some catch-up growth in manufacturing and housing should help offset any speed bumps in consumption that might come about from a second wave of the coronavirus or withdrawal of fiscal support by Congress.

The best encapsulation of this trend might be the advance retail sales and industrial production data released on Tuesday. Retail sales in May significantly outpaced expectations, rising 17.7% from the prior month and down just 6.1% from a year ago. The drivers of the improvement were sales of motor vehicles, furniture and clothing as states began reopening their economies, with consumers perhaps having some pent-up demand after sheltering-in-place for weeks.

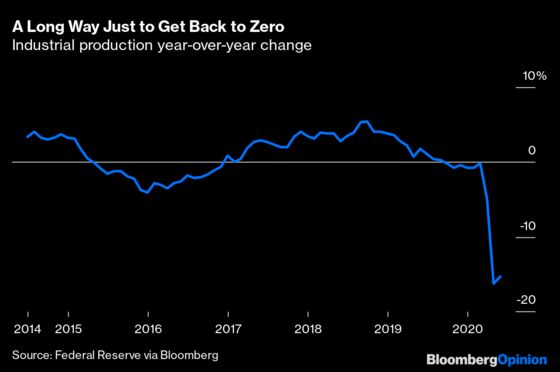

The same can’t be said for industrial production, which only grew 1.4% from the month before, and is still down 15.3% from a year earlier. Because of the nature of this economic dislocation, a shutdown of large parts of the economy in the midst of a public-health crisis, businesses are cautious about forecasting demand as they deal with challenges ranging from stressed supply chains to new safety regulations.

But consumption can only exceed production for so long before we see spot shortages or higher prices for some goods. We've seen this most dramatically in the housing industry. The housing market was already struggling with lack of supply before the crisis hit, and while both demand and construction plummeted as lock-down orders went into place, demand has bounced back faster than production.

The homebuilder Lennar gave a good explanation for why this environment is so difficult in its quarterly earnings conference call this week. The company noted that after a strong start to the year, sales plunged in March and April, with April orders declining 29% from a year earlier. The company's building activity slowed as a result, both in response to weaker demand and in an effort to preserve cash. Since then, Lennar has experienced the same rebound as the rest of the industry, and orders in the first two weeks of June rose 20% from a year earlier.

What this means is that even if demand remains strong -- not a certainty given the risk of a rise in infections -- Lennar will have a shortage of houses for sale in the second half of the year because of decisions made in March and April. This does provide an opportunity for other homebuilders, but it might mean an even more severe inventory shortage for would-be homebuyers. That would, of course, put more upward pressure on home prices while construction activity plays catchup.

Some of the same forces are at work in the auto industry. The rental-car industry has been hard-hit by the decline in travel, leading Hertz to file for bankruptcy. And yet used-car dealers aren't seeing rental-car companies selling their inventory to raise cash. The reason? Because of a lack of production by the automakers, they're worried that they won't be able to replenish inventories if and when demand for rental cars returns. Used-car prices have recovered, at least in part, because of this lack of inventory.

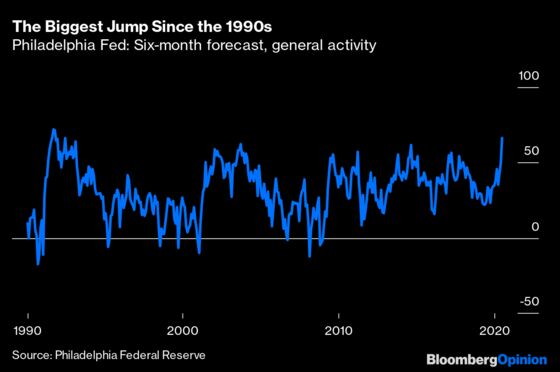

These demand-supply dynamics are among the reasons yesterday's Philadelphia Fed Business Outlook manufacturing survey showed that the six-month outlook for economic activity rose to its highest level since the early 1990s. Throughout the economy, production needs to catch up to meet even a subdued level of demand and rebuild inventories that have been drawn down during the past few months.

Despite signs of an economic rebound, many things still could derail this recovery. Virus hot spots in states such as Arizona, Texas and Florida could undo some of the economic progress made since April. Failure by Congress to extend fiscal relief programs put in place to respond to the crisis could have a similar effect. But with consumers showing more willingness to spend than seemed likely even a month or two ago, production needs to step up to meet that demand. Assuming it does, that added output should help boost economic growth in the months ahead. More worrisome would be if it doesn’t, and we get a mini-bout of stagflation marked by constrained production and higher prices.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Conor Sen is a Bloomberg Opinion columnist. He has been a contributor to the Atlantic and Business Insider.

©2020 Bloomberg L.P.