U.S. Economic Growth Seen Stumbling as Trade Hits Companies

Trade tensions likely helped push down U.S. economic growth last quarter to match the slowest pace of Donald Trump’s presidency.

(Bloomberg) --

Trade tensions likely helped push down U.S. economic growth last quarter to match the slowest pace of Donald Trump’s presidency, with a robust consumer keeping things from looking even worse.

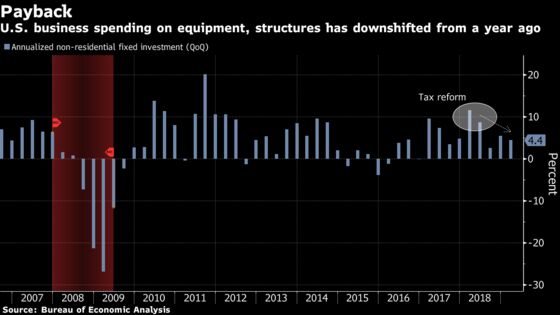

Gross domestic product figures due Friday will likely show business investment weakened, despite getting a late-quarter boost from higher equipment orders in June. Uncertainty from the yearlong U.S.-China tariff war compounded weakness stemming from slowing global growth and falling oil prices.

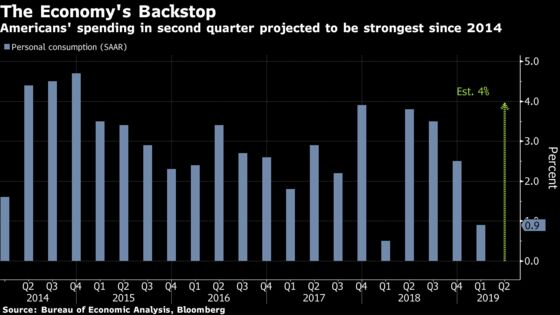

GDP rose 1.8% on an annualized basis in the second quarter, according to the median projection of analysts, which would be the slowest since 2017.

Net exports and inventories probably took a substantial bite in the April-June period, unwinding gains from the first quarter and reflecting fluctuations in companies’ stockpiles -- before and after various Trump tariff deadlines.

Together those items undercut what likely was the strongest increase in consumer spending since 2014. Continued solid gains in jobs and wages prevented growth from sinking into the doldrums -- at least for now.

‘‘The biggest factor weighing on growth is a rather sizable swing downward in inventories and net exports -- so they were the biggest contributors in the first quarter and they’ll be the biggest drag on the second quarter,” said Ellen Zentner, chief U.S. economist at Morgan Stanley.

The GDP report is unlikely to make much difference in a widely anticipated Federal Reserve move next week to cut interest rates by a quarter point. But the data will provide more detail on the state of the U.S. economy to help frame the central bank’s thinking on whether to follow up with additional easing this year, as investors are predicting.

The report, which will include annual revisions to data going back to 2014, is due at 8:30 a.m. in Washington.

While the 1.8% growth estimate isn’t far below the average rate during a relatively tepid expansion, it would still be the weakest since Trump took office in the first quarter of 2017. And it would mark a sharp decline from the 3.1% pace at the start of 2019.

Data Thursday showed a proxy for business investment jumped in June by the most since early 2018, aiding second-quarter GDP and indicating momentum for the third quarter. But a wider-than-expected merchandise-trade deficit and below-forecast inventories signaled a bigger drag from those items that overshadowed the more positive report.

The Atlanta Fed’s GDPNow tracking estimate for second-quarter growth fell to 1.3% from 1.6% after Thursday’s data.

What Our Economists Say

“While headline growth will be considerably slower than it was in the first quarter, the underlying fundamentals will be much more encouraging as consumer spending proves, once again, that it is up to the task of shouldering an outsized share of GDP gains.”

-- Carl Riccadonna, Eliza Winger and Yelena Shulyatyeva

The Trump administration targets annual growth of 3% and the president has frequently complained that the Fed’s interest-rate increases under Chairman Jerome Powell have held back the economy.

But it’s the trade war that’s partly holding things back now.

Companies are hesitating to expand as they wait to see if the U.S. and China resolve their differences, according to the Fed’s Beige Book and other anecdotal evidence. Caterpillar Inc., a frequent economic bellwether, said Wednesday that tariffs are boosting production costs and competition in China is eating into sales.

The grounding of Boeing Co.’s 737 Max jet for safety reasons is also denting the economy, with the company’s plane orders slowing to a trickle. The Institute for Supply Management’s index of manufacturers’ new orders fell in June to the lowest level since 2015, suggesting broader factory weakness will persist in coming months.

Trade Deficit

A widening trade deficit and less inventory accumulation may have knocked as much as 1.7 percentage point off the headline growth figure, ING Bank NV estimated before Thursday’s data. Those categories added a combined 1.5 point to growth in the first quarter. Imports likely jumped last quarter before the U.S. and China reached a trade truce in late June.

“There certainly was still a lot of flux as far as businesses looking at the outlook in regards to trade and having to manage around that,” said Sam Bullard, senior economist at Wells Fargo & Co.

Even so, the headwinds haven’t made much impact on the chief pillar of the economy -- consumer outlays, which probably climbed at a 4% pace during the period. Consumption looks to have rebounded from a paltry 0.9% first-quarter rate, which reflected the federal government shutdown and extremely cold weather in parts of the U.S.

“The good news is that the consumer came roaring back in the second quarter,” said Ryan Sweet, head of monetary-policy research at Moody’s Analytics Inc. “When you strip out net exports and inventories, that’s really the engine of the economy.”

With companies continuing to add workers at an elevated pace, and wage gains remaining solid, the Fed is seen favoring a less-dramatic quarter-point cut over a half-point reduction. The bigger question is whether the headwinds start filtering through to consumers.

“Does that potentially bleed over into the service sector and consumer spending? That’s what they’re looking at hard right now,” Bullard said.

--With assistance from Vince Golle.

To contact the reporters on this story: Katia Dmitrieva in Washington at edmitrieva1@bloomberg.net;Ryan Haar in New York at rhaar3@bloomberg.net

To contact the editors responsible for this story: Scott Lanman at slanman@bloomberg.net, Margaret Collins

©2019 Bloomberg L.P.