Leveraged Loan Exodus Deepens as Outflows Top $3 Billion

U.S. Leveraged Loan Exodus Deepens as Outflows Top $3 Billion

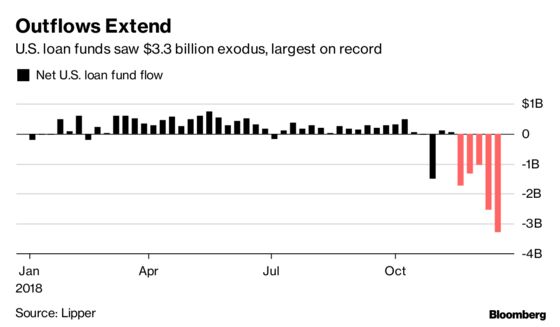

(Bloomberg) -- Investors pulled money out of U.S. loan funds at a record pace, withdrawing $3.3 billion in the week ended Dec. 19, as they grew increasingly spooked by market turmoil.

It was the fifth straight week of outflows of more than $1 billion, an exodus that’s driven prices to the lowest since September 2016, according to the S&P/LSTA Leveraged Loan Price Index. Investors withdrew around $3 billion from mutual funds that buy the debt, according to Lipper, while exchange-traded funds lost $299 million.

For much of the year capital poured into leveraged loans, drawn by debt investments that pay floating yields and offer protection against Federal Reserve rate hikes. Now the Fed is showing signs of slowing down, eroding investors’ incentive to buy loans. And fears of trade-war tensions, slowing growth and steep energy price declines have sapped fund managers’ appetite to take risk.

"With an uncertain rate story for 2019, on top of the persistent volatility, investors have started to move money away from loans," Jon Poglitsch, portfolio manager and head of credit research at Highland Capital, said in an email.

The sell-off followed a rout in equities and high-yield bonds that began in early October. Since the middle of November, prices have spiraled down and the debt has surrendered its gains. Leveraged loans returned around 4 percent this year through the end of September.

Since then, loans lost about 3 percent even after interest payments, with 2 percent of the drop this month. The safer leveraged loans that trade more often have been hit harder: loans made to companies with relatively high junk ratings, those with grades of BB- or higher, have fallen more than those in the B range, or one tier lower.

The volatility has made it more difficult for the biggest buyers of loans, collateralized loan obligations, to step in to fill the gap. New CLO issuance has slowed, and likely won’t fully come back till late January or even February, said Brian Juliano, head of U.S. bank loan portfolios at PGIM Fixed Income.

The outflows come as the loan market is poised to slow down for the holiday break, which exacerbated the volatility. Some money managers have sold loans in big chunks to get ahead of the liquidity squeeze and manage any redemptions, people familiar with the market have said. That has weighed on secondary prices, though that may now lessen the pressure if outflows are contained.

Prices Soften?

"Some loans funds got ahead of some of the outflows. So loan prices could soften less with future outflows, depending on the pace," said Jerry Cudzil, head of credit trading at TCW Group Inc. "Given loan market volatility and widening in CLO liabilities, CLO issuance will most likely be challenged in the near term. This negative feedback loop is further weighing on sentiment."

The waning demand has also hobbled efforts by banks to offload loans they’ve underwritten but not yet sold to investors. Lenders including Wells Fargo & Co., Barclays Plc and Goldman Sachs Group Inc. have taken the rare step of holding on to loans -- which are typically made to finance buyouts -- with the hope that they can resell them to investors later.

That’s been good for some: private debt funds are stepping in to buy loan deals on the cheap amid current market volatility, according to Todd Holleman, practice group leader for King & Spalding’s corporate, finance and investments practice.

In any event, fears are that the situation will worsen during the holiday period, raising questions about whether money managers have enough cash to weather more outflows.

"The mutual funds are injecting volatility, it’s driving everyone out,” said Michael Terwilliger, portfolio manager for the Resource Credit Income Fund. “Next week will be a real test since 95 percent of the market won’t be in their chairs, and there are further retail redemptions.”

To contact the reporter on this story: Lisa Lee in New York at llee299@bloomberg.net

To contact the editors responsible for this story: James Crombie at jcrombie8@bloomberg.net, Sally Bakewell, Dan Wilchins

©2018 Bloomberg L.P.