2014 Had Great GDP Quarter, Too. It Didn’t Last.

2014 Had Great GDP Quarter, Too. It Didn’t Last.

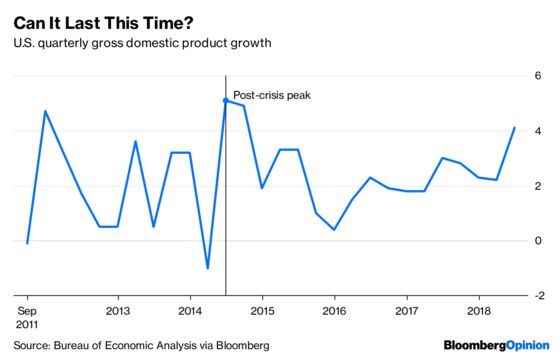

(Bloomberg Opinion) -- Friday’s strong second-quarter gross domestic product report brings up the question of whether it can be sustained in a way it wasn’t the last time GDP growth was this robust four years ago.

The economy in 2014 had some things going for it that the current economy lacks — a federal funds rate firmly anchored at zero and an economy still operating well below its potential, implying more room to grow without inflation being a concern. Yet an unexpected shock came in the form of the collapse of energy prices that dragged down growth during the next couple of years.

The good news in 2018 is it’s hard to see a demand shock lurking out there that might derail things the way energy did four years ago. But the bad news is that with the economy now operating above its potential, we’re going to need some positive surprises if this pace of growth is to be sustained.

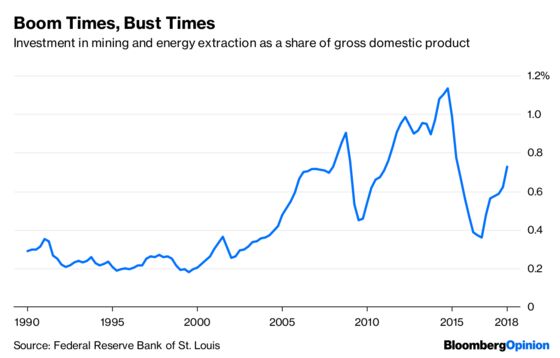

The surge in economic growth in the second and third quarters of 2014 was due in large part to a boom in energy investment. In the 1990s, the share of GDP attributable to fixed investment in mining exploration, shafts and wells was 0.2 percent. That share began to increase in the mid-2000s as the rising price of oil incentivized companies to invest in more energy production. This really took off after the financial crisis as the technology improved, new sources of supply were identified and the price of oil remained high. That same share of GDP due to mining investment peaked at 1.1 percent in the fourth quarter of 2014.

This might sound like a relatively small amount in the context of the vast U.S. economy. Of course, it’s not just the direct impact of that investment that mattered, but the multiplier effects. Industrial companies had to build equipment to support the industry. Trucking and rail companies had higher revenue as machinery and raw materials had to be shipped. In the West Texas shale patch, workers got paid more, which meant they could spend more on consumption. Tax revenue grew. Companies and countries around the world benefited.

But the bust reversed all that and then some. This is because in a bust, investment falls faster than it rose in the boom; it only took six quarters for energy investment as a share of GDP to erase five years of growth. Knock-on effects dented both the supply chain for the industry and the global economy, as the dollar surged, emerging-market economies struggled and credit spreads for the whole economy widened as investors feared how extensive the damage would be. By the fourth quarter of 2015, GDP growth was down to 0.4 percent from 5.1 percent in the second quarter of the prior year.

The good news in 2018 is the energy bust already happened, so that shouldn’t be something that can undermine the economy today. Housing is always an industry people think about when talking about the risk of a downturn. Yet, while land, labor, raw materials and interest rates have all been rising, demand for housing remains robust, with millennials entering their family-forming years and low supply in the marketplace. Muddling through seems like the worst case scenario for housing for now.

The challenge for the economy is how much more room there is for it to grow without inflation accelerating. This remains an unknown. Essentially, there are three frameworks for the state of the economy right now, and they each say things that to some extent are in conflict.

The first focuses on the unemployment rate and demographics. The jobless rate is low, and prospects for labor-force expansion due to population growth are minimal. Therefore, economic growth that puts more downward pressure on the unemployment rate could lead to a faster increase in inflation. Keep in mind that the unemployment rate, now at 4 percent, is below the Federal Reserve’s estimate of full employment.

A second model focused on the labor force participation makes a very different point. During the past 20 years, wage growth has had a closer correlation with the employment-population ratio than the unemployment rate. With prime-age labor force participation yet to return to its pre-crisis highs, the employment-to-population ratio still has room to grow before wage increases and inflation spiral out of control. So that suggest the economy should still have some room to grow.

A third model essentially says that inflation hasn’t been a problem in so long that we shouldn’t worry about it until it’s here. It’s true that inflation both in the U.S. and around the world has been below the target of central bankers since at least the late 1990s. It’s also true that for two consecutive economic cycles the Fed has tightened monetary policy too much too fast, leading to recessions. By this reasons, we’d be better off waiting until we’re absolutely sure inflation is a problem rather than relying too much on models that have arguably come up short during the past generation.

The prospects for sustainability of strong economic growth boil down to which model or models you believe. Between the stimulus from the tax bill, a lack of obvious signs of overinvestment in the economy, and millennial demographics, it’s possible that demand growth can remain strong for a while. It’s just a question of how long it takes for inflationary supply bottlenecks to emerge, and if the Fed decides to raise interest rates enough to end the cycle.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Conor Sen is a Bloomberg Opinion columnist. He is a portfolio manager for New River Investments in Atlanta and has been a contributor to the Atlantic and Business Insider.

©2018 Bloomberg L.P.