U.S. CLO Sales Hit Annual Record Amid Leveraged Buyout Loan Boom

U.S. CLO Sales Hit Annual Record Amid Leveraged Buyout Loan Boom

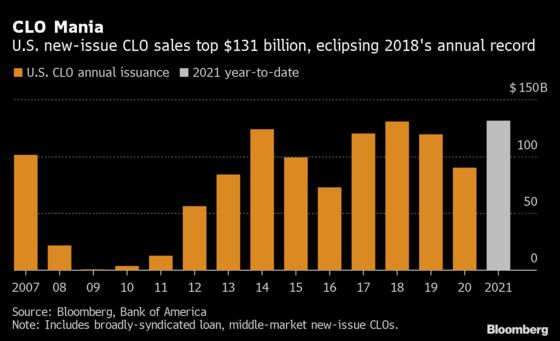

(Bloomberg) -- Sales of U.S. collateralized loan obligations reached a fresh annual record on Friday, topping $131 billion, as investors clamor to buy securities that offer high ratings and protection against inflation.

New issuance surpassed 2018’s record of $130.4 billion, and may not slow down in the coming months. Some banks are projecting that CLO sales can go as high as $160 billion, and there are some 200 short-term credit lines funding upcoming transactions.

CLOs, the biggest buyers of leveraged loans, are benefiting from heavy supply of buyout debt, including Medline Industries Inc., which on Thursday sold one of the biggest LBO loans ever. And the potential profit for putting together CLOs, also known as the arbitrage, is still relatively high. That makes it easier for firms to sell the riskiest parts of CLOs, called the equity.

“We are in a golden period for CLO equity, and demand for paper remains strong,” said Thomas Majewski, managing partner at Eagle Point Credit Management, which buys CLO equity.

CLOs have drawn some scrutiny from regulators and ratings firms, who had expressed concern that the quality of loans getting bundled into the securities had deteriorated. During the early stages of the pandemic, investors fretted that loans would get downgraded en masse or even default, bringing losses to at least some CLO investors.

But loan defaults have ended up being minimal, in part because of Federal Reserve and government rescue programs. Only a few low-ranked portions of U.S. CLOs are expected to default coming out of the 2020 economic downturn, S&P Global Ratings analysts said in a study released last month. As the economy recovers, many investors have grown more sanguine about the outlook for the securities.

The securities are also attractive because of their floating rates, which can translate to higher yields as inflation rises. CLOs typically pay higher yields for securities with higher ratings than their corporate bond counterparts.

“There’s continued acceptance of CLOs,” said Shiloh Bates, managing director at Flat Rock Global, a CLO equity investor. “They have gone from a backwater of finance to a more mainstream asset class.”

Fast Pace

CLO sales broke the $100 billion mark at the fastest pace on record this year, according to data compiled by Bloomberg. Moreover, August posted an official all-time monthly high for CLO offerings, with $19.6 billion sold, according to data compiled by Bloomberg News and Bank of America Corp. strategists that looks at broadly syndicated loans and middle-market new issue deals. The global CLO market has crossed the $1 trillion mark in outstandings.

And there may be as many as 200 active lines of credit financing CLOs now, known as warehouse lines, a 30% increase since July, estimates Western Asset Management Co. These figures are at or above 2018 levels when, according to data compiled by Bloomberg, the CLO market saw record annual issuance of $130.4 billion.

“The number of warehouses means banks feel comfortable that they can sell deals in this favorable environment,” said Ryan Kohan, head of leveraged loans at Western Asset.

New-issue CLOs from asset managers PGIM, Churchill Asset Management, PennantPark Investment Advisers, Irradiant Partners, First Eagle Alternative Credit, and Partners Group priced on Friday to put the tally over the top.

While the annual record refers to new-issue CLOs backed by broadly syndicated loans and middle market loans, the market has also hit a record for so-called refinancings and resets of older deals. When CLO spreads tighten, managers are able to get sweeter terms on refinancing or resetting outstanding transactions once they’ve exited their non-call periods. Even deals that were originated in 2020 that had one-year non-calls are being refinanced or reset.

There have been $88.2 billion of refinancings this year through Sept. 30, and $101.6 billion of so-called resets, which often tweak other parameters of the transaction, such as maturities, in addition to repricing at a lower rate.

©2021 Bloomberg L.P.