U.S. Junk Bonds Set $329.8 Billion Sales Record Amid Yield Hunt

U.S. Junk Bonds Set $329.8 Billion Sales Record Amid Yield Hunt

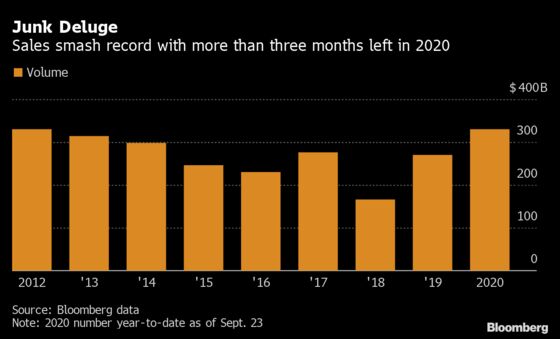

(Bloomberg) -- U.S. high-yield bond sales reached an annual record of $329.8 billion Wednesday as companies reap the benefits of the Federal Reserve’s liquidity-boosting policies and investors grasp for yield.

The crush of debt offerings accelerated in April after the U.S. central bank began purchasing some high-yield bonds as part of its efforts to support the corporate credit markets. Since then, issuance has eclipsed the prior annual sales record of $329.6 billion set in 2012, according to data compiled by Bloomberg.

Companies staring at sharp, pandemic-induced revenue declines were emboldened to borrow billions of dollars to help ride out the pandemic. Some of the most virus-battered borrowers, including airlines, hotels and even cruise operators, were able to tap investors for financing, sometimes paying double-digit coupons.

Now, junk-rated issuers have tilted away from securing lifelines and are instead looking to lock in lower interest rates and push out maturities on existing debt loads. The shift, coupled with support from the Fed, has forced investors to accept diminishing yields.

“A lot of the issuance was to get as much liquidity as you can, because things were looking like they were going to be stalled out for a while,” said Douglas Lopez, senior partner and portfolio manager at Aristotle Credit Partners. “This was the prudent move, but some companies may be building the liquidity bridge to nowhere.”

The junk market’s record year follows the U.S. investment-grade bond market, which reached a new annual issuance high in mid-August. Europe’s high-yield bond sales surged in July, the busiest for that month since 2009.

Fed Frenzy

The Fed’s near zero-interest rate policy, now expected to last through 2023, has paved the way for billions of dollars to flow into funds that invest in high-yield debt as investors search for yield.

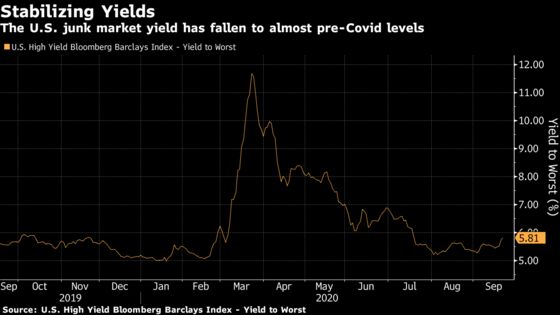

The support has effectively turned high-yield into a borrower’s market, and all-in yields for U.S. junk bonds have dropped to 5.81%, near pre-pandemic levels, according to Bloomberg Barclays index data.

Since July, some 65% of new high-yield bonds have come with sub-6% coupons, according to research by Barclays Plc strategists. Ball Corp. even set a record in August at 2.875% for the lowest coupon ever for a junk bond with a maturity of five years or longer.

Call protection, which prevents a company from repaying a bond early for a period of time, has been shortened in some deals, and covenant quality continues to be in the favor of issuers. Corporations are also using junk bonds to refinance leveraged loans, which are floating-rate and face a sub-1% London interbank offered rate benchmark.

But it’s not all bad news for investors. The recent refinancing wave means companies are managing their balance sheets and giving themselves breathing room, whereas the earlier deals to raise cash improved liquidity but also increased key measures of debt to earnings.

“It really is a smart finance move for these companies to refinance at lower costs and to push out these maturities,” said Nichole Hammond, a senior portfolio manager at Angel Oak Capital Advisors. “The more companies that do that, the better that is for the high-yield market from a fundamental perspective.”

More Refinancings

The flow of refinancings is expected to continue through September and into October. Issuers have pulled forward deals to get ahead of the uncertainty around the November presidential election and a possible second wave of Covid-19.

Though refinancing has surged, the leg of high-yield volume from acquisitions and leveraged buyouts has yet to return. Early discussions for new deals is picking up, but even if those are announced soon, the financings likely wouldn’t come until 2021.

Meanwhile, some of investors’ fears of mass defaults is fading as the market works through a spike in bankruptcies. Junk-bond deals that boosted liquidity also likely drove down default rates because companies had fresh cash to weather Covid-19’s sales hit, said Joseph Lind, senior portfolio manager at Neuberger Berman.

“It will create a hangover of having more debt on these balance sheets, but the rate environment today helps mitigate that,” Lind said.

©2020 Bloomberg L.P.